2017-10-04 23:40:00

WBG WANT ASIA

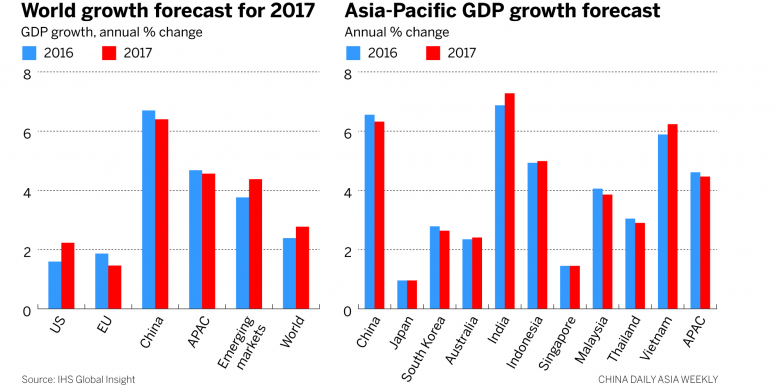

WBG - Improved global growth prospects and continued strong domestic demand underpin a positive outlook for the developing economies of East Asia and the Pacific. Stronger growth in advanced economies, a moderate recovery in commodity prices, and a recovery in global trade growth, are the favorable external factors that will support the economies of developing East Asia and Pacific to expand by 6.4 percent for 2017.

The uptick in growth in 2017 relative to earlier expectations reflects stronger than expected growth in China, at 6.7 percent, the same pace as in 2016. In the rest of the region, including the large Southeast Asian economies, growth in 2017 will be slightly faster at 5.1 percent in 2017 and 5.2 percent in 2018, up from 4.9 percent in 2016.

Several external and domestic risks could impact this positive outlook. Economic policies in some advanced economies remain uncertain, while geopolitical tensions centered on the region have increased. Monetary policies in the U.S. and the Euro Area could be tightened more quickly than expected. Many countries in the region have high levels of private sector debt while fiscal deficits remain high or are on the rise.

China's gradual rebalancing away from investment and towards domestic consumption is expected to continue, with growth projected to slow to around 6.4 percent in 2018.

Thailand and Malaysia are expected to grow more rapidly than expected, due to stronger exports, including tourism, for the former, and increased investment in the latter. Gains in real wages are fueling strong consumption in Indonesia, and a rebound in agriculture and manufacturing is boosting growth in Vietnam. In the Philippines, the economy is projected to expand at a slightly slower pace than in 2016, partly due to slower than expected implementation of public investment projects.

The outlook for smaller countries is mixed. Mongolia and Fiji are expected to fare better in 2017-2018. Mongolia's macroeconomic stabilization program is encouraging new foreign direct investment in mining and transport. Fiji's growth will be supported by reconstruction from Cyclone Winston. Growth in Cambodia and Lao PDR is moderating compared to 2016, but its pace remains higher than other countries in the region; trade and FDI in Cambodia and expansion of the power sector in Lao PDR are the main drivers.

Expanding tourism, low world commodity prices, high levels of revenue from fishing fees, and rising construction activity are supporting moderate GDP growth rates in most of the small Pacific Islands. In the longer term, reforms in tourism, labor mobility, fisheries, and the knowledge economy have the potential to lead to significantly higher incomes, employment, and government revenue.

To maintain resilience against risks, the report calls for a move away from measures aimed at short-term growth towards policies that address financial sector and fiscal vulnerabilities. These measures include: strengthening supervision and prudential regulation in countries experiencing rapid growth in private-sector credit and debt; reforming tax policies and administration to help boost revenue collection; and being ready to tighten monetary policy if warranted by the pace of interest rate increases in advanced economies.

Structural reform priorities differ across countries. Sustained reforms of the state-owned enterprise sectors in China and Vietnam can improve growth prospects. The Philippines, Thailand, Lao PDR and Cambodia will benefit from continued improvements in public investment management systems to support expanding public infrastructure programs. In Indonesia, liberalizing the regulations for foreign investment remains important.

The potential that tourism development and deeper regional integration offer to offset the risks of protectionism. Growth in tourism, if well managed, has the potential to yield substantial benefits to the region, including for the Pacific Island Countries. The ASEAN Economic Community offers one avenue for promoting further regional integration, including by further liberalizing trade in services and reducing non-tariff barriers.

Despite success in reducing poverty, high and rising inequality is a growing concern, as are falling mobility and growing economic insecurity. For lasting inclusive growth, measures to reduce extreme poverty must be accompanied by policies that broaden access to quality services and more productive jobs, and stronger social protection systems that reduce the consequences of adverse shocks.

-----

Earlier:

September, 13, 15:10:00

IMF: SOUTHEAST ASIA'S TRANSFORMATIONIMF - When we think about Asia’s economic future, we know that this future is being built on strong foundations—on the richness and diversity of its cultures, on the incredible energy and ingenuity of the people who have changed the world by transforming their own economies. China and India have been driving the greatest poverty reduction in human history by creating the world’s largest middle classes. In a single generation, Vietnam has moved from being one of the world’s poorest nations to being a middle-income country. |

August, 28, 19:45:00

IMF: BAHRAIN'S VULNERABILITY UPBahrain’s fiscal and external vulnerabilities have increased in the wake of the oil price decline. Overall GDP grew 3 percent in 2016, supported by strong growth of 3.7 percent in the non-oil sector aided by the implementation of GCC-funded projects. Average inflation remained moderate at 2.8 percent. Bank deposit and private sector credit growth slowed. The banking sector remains well capitalized and liquid. Despite the implementation of significant fiscal adjustment, lower oil prices meant that the overall fiscal deficit reached nearly 18 percent of GDP and government debt rose to 82 percent of GDP. The current account deficit widened to 4.7 percent. International reserves have declined. |

August, 16, 09:10:00

IMF HAS IRAQTo strengthen financial sector stability, Directors encouraged the authorities to take measures to bolster supervision, and move forward with plans to restructure the statemdash;owned banks that dominate the banking system. They also encouraged strengthening the legal framework of the Central Bank, eliminating a remaining exchange restriction and a multiple currency practice, and accelerating implementation of AML/CFT and antimdash;corruption measures. Directors considered that the peg to the U.S. dollar, which provides a key anchor to the economy, remains appropriate. |

August, 3, 12:30:00

WORLD BANK BUYS COUNTRIESWorld Bank Group commitments to help developing countries take on poverty and boost opportunity reached nearly $59 billion in loans, grants, equity investments and guarantees in fiscal year 2017. |

July, 17, 13:40:00

IMF WANT BRAZILDirectors observed that the financial sector has remained sound despite the severe stresses. To make the system more robust, they encouraged actions to further strengthen financial safety nets through enhanced monitoring and an improved crisis management framework. Directors underscored the need for continued vigilance and close monitoring of the health of the corporate sector and its impact on the banking system. |

April, 6, 18:30:00

WBG BOUGHT UKRAINE: $10 BLNThe World Bank’s current investment project portfolio in Ukraine amounts to about US$2.8 billion. Investments support improving basic public services that directly benefit ordinary people in areas such as water supply, sanitation, heating, power, roads, social protection and healthcare, as well as private sector development. Since Ukraine joined the World Bank in 1992, the Bank’s commitments to the country have totaled over US$10 billion in about 70 projects and programs. |

March, 27, 18:35:00

WBG WANTS VIETNAMThe World Bank’s current portfolio in Vietnam consists of 49 operations, worth a total of 9.5 billion USD supporting infrastructure, agriculture, human development and improvement in economic and financial sector management. Support to infrastructure includes transport, energy, water and sanitation, and irrigation. |

November, 30, 18:50:00

IMF: EXTERNAL RISKS FOR RUSSIAThe expected fiscal consolidation and the subdued nature of the recovery are putting in place the conditions for the central bank to resume, in due course, monetary policy easing in a manner consistent with the 4 percent inflation target. However, the pace of easing should take into account the presence of external risks and the need to build credibility under the newly introduced inflation targeting regime. |

November, 9, 18:55:00

WBG WANTS MORE EGYPTThe World Bank welcomes Egypt’s recent economic and social reform measures including the floatation of the currency, measures to boost investment especially in Upper Egypt, adjusting energy prices to reflect market conditions, and strengthening the social safety net. |