2018-10-12 11:30:00

OPEC: OIL DEMAND UP BY 1.54 MBD

OPEC - Monthly Oil Market Report

Oil Market Highlights

Crude Oil Price Movements

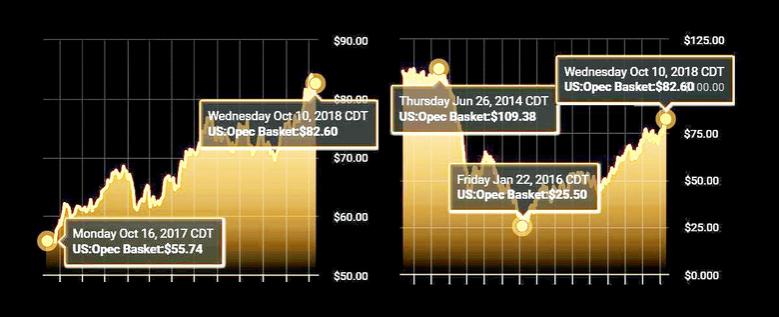

In September, the OPEC Reference Basket increased sharply by almost 7%, or $4.92 m-o-m, to average $77.18/b the highest since October 2014. Crude oil futures prices also increased for the month, mainly supported by geo-political tension, growing concerns over a shortage in global oil supply and low US oil inventories, particularly in Cushing, Oklahoma. ICE Brent was $5.27 higher at $79.11/b compared with the previous month, NYMEX WTI was up $2.24 at $70.08/b and DME Oman increased by $6.08 to $78.75/b.

Year-to-date (y-t-d), ICE Brent was $20.23 higher at $72.74/b, NYMEX WTI increased by $17.43 to $66.79/b and DME Oman was up $19.25 at $70.48/b, compared to the same period a year earlier. The Brent-WTI spread widened to average $9.02/b for the month. Speculative net long positions ended mixed, significantly higher for ICE Brent, while lower for NYMEX WTI. As for market structure, the backwardation in Dubai expanded sharply in September, while that of WTI eased. The Brent market structure flipped into backwardation amid concerns over a shortage global oil supply. Apart from Asian grades, the global sour discount to sweet crudes decreased due to an anticipated tightening of sour crude and high availability of sweet crude.

World Economy

The global economic growth forecast for 2018 was revised down slightly by 0.1 percentage point (pp) to now stand at 3.7%, due mainly to slowing growth in some emerging and developing economies. The 2019 forecast remains unchanged at 3.6%. In the OECD, growth in the US is assessed unchanged at 2.9% in 2018 and 2.5% in 2019 and Euro-zone growth remains at 2.0% for 2018 and 1.9% for 2019. GDP growth in Japan remains at 1.1% in both 2018 and 2019. In the non-OECD countries, India's and China's growth forecasts remains unchanged at 7.6% and 6.6% in 2018, respectively, and 7.4% and 6.2%, respectively, in 2019. Growth in Brazil was revised down by 0.1 pp to 1.1% in 2018, and by 0.2 pp to 1.8% in 2019. Russia's GDP growth forecast is unchanged to stand at 1.6% in 2018 and 1.7% in 2019.

World Oil Demand

In 2018, world oil demand growth is estimated at 1.54 mb/d, following a downward revision of around 80 tb/d from the previous month's assessment, mainly to reflect the most up-to-date data in OECD Europe and the Middle East, as well as the latest developments in the economies of in Latin America. Total oil demand for the year is now pegged at 98.79 mb/d. In 2019, world oil demand growth is forecast at 1.36 mb/d, down by around 50 tb/d from last month's projections, mainly reflecting adjustments in the economic projections for Turkey, Brazil and Argentina. As a result, total world oil demand is anticipated to reach 100.15 mb/d.

Oil demand growth is projected to be driven by Other Asia, led by India, followed by China, and OECD America. In 2019, OECD demand is forecast to grow by 0.25 mb/d, while non-OECD countries will drive oil demand growth by adding an estimated 1.11 mb/d.

World Oil Supply

Non-OPEC oil supply growth in 2018 is estimated at 2.22 mb/d, an upward revision of 0.20 mb/d from the previous month's assessment. The US, Canada, Kazakhstan and Brazil are expected to be the main drivers for y-o-y growth, while Mexico, Norway, Indonesia and Vietnam will show the largest declines. Total non-OPEC supply for 2018 is now estimated at 59.77 mb/d. Non-OPEC oil supply growth in 2019 is forecast at 2.12 mb/d, representing a downward revision of around 0.03 mb/d from last month's projections. The US, Brazil and Canada are the main growth drivers, while Mexico, Norway, Indonesia and Vietnam are expected to see the largest declines. The 2019 non-OPEC supply forecast remains subject to many uncertainties, with potential skewed to the upside. Non-OPEC supply is forecast to average 61.89 mb/d for the year.

OPEC NGLs in 2018 and 2019 are expected to grow by 0.12 mb/d and 0.11 mb/d to average 6.36 mb/d and 6.47 mb/d, respectively. In September, OPEC crude oil production increased by 132 tb/d to average 32.76 mb/d, according to secondary sources.

Product Markets and Refining Operations

Refinery margins in all the main trading hubs weakened in September, on retreating demand further exacerbated by nature-related events, despite the onset of peak refinery maintenance season. In the US, high refinery runs have kept product inventories well sustained fuelling bearish sentiment and thus softening the product market. In Europe, product markets lost ground, mostly pressured by gasoline, naphtha and fuel oil weakness, along with high feedstock costs, despite support from planned and unplanned outages reported during the month. In Asia, losses at the top and bottom of the barrel were partially offset by support from rising retail fuel prices due to a tightening gasoil market.

Tanker Market

Dirty tanker market sentiment was mixed in September. On average, dirty tanker freight rates were up by 4% from the month before, as a result of higher rates for Suezmax and Aframax, while VLCC rates remained flat. The overall dirty tanker market continued to suffer from an oversupply of ships, which mostly pressured freight rates. Relative gains were achieved in the Suezmax and Aframax classes due to the hurricane season, in addition to transit and port delays in several areas. Average clean tanker spot freight rates were also slightly positive, however gains were limited.

Stock Movements

Preliminary data for August showed that total OECD commercial oil stocks rose by 14.2 mb m-o-m to stand at 2,841 mb. This was 165 mb lower than the same time one year ago, and 47 mb below the latest five-year average. Crude stocks indicated a deficit of 6 mb, while products stocks witnessed a deficit of 41 mb. However, OECD commercial stocks remain 271 mb above the January 2014 level. In terms of days of forward demand cover, OECD commercial stocks rose by 0.5 days m-o-m in August to stand at 59.3 days. This was 3.8 days below the same period in 2017 and 2.5 days lower than the latest five-year average.

Balance of Supply and Demand

Demand for OPEC crude in 2018 is estimated at 32.7 mb/d, 0.8 mb/d lower than the 2017 level. In 2019, demand for OPEC crude is forecast at 31.8 mb/d, around 0.9 mb/d lower than the estimated level in 2018.

More information is here.

-----

Earlier:

2018, October, 10, 08:25:00

OIL PRICE: NEAR $85 ANEWREUTERS - Brent crude LCOc1 futures were down 2 cents at $84.98 a barrel by 0049 GMT, after a 1.3 percent gain on Tuesday. US. West Texas Intermediate (WTI) crude CLc1 was down by 16 cents, or 0.2 percent, at $74.8 a barrel, after rising nearly 1 percent in the previous session. |

2018, October, 8, 11:20:00

СТАБИЛЬНАЯ ЦЕНА НЕФТИМИНЭНЕРГО РОССИИ - Министр отметил, что Россия выступает за то, чтобы Иран как крупнейшая страна-экспортер энергоресурсов оставался участником рынка. "Мы не приемлем односторонних санкций, которые не соответствуют решениям ООН. Безусловно, нужно с юридической точки зрения оценивать дальнейшие возможности и механизмы взаимодействия с Ираном, чтобы наши компании не понесли ущерба», - отметил Министр. |

2018, October, 5, 12:45:00

РОССИЯ: РАВНОВЕСИЕ НА РЫНКЕМИНЭНЕРГО РОССИИ - Говоря о динамике цен на энергоресурсы, Александр Новак подчеркнул, что главной задачей как для России, так и для других участников договоренностей о регулировании добычи нефти всегда было балансирование рынка, а не рост стоимости до определенных уровней. |

2018, October, 5, 12:40:00

РОССИЯ: +300 000 БАРРЕЛЕЙМИНЭНЕРГО РОССИИ - цифры были названы президентом РФ: мы в краткосрочном периоде можем увеличить еще на 200-300 тысяч баррелей, если при этом будет необходимость и целесообразность, потому что основная задача — баланс спроса и предложения, чтобы не нарушить равновесие на рынке, а наоборот его сохранить. |

2018, October, 4, 15:05:00

ВЗАИМОДЕЙСТВИЕ РОССИИ И ОПЕКМИНЭНЕРГО РОССИИ - Президент России отметил, что за последние годы у России и ОПЕК сложились плодотворные контакты и эффективное взаимодействие. "Мне кажется, что эта совместная работа пошла на пользу всем участникам рынка. Это касается и производителей, и потребителей энергоресурсов. Благодаря нашим совместным усилиям впервые все участники этих договоренностей практически стопроцентно выполняют все свои обязательства», - отметил Владимир Путин. |

2018, October, 4, 15:00:00

СОТРУДНИЧЕСТВО САУДОВСКОЙ АРАВИИ И РОССИИМИНЭНЕРГО РОССИИ - «Видим постоянно растущую заинтересованность российских компаний в налаживании более тесных связей с саудовскими партнерами. Это особенно важно в свете той ответственной роли, которую наши страны играют на региональной и международной арене, особенно в сфере энергетики», - сказал Александр Новак.

|

2018, October, 4, 14:45:00

ЦЕНА НЕФТИ: $65 - $75МИНЭНЕРГО РОССИИ - «Сейчас рынок пытается достичь баланса цен, который будет отвечать как интересам производителей, так и потребителей. И этот уровень, вероятно, чуть ниже, чем тот, что мы видим сейчас. На основной панели Российской энергетической недели президент Владимир Путин говорил о диапазоне $65-75 за баррель, который, с одной стороны, приемлем для производителей и потребителей, с другой - время позволяет возвращать деньги в отрасль для ее стабильного дальнейшего развития», - пояснил Александр Новак. |