2017-10-16 11:55:00

U.S. ECONOMY UP

FRB - The U.S. Economy and Monetary Policy

Chair Janet L. Yellen

Economic activity in the United States has been growing moderately so far this year, and the labor market has continued to strengthen. The terrible hurricanes that hit Texas, Florida, Puerto Rico, and our neighbors in the Caribbean caused tremendous damage and upended many lives, and our hearts go out to those affected. While the effects of the hurricanes on the U.S. economy are quite noticeable in the short term, history suggests that the longer-term effects will be modest and that aggregate economic activity will recover quickly.

Starting with the labor market, through August, payroll job gains averaged 170,000 per month this year, down only a little from the average pace of gains in 2016 and still well above estimates of the pace necessary to absorb new entrants to the labor force. In September, payrolls were reported to have declined 33,000, but that weakness reflected the effects of Hurricane Irma, which hit Florida during the reference week for the September labor market surveys. I would expect employment to bounce back in subsequent months as communities recover and people return to their jobs. Other aspects of the jobs report for September were strong. The unemployment rate, which seems not to have been noticeably affected by the hurricanes, declined further to 4.2 percent, down about 1/2 percentage point from the end of 2016 and below the median of Federal Open Market Committee (FOMC) participants' estimates of its longer-run normal level. Labor force participation continues to strengthen relative to a downward trend that reflects, in part, the aging of the population. Other labor market indicators, including the rates of job openings and the number of people who voluntarily quit their jobs, also point to strength.

Wage indicators have been mixed, and the most recent news, on average hourly earnings through September, was encouraging. On balance, wage gains appear moderate, and the pace seems broadly consistent with a tightening labor market once we account for the disappointing productivity growth in recent years.

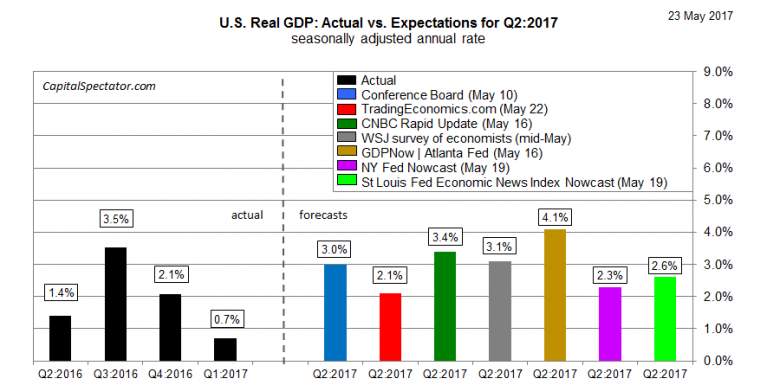

I expect the labor market to strengthen further as economic growth continues. The hurricanes will likely result in some hit to GDP growth in the third quarter but a rebound thereafter, and smoothing through those movements, I'm expecting growth that continues to exceed potential in the second half of the year. The latest projections from FOMC participants have a median of 2-1/2 percent GDP growth this year. Growth of consumer spending has been supported by the ongoing job gains and relatively high levels of household wealth and consumer sentiment. Business investment has strengthened this year following surprising weakness in 2016. The faster gains partly reflect an upturn in investment in the energy sector as oil prices have firmed. But the gains have been broader than that, and some measures of business sentiment remain quite strong. Exports also have risen this year, as growth abroad has solidified and the exchange value of the dollar has declined somewhat. My fellow FOMC participants and I perceive that risks to global growth have receded somewhat and expect growth to continue to improve over the near term.

The biggest surprise in the U.S. economy this year has been inflation. Earlier this year, the 12-month change in the price index for personal consumption expenditures (PCE) reached 2 percent, and core PCE inflation reached 1.9 percent. These readings seemed consistent with the view that inflation had been held down by both the sizable fall in oil prices and the appreciation of the dollar starting around mid-2014, and that these influences have diminished significantly by this year. Accordingly, inflation seemed well on its way to the FOMC's 2 percent inflation objective on a sustainable basis.

Inflation readings over the past several months have been surprisingly soft, however, and the 12-month change in core PCE prices has fallen to 1.3 percent. The recent softness seems to have been exaggerated by what look like one-off reductions in some categories of prices, especially a large decline in quality-adjusted prices for wireless telephone services. More generally, it is common to see movements in inflation of a few tenths of a percentage point that are hard to explain, and such "surprises" should not really be surprising. My best guess is that these soft readings will not persist, and with the ongoing strengthening of labor markets, I expect inflation to move higher next year. Most of my colleagues on the FOMC agree. In the latest Summary of Economic Projections, my colleagues and I project inflation to move higher next year and to reach 2 percent by 2019.

To be sure, our understanding of the forces that drive inflation is imperfect, and we recognize that this year's low inflation could reflect something more persistent than is reflected in our baseline projections. The fact that a number of other advanced economies are also experiencing persistently low inflation understandably adds to the sense among many analysts that something more structural may be going on. Let me mention a few possibilities of more fundamental influences.

First, given that estimates of the natural rate of unemployment are so uncertain, it is possible that there is more slack in U.S. labor markets than is commonly recognized, which may be true for some other advanced economies as well. If so, some further tightening in the labor market might be needed to lift inflation back to 2 percent.

Second, some measures of longer-term inflation expectations have edged lower over the past few years in several major economies, and it remains an open question whether these measures might be reflecting a true decline in expectations that is broad enough to be affecting actual inflation outcomes.

Third, our framework for understanding inflation dynamics could be misspecified in some way. For example, global developments--perhaps technological in nature, such as the tremendous growth of online shopping--could be helping to hold down inflation in a persistent way in many countries. Or there could be sector-specific developments--such as the subdued rise in medical prices in the United States in recent years--that are not typically included in aggregate inflation equations but which have contributed to lower inflation. Such global and sectoral developments could continue to be important restraining influences on inflation. Of course, there are also risks that could unexpectedly boost inflation more rapidly than expected, such as resource utilization having a stronger influence when the economy is running closer to full capacity.

In this economic environment, with ongoing improvements in labor market conditions and softness in inflation that is expected to be temporary, the FOMC has continued its policy of gradual policy normalization. As the Committee announced after our September meeting, we are initiating our balance sheet normalization program this month. That program, which was described in the June Addendum to the Policy Normalization Principles and Plans, will gradually scale back our reinvestments of proceeds from maturing Treasury securities and principal payments from agency securities. As a result, our balance sheet will decline gradually and predictably. By limiting the volume of securities that private investors will have to absorb as we reduce our holdings, the caps should guard against outsized moves in interest rates and other potential market strains.

Changing the target range for the federal funds rate is our primary means of adjusting the stance of monetary policy. Our balance sheet is not intended to be an active tool for monetary policy in normal times. We therefore do not plan on making adjustments to our balance sheet normalization program. But, of course, as we stated in June, the Committee would be prepared to resume reinvestments if a material deterioration in the economic outlook were to warrant a sizable reduction in the federal funds rate.

Also at our September meeting, the Committee decided to maintain its target for the federal funds rate. We continue to expect that the ongoing strength of the economy will warrant gradual increases in that rate to sustain a healthy labor market and stabilize inflation around our 2 percent longer-run objective. That expectation is based on our view that the federal funds rate remains somewhat below its neutral level--that is, the level that is neither expansionary nor contractionary and keeps the economy operating on an even keel. The neutral rate currently appears to be quite low by historical standards, implying that the federal funds rate would not have to rise much further to get to a neutral policy stance. But we expect the neutral level of the federal funds rate to rise somewhat over time, and, as a result, additional gradual rate hikes are likely to be appropriate over the next few years to sustain the economic expansion. Indeed, FOMC participants have built such a gradual path of rate hikes into their projections for the next couple of years.

Of course, policy is not on a preset course. I have spoken about some of the uncertainties associated with the inflation outlook in particular, and we will be paying close attention to the inflation data in the months ahead. But uncertainty about the outlook is by no means limited to inflation. As always, the Committee will adjust the stance of monetary policy in response to incoming economic information and the evolution of the economic outlook to achieve its objectives of maximum employment and stable prices. Moreover, we are mindful of the possibility that shifting expectations concerning the path of U.S. policy can lead to spillovers to other economies via financial markets and the value of the dollar. We remain committed to communicating as clearly and effectively as possible to help mitigate the risk of sudden changes in the policy outlook among market participants that could spur unintended effects in global financial markets.

-----

Earlier:

2017, October, 13, 12:50:00

U.S. OIL FOR ASIAA fresh wave of North American crude cargoes could reach the Far East in the coming months, with an estimated 6 million barrels or more of light sweet US grades loading in November expected to find a home in Asia as regional end-users step up efforts to find cheaper feedstocks amid sustained strength in the Middle Eastern crude complex, Asian trade sources said.

|

2017, October, 6, 12:35:00

U.S. DEFICIT DOWN TO $42.4 BLNThe U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that the goods and services deficit was $42.4 billion in August, down $1.2 billion from $43.6 billion in July, revised. August exports were $195.3 billion, $0.8 billion more than July exports. August imports were $237.7 billion, $0.4 billion less than July imports.

|

2017, September, 29, 12:25:00

U.S. HIGHEST PELROLEUM DEMANDTotal petroleum deliveries in August moved up by 1.3 percent from August 2016 to average 20.5 million barrels per day. These were the highest August deliveries in 10 years, since 2007. Compared with July, total domestic petroleum deliveries, a measure of U.S. petroleum demand, decreased 0.6 percent. For year-to-date, total domestic petroleum deliveries moved up 1.3 percent compared to the same period last year.

|

2017, September, 29, 12:20:00

RUSSIA INFLUENCES U.S.“In light of Facebook’s disclosure of over $100,000 in social media advertising associated with Russian accounts focused on the disruption and influence of US politics through social media, it is likely that Russia undertook a similar effort using social media to influence the US energy market,”

|

2017, September, 27, 13:35:00

U.S. WANT OIL MARKETIf the US were to reimpose nuclear sanctions on Iran, the Trump administration would do so in a way that would have minimal impact on the global oil market, a senior State Department official said Tuesday.

|

2017, September, 22, 08:30:00

U.S. FEDERAL FUNDS RATE: 1 - 1.25%In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1 to 1-1/4 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

|

2017, September, 18, 12:10:00

U.S. INDUSTRIAL PRODUCTION DOWN 0.9%Industrial production declined 0.9 percent in August following six consecutive monthly gains. Hurricane Harvey, which hit the Gulf Coast of Texas in late August, is estimated to have reduced the rate of change in total output by roughly 3/4 percentage point. The index for manufacturing decreased 0.3 percent; storm-related effects appear to have reduced the rate of change in factory output in August about 3/4 percentage point. The manufacturing industries with the largest estimated storm-related effects were petroleum refining, organic chemicals, and plastics materials and resins.

|