2018-03-07 14:15:00

IMF: QATAR IS BETTER

IMF - Qatar: Staff Concluding Statement for the 2018 Article IV Mission

Context

1. Qatar's economy continues to adjust successfully to lower hydrocarbon prices. Following the 2014 oil price shock, export receipts and government revenues fell significantly. The availability of fiscal buffers has allowed a gradual fiscal consolidation anchored mainly on reducing current expenditures, with the merger of ministries and cuts in subsidies. Tariffs of some utilities (water and electricity) have been increased and domestic fuel prices are now adjusted regularly in line with movements in international prices. The financial system remains sound. An infrastructure program in the amount of US$200 billion (equivalent to 121 percent of 2017 GDP) is underway to diversify the economy and prepare for the FIFA 2022 World Cup.

2. The direct economic and financial impact of the diplomatic rift between Qatar and some countries in the region is fading. While economic activity was affected, this has been mostly transitory and new trade routes were quickly established. The banking system has also adjusted. Following the rift, foreign financing (non‑resident deposits and inter-bank placements) and resident private sector deposits fell by about US$40 billion. This decline has been offset by liquidity injections by the central bank and public-sector deposits, particularly from Qatar Investment Authority (QIA). The decline in non‑resident liabilities of banks has abated, obviating the need for further support of the Qatar Central Bank (QCB) and QIA to the banking system, as banks mobilize funding from other (non‑GCC) sources. High frequency financial indicators, following the initial deterioration, are improving. The pegged exchange rate regime remains sustainable and the authorities have launched an investigation into possible exchange and bond markets manipulation in the wake of the rift.

Recent Developments and Outlook

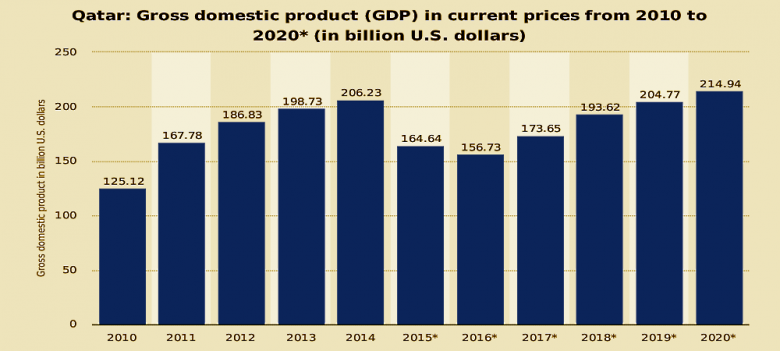

3. Macroeconomic performance remains resilient. Non-hydrocarbon real GDP growth is estimated to have moderated to about 4 percent in 2017, reflecting on-going fiscal consolidation and the impact of the diplomatic rift. A self-imposed moratorium on new projects in the North Oil Field until the second quarter of 2017 and the OPEC+ deal had restrained the growth of hydrocarbon output, resulting in overall real GDP growth of 2.1 percent in 2017. Headline inflation remains subdued, primarily due to lower rental prices. The real estate price index fell by 11 percent in 2017 (year-on-year basis) following cumulative increase of 53 percent during 2013‑16, reflecting increased supply of new properties and reduced effective demand. The fiscal deficit is estimated to have narrowed to about 6 percent in 2017 from 9.2 percent of GDP in 2016. The deficit has been financed by a combination of domestic and external financing. Public debt (estimated at 54 percent of GDP as at end-2017) remains sustainable, given the size of Qatar's sovereign wealth fund (SWF). The current account is improving in the context of increased oil and gas prices, and contraction in imports associated with lower economic growth. International reserves fell in response to capital outflows due to the unprecedented diplomatic rift, reaching about US$15 billion at end-December 2017. International reserves have been increasing in 2018, reaching US$18 billion by end-January 2018. Monetary conditions moderately tightened in 2017 due partly to monetary policy stance in the U.S., with higher interbank interest rates. However, the growth of private-sector credit was broadly stable. Qatar's banking sector remains healthy overall, reflecting high asset quality and strong capitalization. Macro-financial indicators are improving in 2018 compared to mid-2017; the CDS spreads have come down, stock market has recovered, and non-resident deposits have started to flow back in.

4. Medium-term macro-financial outlook is expected to remain broadly favorable. Overall, GDP growth of 2.6 percent is projected for 2018. While the implementation of the public investment program and the ease in the pace of fiscal consolidation would help support growth, the continuation of the diplomatic tensions could weigh on confidence. During 2019–23, growth is envisaged to average about 2.7 percent, supported by the authorities' intention to increase Liquid Natural Gas (LNG) production capacity by about 30 percent. Inflation is expected to peak at 3.8 percent in 2018—as the impact of the VAT being introduced during the second half of 2018 would mostly be felt in that year —before easing to 2.2 percent in the medium term. Authorities, in their assessment, indicated that inflation could be lower compared to staff's projection in 2018. Fiscal and external balances are projected to improve in the near and medium term due to continued expenditure restraint and higher hydrocarbon prices than in 2014–16. While government's ability to support banks' balance sheets remains strong and banks are expanding the sources of financing, the ongoing diplomatic rift and expected further monetary policy normalization in the U.S., which directly affects Qatar via the peg of the riyal to the dollar, could somewhat dampen private sector credit growth.

5. The main risks relate to the possibility of lower hydrocarbon prices, the implementation of planned fiscal measures, and uncertainty associated with the lingering impact of the diplomatic rift.

Macro-financial linkages can amplify the effects of lower hydrocarbon prices, as weaker government spending can lead to slower non-oil growth, weaker credit growth, and some deterioration in the quality of bank loan portfolios. However, the availability of government financial assets would help to contain the adverse impact of such a scenario. The authorities' stress tests indicate that banks would maintain high capital adequacy in the face of severe and protracted shocks.

Higher fiscal deficit, current account deficit, and public debt could emerge from delayed implementation of key fiscal measures.

Tighter global financial conditions could raise funding costs and market risks for the sovereign, banks, and corporates.

An escalation of the diplomatic rift could adversely affect external funding and growth. Although banks' balance sheets can withstand sizable shocks, financial buffers at the disposal of the authorities can provide additional support, if needed. Acceleration of structural reforms would be important to ensure that the economy remains competitive and attractive for investment.

Fiscal Policy

6. Continuing gradual fiscal consolidation over the medium term will help ensure adequate saving of the exhaustible hydrocarbon wealth for future generations. The non-hydrocarbon primary balance consistent with intergenerational equity (the benchmark non-hydrocarbon primary deficit calculated using the permanent income hypothesis) is the appropriate anchor for assessing the fiscal position in Qatar, given ample oil and gas reserves. With the fiscal consolidation that has already taken place during 2016–17, the estimated gap between the non‑hydrocarbon balance derived from this framework and the actual non‑hydrocarbon primary balance in 2017 was about 6 percentage points of non-hydrocarbon GDP. Gradual fiscal consolidation is appropriate in view of significant fiscal space (large fiscal and external buffers accumulated in the SWF, still favorable terms of external borrowing, and the need to avoid more pronounced slowdown in growth due to a more ambitious fiscal consolidation path). The authorities have the space to go even slower in the event of adverse shocks or if cyclical conditions warrant.

7. Effective prioritization and sequencing of fiscal reforms is important to preventing reform fatigue. In line with this approach, the 2018 budget continues with gradual fiscal consolidation, with emphasis on new tax measures (VAT and excises), fees for the use of government services, contained current expenditure, and efficient and higher capital expenditure. In the medium term, further fiscal consolidation is envisaged, including limiting the growth of the public wage bill and spending on good and services, and reduced public investment. Going forward, consideration could be given to wage reform, underpinned by restructuring based on well-designed and implemented public sector employment reforms in conjunction with reforming education and the labor market. Public employment reform is important to improving economic efficiency and supporting private sector-led growth. The direction of the energy and water price reforms is appropriate. Gradually reducing energy subsidies (water and electricity), while putting in place robust mechanisms to protect the most vulnerable segments of the population is important.

8. Planned fiscal efforts should be discussed in a medium-term fiscal framework with a clear medium-term objective. The authorities have formulated a medium-term fiscal framework (MTFF), with key macroeconomic assumptions. The focus should now be on preparing the medium-term budget framework (MTBF) by matching the MTFF with a bottom-up estimation of the costs of existing policy and integrating the MTBF in the annual budget process. Gradually turning the MTBF into a performance based medium-term expenditure framework would be especially useful.

9. Enhanced asset-liability management framework remains important. Deficit financing should avoid crowding out private sector credit growth and the appropriate mix between the various borrowing and investment options should be guided by a comprehensive asset/liability management framework that considers macro‑financial implications, including the impact on debt sustainability, domestic liquidity, credit to the economy, and central bank reserves. Total public debt as a ratio of GDP is projected to reach 54.6 percent of GDP in 2018, with external component of 21.6 percent of GDP. The authorities plan to use possible future fiscal surpluses in light of the evolution of oil prices to build up the reserves of QCB and increase asset holding of QIA.

Monetary, financial sector, and Exchange Rate Policies

10. The authorities continue to enhance the existing framework for liquidity management. Emphasis has been placed on greater coordination and information sharing between the central government, QCB, and the QIA. Further progress in upgrading liquidity management can be made by improving liquidity monitoring and forecasting. Efforts to further deepen domestic financial markets to promote saving and offer borrowing and investment opportunities remain important. While QCB liquidity injections and increased public-sector deposits have helped mitigate the funding pressures on Qatari banks in the wake of the diplomatic rift, the banking system has to adjust to a new funding model.

11. A robust regulatory framework and effective supervision have helped ensure the resilience of the financial system. The banking system is characterized by high loan concentrations—particularly real estate loans—and connected lending. The on-going efforts that focus on bolstering macro-prudential regulations, and strengthening consolidated supervision would help to prevent and mitigate systemic risks. QCB introduced a new loan-to-deposit requirement of 100 percent that came into effect in January 2018. QCB is further strengthening its financial sector surveillance to detect in a timely fashion emerging pressures, including those related to liquidity, real estate sector, the impact of U.S. monetary policy normalization, and the on-going diplomatic rift.

12. Basel IV, once adopted, will significantly increase risk-weights, thereby impacting banks' capital ratios, credit risk management, pricing, processes and disclosure. QCB could undertake an impact study of Basel IV on banks' capital adequacy ratios to inform the appropriate speed of its implementation. The rise of FinTech will create new challenges for financial sector regulators as well as opportunities for developing domestic financial markets and fostering innovation, which requires enhanced capacity in this area.

13. Efforts are ongoing to develop financial markets and strengthen their financial integrity. Deepening domestic financial markets, especially domestic government and corporate bond markets, should be a priority reform area to support non-hydrocarbon private sector growth. Developing financial markets, ensuring financial inclusion and fostering financial innovation (FinTech) that seeks to reach out to a broader base through cost-effective technology are a cornerstone of the authorities' Second Strategic Plan for the Financial Sector. The authorities are increasingly focusing on enhancing AML/CFT effectiveness and strengthening anti-corruption regimes. They are putting in place a comprehensive mechanism to implement targeted financial sanctions and managing risks posed by non‑profit organizations. In addition, priority is given to the combating of terrorist financing legal framework, and the assessment of national risks.

14. The currency peg remains appropriate. The peg to the U.S. dollar continues to serve Qatar well, providing a clear and credible monetary anchor. Nevertheless, the exchange rate regime should be periodically reviewed to ensure it remains appropriate as the economy moves towards a more diversified export structures. Staff's assessment suggests that the external position is moderately weaker than the level that would be consistent with sufficient saving of Qatar's exhaustible resource revenue. However, with gradual fiscal adjustment, the estimated current account gap could be closed in the medium term. Reserves are considered to be broadly adequate in view of the size of the sovereign wealth fund.

Private Sector Development, Economic Diversification and Macroeconomic Statistics

15. The Qatari economy remains competitive, though there are certain areas that deserve attention. Qatar has fallen to 25th place (out of 137) in the World Economic Forum's Global Competitiveness Index (2017–18), down from 18 th in 2016–17. Nonetheless, it still ranks ahead of most emerging markets, a reflection of a stronger infrastructure base. While recognizing measurement limitations, the World Bank's Ease of Doing Business Index ranks Qatar 83rd out of 190 countries, which is below the GCC average on account of a number of indicators such as access to credit and contract enforcement. Though Qatar is doing better than some GCC countries in terms of educational outcomes, there is considerable room for improvement.

16. Authorities are advancing a structural reform agenda to improve the business environment, with the diplomatic rift having provided impetus to speed up such reforms. The diplomatic rift has acted as a catalyst for enhancing domestic food production and reducing reliance on a small group of countries. Though a welcome move, self-reliance should not translate into import-substitution policies with attendant inefficiencies, but rather be used to tap into regional and global value chains. Qatar's privatization initiatives in some sectors, for example health and education, are steps in the right direction. Authorities also plan to set up special economic zones (SEZs), which are expected to stimulate diversification efforts and encourage FDI. In establishing SEZs, special attention should be paid to designing tax incentives and labor policies to avert market distortions. In addition, such schemes should also be cognizant of the objective to reduce fiscal dependence on hydrocarbons. Qatar could make further progress in enhancing contract enforcement by reducing the time and cost associated with settling commercial disputes and by strengthening the insolvency mechanism. The Supreme Council for Economic Affairs and Investment has approved the second national development strategy that would help address some of these challenges. Work is on-going on ensuring majority foreign ownership of companies. In addition, Qatar has announced a visa-free entry program for 80 nationalities to stimulate tourism, approved a draft law to grant permanent residency to foreigners who provide "outstanding services to Qatar", put in place a worker dispute settlement committee, and a trust fund in case workers face bankruptcy. In addition, the authorities are considering establishing a minimum wage under the International Labor Organization (ILO) framework and a new law to protect expatriate labor providing domestic help.

17. The authorities continue to enhance macroeconomic statistics. Progress is being made in conducting quarterly investment survey, compiling fiscal data according to the GFSM 2001, and subscribing to the Special Data Dissemination Standard (SDSS). QCB expressed its intention to compile and disseminate the Reserves Data Template fully in line with the Guidelines for a Data Template. Enhanced fiscal reporting (frequency, timeliness, and analysis), including of government financial transactions would help strengthen accountability and transparency. The authorities should endeavor to disseminate the financing components of central government operations, central government domestic debt, and external debt.

18. The mission team is grateful for the authorities' productive and candid discussions, hospitality, and close collaboration.

-----

Earlier:

2018, January, 31, 10:45:00

SAUDI - QATAR COMPETITIONBLOOMBERG - Oil exports from Qatar, one of OPEC’s smaller crude producers, to Japan last year slumped by almost a quarter to its lowest level since 1990, while shipments from giant supplier Saudi Arabia grew 8.1 percent, boosting its market share in the Asian nation to a record. Over in South Korea, imports from Qatar sank 26 percent to the least in seven years.

|

2018, January, 4, 12:25:00

QATARGAS & RASGAS MERGERTOGY - The merger of the world’s largest LNG producers, Qatargas and RasGas, is complete, and the new entity, called Qatargas, has started operations, parent company Qatar Petroleum (QP) announced

|

2017, July, 5, 12:15:00

QATAR SHOW STRENGTHQatar mounted what appeared to be a show of strength on Tuesday, when the state-owned Qatar Petroleum announced plans to raise liquefied natural gas capacity by 30 percent. Its immediate effect will be to worsen a glut on the LNG market where Australia, the United States and Russia vie.

|

2017, June, 24, 09:45:00

RUSSIA - QATAR COMPETITIONQatar and Russia have long been rivals in global gas markets. Qatar's supplies came under the spotlight in the past month after Saudi Arabia cut economic and diplomatic ties, in a move ratcheting up a wider violent and diplomatic conflict in the Middle East.

|

2017, June, 7, 18:00:00

QATAR WILLING TO SPEAK"We are willing to sit and talk," Qatari Foreign Minister Sheikh Mohammed bin Abdulrahman al-Thani told CNN late on Tuesday. He said his country was "protecting the world from potential terrorists".

|

2017, April, 12, 18:40:00

QATAR'S GDP UP TO 2.7%Lower hydrocarbon prices have adversely impacted macroeconomic performance. Growth has slowed despite still resilient non-hydrocarbon activity. Real GDP growth of 2.7 percent is estimated for 2016. Inflation remained low despite subsidy cuts, averaging about 2.7 percent in 2016.

|

2017, January, 26, 18:50:00

QATAR'S INVESTMENT TO RUSSIAAbullah bin Mohammed Al Thani, the fund’s chief executive, said it would invest a further $2bn on top of $500m of existing investments in the country. Some of the investments would be made jointly with the $10bn sovereign Russian Direct Investment Fund, its partner in a deal last summer for St. Petersburg’s airport, he added. |