2017-03-16 18:40:00

STRENGTHENING IMF

IMF - There are two key shifts taking place that have implications for global financial stability.

First, the center of global economic "gravity" continues to shift. This reflects the core role of emerging markets and the ongoing integration of developing economies. The numbers clearly highlight the trend: since 2000, the share of emerging and developing economies in global GDP has increased more than two thirds. It reached almost 40 percent in 2015. This transformation has had a direct impact on the IMF—in terms of both policy and governance. The shift toward the emerging markets under the 2010 quota reforms was one direct result.

Second, we are witnessing the rapid rise of financial interconnectedness. Global capital flows and external liabilities have risen sharply over the past three to four decades as countries have opened their capital accounts, and financial markets have deepened. Here, too, the numbers tell the story: gross external liabilities stood above 160 percent of world GDP in 2015; up from 30 percent of world GDP in 1980.

We all understand the strain that these shifts are putting on the international monetary system. Our world is becoming more and more multipolar. While greater interconnectedness allows economies to benefit from a globalized economy, it also presents new weaknesses. We face the risk of new sources of spillovers and spillbacks, as we saw in 2015 with China's financial market difficulties. All of this complicates macroeconomic management.

Global imbalances are an important part of this picture. We have witnessed sustained periods of imbalances. While they have narrowed since the crisis, they remain above desirable levels. In the absence of formal adjustment mechanisms, adjustment has largely achieved through demand compression in deficit countries.

The concentration of imbalances among a few large countries presents a risk to the global economy. It increases vulnerabilities—and even raises the risk of market disruptions.

To address imbalances will require cooperation among deficit and surplus countries. To facilitate this process, the IMF has overhauled its surveillance process and strengthened its analytical tools. This includes the introduction of the External Sector Report, which assesses the largest economies' external positions and analyzes potential spillovers in a multilateral context. These analyses then become an integral part of our bilateral surveillance, where we discuss implications of policies with the relevant authorities.

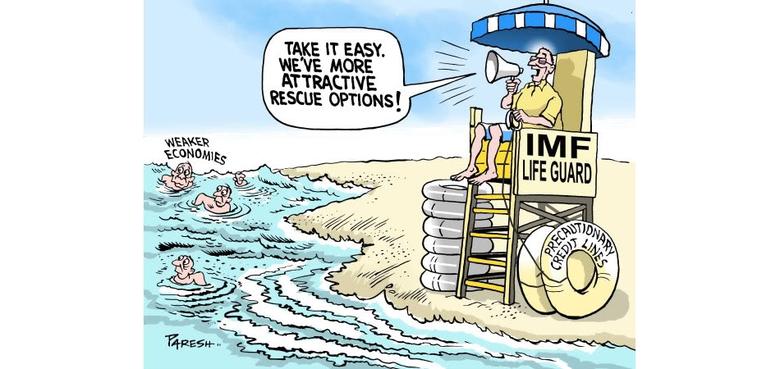

In addition to this, what is needed is a safety net that could make timely and sufficient liquidity support available to all countries. This could reduce the impulse to self-insurance that lies behind reserve accumulation.

You know the important role that international efforts played in stemming the global financial crisis. They provided important financing to some countries and shielded others that might have been at risk. But it is clear that shortcomings remain.

The IMF has led the reform effort to strengthen the safety net. Thanks to the support of our membership, our lending capacity was boosted to $1 trillion. We overhauled our lending framework to offer more insurance and financing instruments. We are now exploring the possibility of a new short-term liquidity facility and a non-financial policy instrument. These would provide monitoring and signaling of member countries' policies.

We are now working to remove the perception that Fund programs carry a stigma. We want to encourage countries to approach the Fund earlier—when they see a shock coming. I think there has been progress: for example, our Flexible Credit Line is seen as a sign of strength for the economies that have used it.

We are also exploring whether the SDR, in its various forms can play a greater systemic role in strengthening the IMS. This could include the official SDR, SDR-denominated assets, or the SDR as a unit of account. The IMF reached a milestone last year when the renminbi was included in the SDR basket. That enhanced the SDR as a reserve asset. Also, in the last year large SDR-denominated bonds were successfully placed in China.

Regional Financing Arrangements have become an important component of the safety net at the regional level. They complement IMF resources. We welcomed the doubling of resources under the Chiang Mai Initiative Multilateralization to $240 billion from 2014. We also are working to strengthen cooperation through structured dialogue.

At the same time, we need to recognize that a central element of the safety net is reserve accumulation. This has served an important purpose—especially in this region since the Asian Crisis.

But reserve accumulation can be a costly defense. It leads to inefficient resource allocation, hinders external adjustment, and can contribute to looser policies on the part of reserve issuers.

So the Fund's view is that the international community should continue working to upgrade the safety net. This involves questions of size, predictability, and timelines of liquidity support.

Now let's turn to the internationalization of currencies, a topic that has become of central importance to Asia and the international monetary system.

From a systemic point of view, the greater use of multiple currencies has the potential to diversify risks, enable gradual global adjustments, and provide incentives for sustainable policies. It also can help create a more stable environment for capital flows—thus enhancing systemic stability. It can do this by reducing tensions between domestic policies in reserve-issuing countries and the liquidity needs of the global economy.

At the country level, the benefits may include lower transaction costs and reduced exchange rate risk, and the ability to issue foreign debt on more competitive terms.

International experience has shown that countries wishing to promote greater international use of their currencies need to safeguard macroeconomic stability, increase the flexibility of their monetary frameworks, and deepen their financial markets. From this point of view, the internationalization of a currency may well come simply as a by-product of such a policy agenda.

At the same time, we have to recognize that a multi-currency system alone will not solve the shortcomings of the IMS. In fact, it potentially could increase systemic risks. If the domestic policies of reserve issuers produce what are called "switching effects" between two dominant currencies, financial volatility could increase—as could external imbalances. There is no substitute for strong policies.

That must be the bottom line, if we are to remain vigilant against the challenges to the international monetary system. The IMF is prepared to assist its membership in this effort. This is how we can be more effective in preventing crises and responding to those that arise.

-----

Earlier:

IMF: EXTERNAL RISKS FOR RUSSIA