2018-03-16 10:30:00

OIL DEMAND GROWTH - 2018: 1.5 MBD

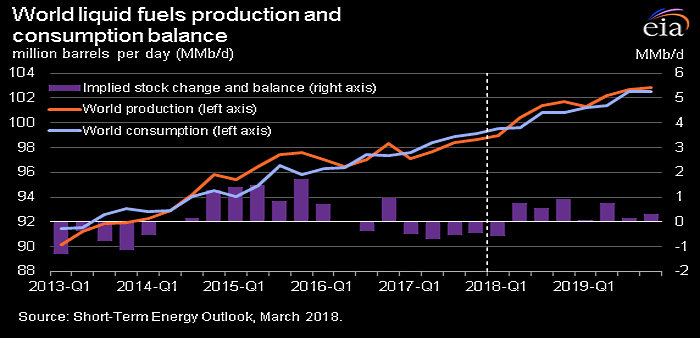

IEA - The past month has been relatively uneventful in terms of data changes, apart from an increase to our demand growth estimate. Crude oil prices are slightly lower than last month, and have generally been relatively stable for several weeks. Even so, the value of Brent crude oil is still averaging close to $67/bbl in 2018, which is about 20% higher than in the early part of last year.

Looking at demand, our estimate for global growth in 2018 has increased by 90 kb/d taking it up to 1.5 mb/d. Although this is a modest revision, it is interesting that provisional data suggests very strong starts to the year in China and India, which, taken together, accounted for nearly 50% of global demand growth in 2017. Cold weather in some parts of the northern hemisphere in January-February saw an increase in heating demand.

On supply, new and revised data shows very little change in the outlook versus last month. Although US production was lower than expected in December, there is no change to our overall 2017 number neither to our outlook for 2018 that expects crude output there to grow by 1.3 mb/d. We retain our view that total non-OPEC production grew by 760 kb/d last year and that it will surge by 1.78 mb/d this year. Within the OPEC countries, the biggest risk factor is, and will likely remain, Venezuela. Our estimate for February shows output down again, by 60 kb/d. Other countries with a risk factor include Libya, and, to a lesser extent, Nigeria. In Libya, we saw another modest supply gain in February to 1.02 mb/d and, although stability cannot be taken for granted, it appears that the frequency and severity of production interruptions is declining and higher rates of output are being maintained. Taking OPEC as a whole, quota compliance in February was 147%, but even if Venezuela's production were at its allocated level, the group's compliance would still be close to 100%.

Stocks, and specifically OECD stocks, remain the most-cited indicator of oil market re-balancing. In this Report, we note that in January they increased month-on-month for the first time since July. However, the increase of 18 mb was half the average level for January seen in the past five years. Indeed, the surplus of total OECD stocks against the five-year average fell for the ninth successive month to 50 mb, with products showing a very small deficit.

In the meantime, market re-balancing is clearly moving ahead with key indicators – supply and demand becoming more closely aligned, OECD stocks falling close to average levels, the forward price curve in backwardation at prices that increasingly appear to be sustainable – pointing in that direction. In our chart, we assume for scenario purposes that OPEC production remains flat for the rest of 2018, and on this basis there will be a very small stock build in 1Q18 with deficits in the rest of the year. With supply from Venezuela clearly vulnerable to an accelerated decline, without any compensatory change from other producers it is possible that the Latin American country could be the final element that tips the market decisively into deficit.

Moving further into the future, we highlighted how in 2017 discoveries of new resources fell to a record low of only 4 bn barrels while 36 bn barrels were actually produced. In 2018 investment spending is likely to grow only by 6% having barely increased at all in 2017. To 2020, production increases from non-OPEC countries are by themselves enough to meet demand growth. After that time, the pace of growth from these countries is less certain, and the market might well need the supplies currently being held off the market by leading producers.

-----

Earlier:

2018, January, 26, 12:35:00

СПРОС НА НЕФТЬ: 100 МЛН.МИНЭНЕРГО РОССИИ - «На сегодня 100 млн баррелей в сутки - общемировой спрос на нефть, а сланцевая нефть- это всего 5,7 млн барр в сутки. Это лишь один из способов удовлетворения спроса рынка».

|

2018, January, 26, 12:30:00

РЫНОК БУДЕТ СБАЛАНСИРОВАНМИНЭНЕРГО РОССИИ - «Надеюсь, что к концу 2018 года рынок сбалансируется. Действия ОПЕК+ показали, что в будущем мы можем применять подобные механизмы. При этом мы настроены не только продолжать сотрудничество в рамках сокращения, но и проводить раз в полгода или год совместные консультации стран — участниц сделки с привлечением других государств».

|

2018, January, 24, 12:15:00

СОГЛАШЕНИЕ ВЫПОЛНЕНО НА 107%МИНЭНЕРГО РОССИИ - АЛЕКСАНДР НОВАК: СОГЛАШЕНИЕ ОПЕК+ ПО ИТОГАМ 2017 ГОДА ВЫПОЛНЕНО НА 107%

|

2017, December, 4, 23:15:00

СОТРУДНИЧЕСТВО С ОПЕКМИНЭНЕРГО РОССИИ - ОПЕК оставляет в силе решения, принятые 30 ноября 2017 года; в «Декларацию о сотрудничестве» вносится поправка, согласно которой ее срок действия охватывает весь 2018 год с января по декабрь 2018 года, при этом входящие и участвующие в кооперации не входящие в ОПЕК страны обязуются обеспечить полное и своевременное исполнение условий «Декларации о сотрудничестве» и скорректировать объемы добычи в соответствии с достигнутыми на добровольной основе договоренностями.

|

2017, December, 1, 13:00:00

СОГЛАШЕНИЕ: МЕНЬШЕ НЕФТИМИНЭНЕРГО РОССИИ - «Мы успешно и конструктивно провели переговоры по продлению сделки. Мы удовлетворены результатами балансировки рынка, сокращением излишков нефти и нефтепродуктов, снижением волатильности цен, а также возврату инвестиционной активности в отрасли. В тоже время мы также единодушно подтвердили то, что мы находимся лишь в середине пути, и для того, чтобы достичь окончательной цели по балансировке рынка, нам нужно продолжить совместные усилия».

|

2017, November, 27, 20:15:00

РОССИЯ ПОДДЕРЖИВАЕТ СОКРАЩЕНИЕМИНЭНЕРГО РОССИИ - «Мы видим, что с рынка ушло примерно 50% излишком запасов нефти, мы видим, что цена сбалансировалась и вышла на достаточно приемлемый уровень в районе 60 и выше долларов за баррель марки Brent, инвестиции начали уже в 17-м году расти, а до этого они 15-16-й год падали. Тем не менее, мы не достигли еще до конца цели по балансировке рынка, и сегодня практически все выступают за то, что необходимо продлить сделку дополнительно для того, чтобы достичь окончательных целей. В принципе, Россия тоже поддерживает такие предложения, рассматриваются разные варианты».

|

2017, November, 27, 20:05:00

OIL SUPPLY & DEMANDBLOOMBERG - Global crude inventories are declining and supply and demand are in balance, according to the head of Saudi Aramco, while the United Arab Emirates energy minister said U.S. shale oil doesn’t threaten OPEC’s efforts to support the market. |