2015-01-10 22:00:00

OIL IS LOOKING FOR BOTTOM

Crude Oil

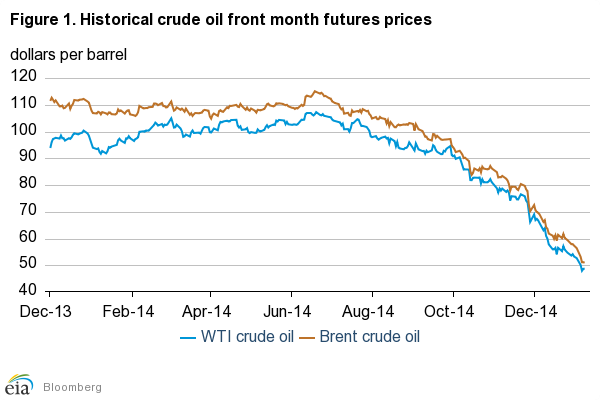

Prices: Crude oil markets continue to search for a bottom as prices declined again in December and the first week of January. The North Sea Brent front month futures price settled at $50.96/bbl on January 8, a decline of $21.58/bbl from December 1 (Figure 1). The front month West Texas Intermediate (WTI) contract price settled at $48.79/bbl on January 8, decreasing by $20.21/bbl since the start of December. Crude oil prices now have declined more than 50% compared with the 2014 highs in June.

A combination of news items indicating robust supply and weak demand growth help lower oil prices. Russian crude oil output was at record highs in December and the Iraq central government reached a deal with the Kurdish regional government on oil revenue sharing, which could lead to higher production volumes in the future. Although the U.S. economic data was strong, economic data in the rest of the world was generally below expectations and was met with declining equity prices and higher bond yields in many countries. With most of the projected increases in future global consumption coming from outside the United States, disappointing international economic news had more influence on crude oil prices than positive U.S. data.

For the sixth consecutive month, near-term crude oil futures prices continued to weaken relative to longer-dated ones as contango in both the Brent and WTI futures curves deepened. The Brent 1st-13th futures price spread settled at -$10.37/bbl and on January 8, a decline of $5.21/bbl since December 1 (Figure 2). The recent contango in Brent crude oil futures market is the deepest since April 2009, when global inventories were building strongly. Preliminary data for December implies inventory builds similar to those that occurred in the first half of 2009.

Commercial crude oil inventories in the United States have now built for three consecutive months, which is atypical for this time of year and reflects a loose crude oil market. The 1st-13th spread for WTI settled at -$7.51/bbl on January 8, $5.66/bbl lower compared to December 1.

Domestic and international crude oil prices fell at similar rates as differentials remained close to levels at the start of December and small relative to this time last year. The Brent-WTI spread settled at $2.17/bbl on January 8, a decline of $1.37/bbl since December 1 (Figure 3). Gulf coast spreads also remained close to Brent prices, with Louisiana Light Sweet (LLS) crude oil prices settling at a $1.07/bbl discount to Brent on January 8.

The LLS-WTI spread decreased slightly from December 1 to January 8 and may reflect slower movement of incremental barrels out of the Midwest (PADD 2) and into PADD 3. The LLS-WTI spread settled at $1.10/bbl on January 8, $1.45/bbl lower than on December 1. Refinery utilization remains higher in PADD 2 than in PADD 3 and may be contributing to the LLS-WTI differential trading below pipeline tariffs to move crude oil south.

Manufacturing Purchasing Manager's Index: The manufacturing Purchasing Manager's Index (PMI) serves as a leading indicator for manufacturing activity and was below expectations in December for the United States., China, and Europe. The PMI for the United States and China fell to 55.5 and 50.1 (where a reading of 50 indicates expansion in the manufacturing sector), respectively, in December and marked the lowest level of the index for China in 2014 (Figure 4). Eurozone PMI rose slightly in December but remains below levels from the first half of 2014. Slowing manufacturing activity increases the risk that future economic growth may fall below projections and potentially reduce future consumption of crude oil and petroleum products.

Trading Volume: From 2011 to 2013, total monthly trading volumes for Brent and WTI futures contracts were at the lowest levels in December of each year. However, that pattern did not continue in 2014, as recent price volatility has supported trading volumes. A total of 12.4 million and 14.1 million contracts were bought and sold in December for Brent and WTI, respectively (Figure 5). This was a decrease of only 0.2 million contracts from November for Brent and an increase of 1.9 million contracts for WTI. It was the smallest decline in trading volume from November to December for Brent since 2003 and the first increase in trading volume from November to December for WTI since 2009.

Volatility: Front month futures contract implied volatility moved higher for both WTI and Brent in December and the first week of January. Brent implied volatility settled at 44.7% on January 8, 6.3 percentage points higher than on December 1 (Figure 6). WTI implied volatility settled at 50.3% on January 8, an increase of 14.1 percentage points compared to December 1. Implied volatility for both Brent and WTI crossed over the 50% level for the first time since August 2011 in December. The elevated level of volatility reflects the large uncertainty in crude oil markets on both the supply and demand side going forward.

Market-Derived Probabilities: The April 2015 WTI futures contract averaged $50.74/bbl for the five trading days ending January 8 and has a probability of exceeding $65/bbl at expiration of 10%. The same contract for the five trading days ending December 1 had a probability of exceeding $65 of 70% (Figure 7). Because Brent prices are higher than WTI prices, the probability of Brent futures contracts expiring above the same dollar thresholds is higher.

Petroleum Products

Gasoline prices: The reformulated blendstock for oxygenate blending (RBOB, the petroleum component of gasoline) front month futures price declined 54 cents per gallon (gal) from December 1 to settle at $1.34/gal on January 8 (Figure 8). The RBOB-Brent crack spread declined by $0.03/gal from December 1 to settle at $0.13/gal on January 8. For much of the second half of 2014, gasoline prices have followed the decline in crude oil prices, with crack spreads remaining above the five-year average. However, the RBOB-Brent crack spread fell to near its five-year average in December.

Gasoline crack spreads weakened in December primarily due to increased gasoline supply from higher imports and refinery runs. Total U.S. motor gasoline imports for the four weeks ending January 2 were 0.8 million bbl/d, an increase of 0.3 million bbl/d since November, and 0.3 million bbl/d higher compared with December 2013. In the previous five years, the change in total gasoline imports from November to December was either negative or negligible. At the same time, total U.S. refinery gross inputs rose by 0.4 million bbl/d from November to December to 16.7 million bbl/d, adding more gasoline to the market.

The robust supply in the gasoline market contributed to a decrease in the RBOB 1st-13th futures curve spread, which fell to -$0.17/gal on January 8, the deepest contango since August 2010 (Figure 9). Total U.S. motor gasoline stocks rose from November to December by 29 million barrels, of which PADD 1, the delivery point of the RBOB futures contract, accounted for 12 million barrels.

The increase in gasoline stocks in the United States was much larger than the five-year average increase of 8 million barrels. Similarly, the five-year average increase in PADD 1 gasoline stocks was 3 million barrels, indicating a comparatively weaker near-term market for gasoline than in previous years.

Heating oil prices: The front month futures price for heating oil decreased $0.50/gal from December 1, settling at $1.71/gal on January 8 (Figure 10). The heating oil-Brent crack spread was nearly unchanged from December 1 and settled at$0.50/gal on January 8.

While much of the recent decline in heating oil prices can be attributed to the decline in crude oil prices, crack spreads in November and December remained near the top of the five-year range. In December, distillate production increased to a four-week average of 5.2 million bbl/d, up 0.3 million bbl/d from November and the highest production total for December on record. Subsequently, inventories, rose by almost 21 million barrels, which could put downward pressure on crack spreads going forward if inventory builds continue.

Volatility: Implied volatility for both RBOB and heating oil continue to rise rapidly as uncertainty over future price movements remains elevated in both product markets. Implied volatility for the front month RBOB contract and for the front month heating oil contract increased 7.4 percentage points and 2.2 percentage points, respectively, from December 1 to settle at 42.6% and 32.6%, respectively, on January 8 (Figure 11).

Market-Derived Probabilities: The April 2015 RBOB futures contract averaged $1.63/gal for the five trading days ending January 8 and has an 8% probability of exceeding $2.10/gal (typically leading to a retail price of $2.75/gal) at expiration. The same contract for the five trading days ending December 1 had a 55% probability of exceeding $2.10/gal (Figure 12).

Natural Gas

Prices: After increasing in November, natural gas futures prices declined in December, displaying the largest month-over-month price drop since July 2008. The front month futures contract for delivery at Henry Hub settled at $2.93/MMBtu on January 8, a decline of $1.08/MMBtu compared to December 1 and the first settlement under $3.00/MMBtu in more than two years (Figure 13). Mild winter weather, combined with high production, led to a net storage injection in certain areas of the United States in late December, contributing to the price declines.

Whereas heating degree days (HDD) were 73 HDD above the 30-year normal in November, they fell to 46 HDD below normal in December, decreasing demand. Furthermore, dry gas production has continued to grow, with the latest EIA monthly data showing another all-time high in production of 72.2 Billion cubic feet (Bcf) per day in October. The production gains and low demand resulted in a year-over-year build in inventories in early December, recovering from a year-over-year deficit of almost 900 Bcf in February of 2014. Increases in inventory may raise storage costs, contributing to a fall in front month futures prices compared with longer dated contracts. The difference between the front month and 13th month price reached the lowest in more than two years, dropping $0.42/MMBtu since December 1 to settle at -$0.52/MMBtu on January 8 (Figure 14).

Volatility: Implied volatility for the natural gas front month futures contract settled at 58.1% on January 8, 6.4 percentage points higher than the close on December 1 and averaged over 50% for the second consecutive month. Historical volatility also rose, settling at 61% on January 8, reflecting uncertainty due to fluctuating winter temperatures (Figure 15).

Market-Derived Probabilities: The April 2015 Henry Hub futures contract averaged $2.88/MMBtu for the five trading days ending January 8 and has a 15% probability of exceeding $3.50/MMBtu at expiration. The same contract for the five trading days ending December 1 had a 59% probability of exceeding $3.50/MMBtu (Figure 16).

eia.gov