2017-07-26 14:40:00

WORLD OIL CHOKEPOINTS

EIA - The U.S. Energy Information Administration (EIA) defines world oil chokepoints as narrow channels along widely used global sea routes, some so narrow that restrictions are placed on the size of the vessel that can navigate through them. Chokepoints are a critical part of global energy security because of the high volume of petroleum and other liquids transported through their narrow straits.

In 2015, total world petroleum and other liquids supply was about 96.7 million barrels per day (b/d). EIA estimates that about 61% that amount (58.9 million b/d) traveled via seaborne trade. Oil tankers accounted for almost 28% of the world's shipping by deadweight tonnage in 2016, according to data from the United Nations Conference on Trade and Development (UNCTAD), having fallen steadily from 50% in 1980.

International energy markets depend on reliable transport routes. Blocking a chokepoint, even temporarily, can lead to substantial increases in total energy costs and world energy prices. Chokepoints also leave oil tankers vulnerable to theft from pirates, terrorist attacks, political unrest in the form of wars or hostilities, and shipping accidents that can lead to disastrous oil spills.

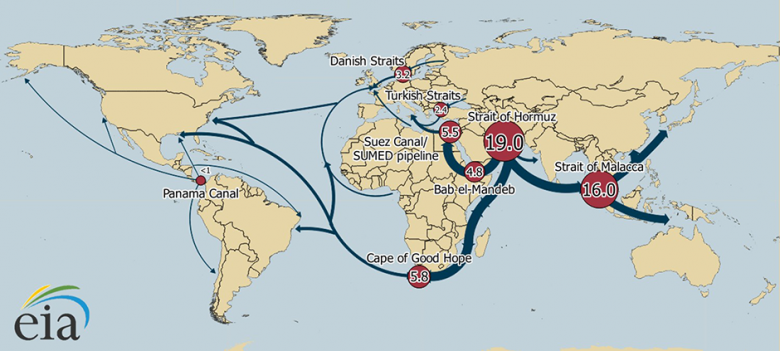

The seven chokepoints highlighted in this report are part of major trade routes for global seaborne oil transportation. Disruptions to these routes could affect oil prices and add thousands of miles of transit in alternative routes. By volume of oil transit, the Strait of Hormuz, leading out of the Persian Gulf, and the Strait of Malacca (linking the Indian and Pacific Oceans) are the world's most important strategic chokepoints. This report also discusses the role of the Cape of Good Hope, which is not a chokepoint but is a major trade route and potential alternate route to certain chokepoints.

| Location | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|

| Strait of Hormuz | 17.0 | 16.8 | 16.6 | 16.9 | 17.0 | 18.5 |

| Strait of Malacca | 14.5 | 15.1 | 15.4 | 15.5 | 15.5 | 16.0 |

| Suez Canal and SUMED Pipeline | 3.8 | 4.5 | 4.6 | 5.2 | 5.4 | 5.5 |

| Bab el-Mandab | 3.3 | 3.6 | 3.8 | 4.3 | 4.7 | 4.8 |

| Danish Straits | 3.0 | 3.3 | 3.1 | 3.0 | 3.2 | 3.2 |

| Turkish Straits | 2.9 | 2.7 | 2.6 | 2.6 | 2.4 | 2.4 |

| Panama Canal | 0.8 | 0.8 | 0.8 | 0.9 | 1.0 | 0.9 |

| Cape of Good Hope | 4.7 | 5.4 | 5.1 | 4.9 | 5.1 | 5.8 |

| World maritime oil trade | 55.5 | 56.4 | 56.5 | 56.4 | 58.9 | n/a |

| World total petroleum and other liquids supply | 88.8 | 90.8 | 91.3 | 93.8 | 96.7 | 97.2 |

| Note: Data for Panama Canal are by fiscal year. Sources: U.S. Energy Information Administration analysis based on Lloyd's List Intelligence, Panama Canal Authority, Argus FSU, Suez Canal Authority, GTT, BP Statistical Review of World Energy, IHS Waterborne, Oil and Gas Journal, and UNCTAD, using EIA conversion factors. |

||||||

Strait of Hormuz

The Strait of Hormuz is the world's most important chokepoint, with an oil flow of 17 million b/d in 2015, about 30% of all seaborne-traded crude oil and other liquids during the year. In 2016, total flows through the Strait of Hormuz increased to a record high of 18.5 million b/d.

Located between Oman and Iran, the Strait of Hormuz connects the Persian Gulf with the Gulf of Oman and the Arabian Sea. The Strait of Hormuz is the world's most important oil chokepoint because its daily oil flow of about 17 million barrels per day in 2015, accounted for 30% of all seaborne-traded crude oil and other liquids. The volume that traveled through this vital choke point increased to 18.5 million b/d in 2016.

EIA estimates that about 80% of the crude oil that moved through this chokepoint went to Asian markets, based on data from Lloyd's List Intelligence tanker tracking service.6 China, Japan, India, South Korea, and Singapore are the largest destinations for oil moving through the Strait of Hormuz.

Qatar exported about 3.7 trillion cubic feet per year of liquefied natural gas (LNG) through the Strait of Hormuz in 2016, according to BP's Statistical Review of World Energy 2017.7 This volume accounts for more than 30% of global LNG trade. Kuwait imports LNG volumes that travel northward through the Strait of Hormuz.

At its narrowest point, the Strait of Hormuz is 21 miles wide, but the width of the shipping lane in either direction is only two miles wide, separated by a two-mile buffer zone. The Strait of Hormuz is deep enough and wide enough to handle the world's largest crude oil tankers, with about two-thirds of oil shipments carried by tankers in excess of 150,000 deadweight tons coming through this Strait.

Strait of Malacca

The Strait of Malacca, linking the Indian Ocean and the Pacific Ocean, is the shortest sea route between the Middle East and growing Asian markets. Flows through the Strait of Malacca rose to 16 million b/d in 2016, retaining its position as the second busiest transit chokepoint.

The Strait of Malacca, located between Indonesia, Malaysia, and Singapore, links the Indian Ocean to the South China Sea and to the Pacific Ocean. The Strait of Malacca is the shortest sea route between Persian Gulf suppliers and the Asian markets—notably China, Japan, South Korea, and the Pacific Rim.

Oil shipments through the Strait of Malacca supply China and Indonesia, two of the world's fastest-growing economies. This Strait is the primary chokepoint in Asia, with an estimated 16.0 million b/d flow in 2016, compared with 14.5 million b/d in 2011. Crude oil generally makes up between 85% and 90% of total oil flows per year, and petroleum products account for the remainder (Table 3).

At its narrowest point in the Phillips Channel of the Singapore Strait, the Strait of Malacca is only about 1.7 miles wide, creating a natural bottleneck with the potential for collisions, grounding, or oil spills. According to the International Maritime Bureau's Piracy Reporting Centre, piracy, including attempted theft and hijackings, is a threat to tankers in the Strait of Malacca, and ships saw an increasing number of attacks in 2015. Data for 2016 were not available at the time of publication.

If the Strait of Malacca were blocked, nearly half of the world's fleet would be required to reroute around the Indonesian archipelago, such as through the Lombok Strait between the Indonesian islands of Bali and Lombok, or through the Sunda Strait between Java and Sumatra.Rerouting would tie up global shipping capacity, add to shipping costs, and potentially affect energy prices.

Several proposals have been made to build bypass options and reduce tanker traffic through the Strait of Malacca. In particular, China and Myanmar (Burma) commissioned the Myanmar-China natural gas pipeline in 2013 that stretches from Myanmar's ports in the Bay of Bengal to the Yunnan province of China. The pipeline has a capacity of 424 billion cubic feet per year. The oil portion of the pipeline was completed in August 2014 and it is now operational at full capacity since the 260,000 b/d refinery in Yunnan, China, began operating in June 2017. The Myanmar-China oil line transports Middle Eastern oil, allowing it to bypass the Strait of Malacca.

The Strait of Malacca is also an important transit route for liquefied natural gas (LNG) from Persian Gulf and African suppliers, particularly Qatar, to East Asian countries with growing LNG demand. The biggest importers of LNG in the region are Japan and South Korea.

| million barrels per day | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|

| Total oil flows through Strait of Malacca | 14.5 | 15.1 | 15.4 | 15.5 | 15.5 | 16.0 |

| crude oil | 12.8 | 13.2 | 13.3 | 13.3 | 13.9 | 14.6 |

| refined products | 1.7 | 1.9 | 2.1 | 2.2 | 1.6 | 1.4 |

| LNG (Tcf per year) | 2.8 | 3.5 | 3.9 | 4.1 | 3.6 | 3.2 |

| Notes: Tcf = Trillion cubic feet. Sources: U.S. Energy Information Administration analysis based on Lloyd’s List Intelligence, IHS Waterborne, BP. |

||||||

Suez Canal/SUMED Pipeline

The Suez Canal and the SUMED Pipeline are strategic routes for Persian Gulf oil and natural gas shipments to Europe and North America. These two routes combined accounted for about 9% of the world's seaborne oil trade in 2015.

Suez Canal

The Suez Canal is located in Egypt and connects the Red Sea and the Gulf of Suez with the Mediterranean Sea. In 2016, total petroleum and other liquids (crude oil and refined products) and LNG accounted for 17% and 6% of total Suez cargoes, measured by net metric tonnage, respectively. The Suez Canal cannot handle Ultra Large Crude Carriers (ULCC) and fully laden Very Large Crude Carriers (VLCC) class crude oil tankers. The Suezmax was the largest ship that could navigate through the canal until 2010, when the Suez Canal Authority extended the canal depth to 66 feet to allow more than 60% of all tankers to transit the Canal, according to the Suez Canal Authority. In addition, almost 93% of bulk carriers and 100% of container ships have been able to transit the Suez Canal since 2010.

In 2016, 3.9 million b/d of total oil (crude oil and refined products) transited the Suez Canal in both directions, according to data published by the Suez Canal Authority. Northbound flows rose by about 300,000 b/d in 2016, but southbound shipments decreased for the first time since at least 2009. Increased crude oil exports from Iraq and Saudi Arabia to Europe contributed to higher northbound traffic, while lower exports of petroleum products from Russia to Asia contributed the most to lower southbound traffic.

Most oil transiting the Suez Canal was sent northbound (2.4 million b/d) toward European and North American markets, and the remainder was sent southbound (1.5 million b/d), mainly toward Asian markets. Oil exports from Persian Gulf countries (Saudi Arabia, Iraq, Kuwait, United Arab Emirates, Iran, Oman, Qatar, and Bahrain) accounted for 84% of Suez Canal northbound oil flows. The largest importers of northbound oil flows through the Suez Canal in 2016 were European countries (78%) and the United States (14%). Oil exports from Russia accounted for the largest share of (17%) of Suez southbound oil flows, followed by Turkey (15%) and Netherlands (11%). North Africa (Algeria and Libya) made up 12% of the southbound flow. The largest importers of Suez southbound oil flows were Asian countries, with Singapore, China and India accounting for more than 50% of the total.

Total traffic through the Suez Canal has been steadily increasing since 2009, and total oil flows rose to more than 2 million b/d by 2014. The increase in oil shipments during 2015 and 2016 in particular reflect increased OPEC production and exports, including increased output in Iraq and Saudi Arabia, and increased exports from Iran in 2016 as sanctions targeting its oil exports were eased.

SUMED Pipeline

The 200-mile long SUMED Pipeline, or Suez-Mediterranean Pipeline, transports crude oil through Egypt from the Red Sea to the Mediterranean Sea. The crude oil flows through two parallel pipelines that are 42 inches in diameter, which have a total pipeline capacity of 2.34 million b/d. Oil flows north starting at the Ain Sukhna terminal along the Red Sea coast to its end point at the Sidi Kerir terminal on the Mediterranean Sea. SUMED is owned by the Arab Petroleum Pipeline Company, a joint venture between the Egyptian General Petroleum Corporation (50%), Saudi Aramco (15%), Abu Dhabi's International Petroleum Investment Company (15%), multiple Kuwaiti companies (15%), and Qatar Petroleum (5%).

The SUMED Pipeline is the only alternate route to transport crude oil from the Red Sea to the Mediterranean Sea if ships cannot navigate through the Suez Canal. Closure of the Suez Canal and the SUMED Pipeline would require oil tankers to divert around the southern tip of Africa, the Cape of Good Hope, which would add approximately 2,700 miles to the transit from Saudi Arabia to the United States. The increased transit time would also increase costs and shipping time, according to the U.S. Department of Transportation. According to the International Energy Agency (IEA), shipping around Africa would add 15 days of transit to Europe and 8–10 days to the United States.

Fully laden VLCCs going toward the Suez Canal also use the SUMED Pipeline for lightering. Lightering occurs when a vessel needs to reduce its weight and draft by offloading cargo to enter a restrictive waterway, such as a canal. The Suez Canal is not deep enough for a fully-laden VLCC and, therefore, a portion of the crude is offloaded at the SUMED Pipeline at the Ain Sukhna terminal. The now partially-laden VLCC goes through the Suez Canal and picks up the offloaded crude at the other end of the pipeline at the Sidi Kerir terminal.

In 2016, 1.6 million b/d of crude oil was transported through the SUMED Pipeline to the Mediterranean Sea, and then loaded onto tankers for seaborne trade. Flows via SUMED were relatively unchanged compared with 2015. Total oil flows via SUMED and the Suez Canal were 5.5 million b/d in 2016, 100,000 b/d more than in 2015. Total oil flows via the Suez Canal and SUMED pipeline accounted for about 9% of total seaborne-traded oil in 2015.

| million barrels per day | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|

| Total oil flows via the Suez Canal and SUMED pipeline | 3.8 | 4.5 | 4.6 | 5.2 | 5.4 | 5.5 |

| Suez Canal total flows | ||||||

| crude oil | 0.7 | 1.4 | 1.5 | 1.8 | 1.6 | 1.8 |

| refined products | 1.4 | 1.6 | 1.7 | 2.0 | 2.2 | 2.0 |

| total oil | 2.2 | 2.9 | 3.2 | 3.7 | 3.8 | 3.9 |

| LNG (Tcf per year) | 2.1 | 1.5 | 1.2 | 1.2 | 1.3 | 1.2 |

| Suez northbound flows | ||||||

| crude oil | 0.5 | 0.9 | 1.1 | 1.4 | 1.2 | 1.4 |

| refined products | 0.9 | 0.8 | 0.7 | 0.8 | 0.8 | 1.0 |

| total oil | 1.4 | 1.7 | 1.9 | 2.1 | 2.1 | 2.4 |

| LNG (Tcf per year) | 1.8 | 1.2 | 1 | 0.9 | 1.1 | 0.8 |

| Suez southbound flows | ||||||

| crude oil | 0.2 | 0.5 | 0.4 | 0.4 | 0.4 | 0.4 |

| refined products | 0.6 | 0.8 | 1 | 1.2 | 1.4 | 1.1 |

| total oil | 0.8 | 1.3 | 1.3 | 1.6 | 1.7 | 1.5 |

| LNG (Tcf per year) | 0.2 | 0.3 | 0.2 | 0.3 | 0.3 | 0.3 |

| SUMED pipeline crude oil flows | 1.7 | 1.5 | 1.5 | 1.5 | 1.6 | 1.6 |

| Notes: Totals may not exactly match corresponding values as a result of independent rounding. Tcf = Trillion cubic feet. Source: U.S. Energy Information Administration analysis based on Lloyd’s List Intelligence, Suez Canal Authority (with EIA conversions). |

||||||

Liquefied natural gas (LNG)

LNG flows through the Suez Canal in both directions were 1.2 Tcf in 2016, accounting for 9% of total LNG transported worldwide.

LNG flows through the Suez Canal in both directions were 1.2 trillion cubic feet (Tcf) in 2016, accounting for about 9% of total LNG traded worldwide. Southbound LNG transit mostly originates in Nigeria, France (as re-exports), and Trinidad and Tobago, mostly destined for Egypt, Jordan, and Japan, which combined account for more than 65% of the total southbound LNG imports through the canal. Nearly all of the northbound transit (99%) is from Qatar and is mainly destined for European markets. The rapid growth in LNG flows through the Suez Canal after 2008 represents the expansion of LNG exports from Qatar.

LNG flows through the Suez Canal in both directions have declined from their peak of almost 2.1 Tcf in 2011. The decrease mostly reflects the fall in northbound LNG flows and is consistent with LNG import data for the United States, which show that total LNG imports fell dramatically between 2011 and 2016. U.S. LNG imports from Qatar fell from 91 billion cubic feet in 2011 to zero in 2014 and have remained at this level since then. The changes reflect growing domestic natural gas production in the United States, a decrease in LNG demand in some European countries, and strong competition for LNG in the global market. As a result, Suez LNG flows as a share of total LNG traded worldwide fell to 9% in 2016, compared with 18% in 2011.

Bab el-Mandeb

Closing the Bab el-Mandeb Strait could keep tankers in the Persian Gulf from reaching the Suez Canal and the SUMED Pipeline, diverting them around the southern tip of Africa.

The Bab el-Mandeb Strait is a chokepoint between the Horn of Africa and the Middle East, and it is a strategic link between the Mediterranean Sea and the Indian Ocean. The strait is located between Yemen, Djibouti, and Eritrea, and it connects the Red Sea with the Gulf of Aden and the Arabian Sea. Most exports from the Persian Gulf that transit the Suez Canal and the SUMED Pipeline also pass through Bab el-Mandeb. An estimated 4.8 million b/d of crude oil and refined petroleum products flowed through this waterway in 2016 toward Europe, the United States, and Asia, an increase from 3.3 million b/d in 2011.

The Bab el-Mandeb Strait is 18 miles wide at its narrowest point, limiting tanker traffic to two 2-mile-wide channels for inbound and outbound shipments. Closure of the Bab el-Mandeb could keep tankers originating in the Persian Gulf from reaching the Suez Canal or the SUMED Pipeline, diverting them around the southern tip of Africa, which would add to transit time and cost. In addition, European and North African southbound oil flows could no longer take the most direct route to Asian markets via the Suez Canal and Bab el-Mandeb.

| million b/d | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|

| Total oil flows | 3.3 | 3.6 | 3.8 | 4.3 | 4.7 | 4.8 |

| Northbound | 2.0 | 2.0 | 2.1 | 2.2 | 2.5 | 2.8 |

| Southbounds | 1.3 | 1.6 | 1.7 | 2.1 | 2.2 | 2.0 |

| Note: Totals may not exactly match corresponding values as a result of independent rounding. Sources: U.S. Energy Information Administration analysis based on Lloyd’s List Intelligence, Suez Canal Authority, and GTT, using EIA conversion factors. |

||||||

Turkish Straits

Although still an important chokepoint for petroleum liquids transit from the Caspian Sea region, the Turkish Straits have seen declining transit volumes since 2011, falling to 2.4 million b/d in 2016. Oil moving through these straits supplies Western and Southern Europe.

The Turkish Straits, which includes the Bosporus and Dardanelles waterways, divide Asia from Europe. The Bosporus is a 17-mile waterway that connects the Black Sea with the Sea of Marmara. The Dardanelles is a 40-mile waterway that links the Sea of Marmara with the Aegean and Mediterranean Seas. Both waterways are located in Turkey and supply Western and Southern Europe with oil from Russia and the Caspian Sea region.

An estimated 2.4 million b/d of crude oil and petroleum products flowed through the Turkish Straits in 2016. More than 80% of this volume was crude oil. These Black Sea ports are among the primary oil export routes for Russia and other Eurasian countries including Azerbaijan and Kazakhstan.

Oil shipments through the Turkish Straits decreased from 2.9 million b/d in 2011 to 2.4 million b/d in 2016. At its peak, more than 3.4 million b/d transited the straits in 2004, but the volume that traveled through the Turkish Straits fell in the mid-2000s as Russia shifted crude oil exports away from the Black Sea and toward the Baltic ports. Subsequent increases in production and exports from Azerbaijan and Kazakhstan resulted in an increase in shipments through the Turkish Straits, but the increasing trend did not last: Turkish Straits have seen a steady decrease in traffic over the past five years. These volumes may increase in the future as Kazakhstan's production of crude oil increases and the country exports more crude oil via Black Sea. EIA expects Kazakhstan's crude oil production to increase through at least the end of 2018 as volumes from the country's Kashagan field continue to rise.

Only half a mile wide at the narrowest point, the Turkish Straits are among the world's most difficult waterways to navigate because of their sinuous geography. About 48,000 vessels transit the straits each year, making this area one of the world's busiest maritime chokepoints.Commercial shipping has the right of free passage through the Turkish Straits in peacetime, although Turkey claims the right to impose regulations for safety and environmental purposes. Bottlenecks and heavy traffic also create problems for oil tankers in the Turkish Straits.

Panama Canal

The Panama Canal is not a significant route for U.S. petroleum trade. The recently completed expansion of the canal is unlikely to significantly change crude oil and petroleum product flows, with the exception of U.S. propane exports. Crude oil and petroleum liquids tankers accounted for a small portion of total transit traffic through the canal in 2016.

The Panama Canal is an important route connecting the Pacific Ocean with the Caribbean Sea and the Atlantic Ocean. The canal is 50 miles long and only 110 feet wide at its narrowest point—the Culebra Cut—at the Continental Divide.19 More than 13,000 vessels transited the Panama Canal in fiscal year 2016, representing roughly 204 million tons of cargo. Goods originating in or traveling to the United States accounted for more than 67% of the total shipments passing through the Panama Canal during 2016; China's share was a distant second at roughly 19%.

Alternatives to the Panama Canal include the Straits of Magellan, Cape Horn, and Drake Passage at the southern tip of South America, but these routes would significantly increase transit times and costs, adding about 8,000 miles of travel.

Although petroleum and petroleum products represented 27% of the principal commodities that crossed through the Panama Canal from the Atlantic to the Pacific in 2016, that canal is not a significant route for global petroleum and petroleum product transit. Northbound (Pacific to Atlantic) traffic of petroleum and petroleum products accounted for only 9% of the total products traveling through the canal. In 2015, 1.7% of total global maritime petroleum and petroleum product flows went through the Panama Canal. According to the Panama Canal Authority, 921,000 b/d of petroleum and petroleum products were transported through the canal in fiscal year 2016, of which 843,000 b/d were refined products and the remainder was crude oil. About 84% of total petroleum (775,000 b/d) went southbound from the Atlantic to the Pacific in 2016.

Some oil tankers, such as the ULCC (Ultra Large Crude Carrier) class tankers, can be nearly five times larger than the maximum capacity of the canal. To make the canal more accessible, the Panama Canal Authority, the body that operates the Canal, undertook an expansion program that was completed in June 2016. With the expansion, the Panama Canal Authority inaugurated a third set of locks that allows larger ships to transit the canal. This expansion was the first one since the canal was completed in 1914.

The canal expansion involved deepening and widening some portions of the canal and constructing an additional, larger set of locks. Unlike the old lock system, which had two lanes of side-by-side traffic, the new set of locks is one large lane and allows four transits per day, supplementing the 25 daily transits using the older lock system. The wider and deeper navigation channels and larger locks allow for the transit of larger vessels through the canal. The maximum vessel dimensions in the old lock system, known as Panamax vessels, limited tankers to those of approximately 300,000 to 500,000 barrels of capacity of petroleum products such as gasoline and diesel fuel. The newer lock system allow the larger Neopanamax vessels to transit the canal, with estimated petroleum product capacities of 400,000 to 600,000 barrels (Figure 8).

The expansion of the Panama Canal is not likely to affect crude oil and petroleum product flows in the future, with the exception of U.S. propane exports. Previously, the size limitations of the canal created logistical bottlenecks for U.S. propane exports travelling to markets in Asia, necessitating ship-to-ship transfers. The new, larger Panama Canal locks allow most Very Large Gas Carriers (VLGC), the type of ship that carries propane and other hydrocarbon gas liquids (HGL), to transit.

| thousand barrels per day | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|

| Panama Canal total flows | ||||||

| total oil | 768 | 813 | 863 | 877 | 1031 | 934 |

| crude oil | 121 | 120 | 92 | 133 | 134 | 79 |

| refined products | 647 | 693 | 771 | 744 | 897 | 855 |

| Panama Canal southbound flows | ||||||

| total oil | 609 | 696 | 719 | 701 | 826 | 785 |

| crude oil | 69 | 72 | 40 | 48 | 60 | 47 |

| refined products | 541 | 624 | 679 | 653 | 766 | 738 |

| Panama canal northbound flows | ||||||

| total oil | 158 | 117 | 144 | 176 | 205 | 149 |

| crude oil | 52 | 48 | 52 | 84 | 74 | 32 |

| refined products | 106 | 69 | 92 | 91 | 131 | 116 |

| Notes: Totals may not equal the sum of the components due to independent rounding. Data for the Panama Canal are by fiscal years (October 1 to September 30). Sources: U.S. Energy Information Administration analysis based on Lloyd’s List Intelligence, Panama Canal Authority (with EIA conversions).26 |

||||||

Trans-Panama Pipeline

The Trans-Panama Pipeline (TPP), operated by Petroterminal de Panama, S.A. (PTP), is located outside the former Canal Zone near the Costa Rican border. It runs from the port of Charco Azul on the Pacific coast to the port of Chiriqui Grande in Bocas del Toro, Panama, on the Caribbean Sea. The pipeline began operating in 1982 with the original purpose of facilitating crude oil shipments from Alaska's North Slope to refineries in the Caribbean and in the U.S. Gulf Coast. However, in 1996, the TPP was shut down as oil companies began shipping Alaskan crude oil along alternate routes. In August 2010, the flow of the TPP was reversed, and the pipeline now transports oil from the Caribbean to the Pacific.

In 2012, BP and PTP signed a seven-year transportation and storage agreement allowing BP to lease storage facilities located on the Caribbean and Pacific coasts of Panama and to use the pipeline to transport crude oil to U.S. West Coast refiners. According to PTP, BP has leased 5.4 million barrels of PTP's storage and committed to east-to-west shipments through the pipeline averaging 100,000 b/d. The route reduces the transport time and the costs of ships that have to travel around Cape Horn at the southern tip of South America to get to the U.S. West Coast.29 Shell, also reportedly signed a three-year agreement to lease capacity in early 2017, gaining access to storage and transshipment facilities, the pipeline network, and tanker docks for oil loading. According to Lloyd's List Intelligence, 111,000 b/d of crude oil was transported through the pipeline to the port of Charco Azul in 2016.

Danish Straits

The Danish Straits are a vital route for Russian seaborne oil exports to Europe.

The Danish Straits are a series of channels that connect the Baltic Sea to the North Sea. They are an important route for Russian seaborne oil exports to Europe. An estimated 3.2 million b/d of crude oil and petroleum products flowed through the Danish Straits in 2016.

Russia shifted a significant portion of its crude oil exports to its Baltic ports after opening the port of Primorsk in 2005. In 2011, Primorsk oil exports accounted for almost half of all exports through the Danish Straits, although the volume fell to 32% in 2016. A small amount of oil (less than 50,000 b/d), primarily from Norway and the United Kingdom, also flowed eastward to Scandinavian markets in 2016.

Cape of Good Hope

Although not a chokepoint, the Cape of Good Hope is a major global trade route. Crude oil flows around the Cape accounted for about 9% of all seaborne-traded oil.

The Cape of Good Hope, located on the southern tip of South Africa, is a significant transit point for oil tanker shipments around the globe. EIA estimates about 5.8 million b/d of seaborne-traded crude oil moved around the Cape of Good Hope in both directions in 2016. In 2015, crude oil transit around the Cape accounted for roughly 9% of global maritime trade of 5.1 million b/d.

In 2016, 4.3 million b/d of crude oil around the world moved eastbound, originating mostly from Africa (2.2 million b/d) and from South America and the Caribbean (1.6 million b/d). Eastbound crude oil flows were nearly all destined for Asian markets (4.1 million b/d). In the opposite direction, nearly all westbound flows originated from the Middle East (1.5 million b/d), mostly destined for the Americas, with the United States accounting for the majority of the total (75% of total flows). Europe was the destination for less than 12% of the flows.

The Cape of Good Hope is also an alternate sea route for vessels traveling westward that want to bypass the Gulf of Aden, Bab el-Mandeb Straits, and/or the Suez Canal. However, diverting vessels around the Cape of Good Hope increases costs and shipping time. For example, closure of the Suez Canal and the SUMED Pipeline would require oil tankers to divert around the Cape of Good Hope, adding approximately 2,700 miles to transit from Saudi Arabia to the United States, which would increase both costs and shipping time, according to the U.S. Department of Transportation. According to the International Energy Agency (IEA), shipping around Africa would add 15 days of transit to Europe and 8—10 days to the United States.

| million b/d | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|

| Total flows | 4.7 | 5.4 | 5.1 | 4.9 | 5.1 | 5.8 |

| Eastbound | 2.9 | 3.7 | 3.7 | 3.8 | 4.1 | 4.3 |

| Westbound | 1.8 | 1.7 | 1.4 | 1.1 | 1.0 | 1.5 |

| Notes: Totals may not equal the sum of the components due to independent rounding. Sources: U.S. Energy Information Administration analysis based on Lloyd’s List Intelligence |

||||||

Oil tanker sizes

Ships carrying crude oil and petroleum products are limited by size restrictions imposed by maritime oil chokepoints. The global crude oil and refined product tanker fleet uses a classification system to standardize contract terms, to establish shipping costs, and to classify vessels for chartering contracts. This system, known as the Average Freight Rate Assessment (AFRA) system, was established by Royal Dutch Shell six decades ago, and the London Tanker Brokers' Panel (LTBP), an independent group of shipping brokers, oversees the system.

AFRA uses a scale that classifies tanker vessels according to deadweight tons—a measure of a ship's capacity to carry cargo. The approximate capacity of a ship in barrels is determined using an estimated 90% of a ship's deadweight tonnage, which is multiplied by a barrel-per-metric-ton conversion factor specific to each type of petroleum product and crude oil, as liquid fuel densities vary by type and grade.

The smaller vessels on the AFRA scale—the General Purpose (GP) and Medium Range (MR) tankers—are commonly used to transport cargos of refined petroleum products over relatively shorter distances, such as from Europe to the U.S. East Coast. Their smaller size allows them to access most ports around the globe. A GP tanker can carry between 70,000 barrels and 190,000 barrels of motor gasoline (3.2-8 million gallons), and an MR tanker can carry between 190,000 barrels and 345,000 barrels of motor gasoline (8-14.5 million gallons).

Long Range (LR) class ships are the most common ships in the global tanker fleet, as they are used to carry both refined products and crude oil. These ships can access most large ports that ship crude oil and petroleum products. An LR1 tanker can carry between 345,000 barrels and 615,000 barrels of gasoline (14.5-25.8 million gallons) or between 310,000 barrels and 550,000 barrels of light sweet crude oil.

A large portion of the global tanker fleet is classified as AFRAMAX. AFRAMAX vessels are ships between 80,000 deadweight tons and 120,000 deadweight tons. This ship size is popular with oil companies for logistical purposes, and many ships have been built within these specifications. Because the AFRAMAX range exists somewhere between the LR1 and LR2 AFRA scales, the LTBP does not publish a freight assessment specifically for AFRAMAX vessels.

Over the history of AFRA, vessels grew in size, and newer classifications were added. The Very Large Crude Carrier (VLCC) and Ultra-Large Crude Carrier (ULCC) were added as the global oil trade expanded and larger vessels provided better economics for crude oil shipments. VLCCs are responsible for most crude oil shipments around the globe, including in the North Sea, home of the crude oil price benchmark Brent. A VLCC can carry between 1.9 million and 2.2 million barrels of a West Texas Intermediate (WTI) type crude oil.

-----

Earlier: