2018-10-01 10:55:00

PHILIPPINES GDP UP BY 6.5%

IMF - Real GDP grew by 6.7 percent in 2017 and by 6.3 percent in the first half of 2018 (y/y) led by strong public investment. Inflation rose to 6.4 percent (y/y) in August 2018, averaging 4.8 percent year to date and above the inflation target band of 2−4 percent, led by adjustments in excise taxes, the rise in global oil prices, the weaker peso, and above-trend growth. Investment-led growth and sustained supply pressures have likely raised employment with renewed wage demand pressures. Following surpluses before 2016, the current account deficit widened to 0.8 percent of GDP in 2017, driven mainly by imports of capital goods, oil, and raw materials, reflecting strong investment growth.

The economy continues to perform well but is facing new challenges. Real GDP growth is projected to grow strongly in 2018 and 2019, supported by domestic demand. However, poverty and inequality challenges remain, inflation has risen, and external uncertainty has increased. The medium-term economic outlook remains favorable, but short-term risks have risen. Real GDP growth is projected at just under 7 percent over the medium term. Inflation is projected at above the 4 percent upper target bound in 2018 and stay in the upper half of the target band (3−4 percent) during 2019–2020. The current account deficit is projected to remain manageable, financed largely by foreign direct investment. Downside risks stem mainly from rising inflation, continued rapid credit growth, higher U.S. interest rates and U.S. dollar, volatile capital flows, and trade tensions.

Executive Board Assessment

Executive Directors commended the authorities for the strong economic performance owing to sound macroeconomic management and continued reforms to promote inclusive growth. Directors noted that short-term risks have increased from rising inflation and a less favorable external environment, and underscored the need to adjust the policy mix to address these risks.

Nonetheless, the medium-term economic outlook remains favorable, placing the Philippines in a good position to tackle still-elevated poverty and inequality.

Directors broadly urged the authorities to consider adjusting the fiscal stance over 2018-2019 to continue to support pro-growth infrastructure investment and social spending while containing nonpriority spending, in order to avoid overburdening monetary policy. They stressed the importance of careful selection and management of infrastructure projects to maximize their impact on growth.

Directors supported the authorities' reforms to make tax incentives more effective in achieving national policy goals and improve economy-wide productivity. Enhancing the VAT refund system and strengthening the international taxation framework will also be steps in the right direction. Directors suggested complementing these reforms with enhanced social protection.

Directors welcomed recent decisions of the Bangko Sentral ng Pilipinas (BSP) to increase the policy rate and its announced readiness to take further actions to safeguard price stability. In this context, they recommended carefully monitoring both supply-and demand-side pressures. They also welcomed the BSP's decision to delay the bank reserve requirement cuts until inflation expectations are more firmly anchored. Directors supported the authorities' policy of allowing the exchange rate to move freely in line with market forces, while limiting foreign exchange intervention to address disorderly market conditions. They welcomed the recent launch of national retail payment systems and the progress made with domestic capital market and FX liberalization reforms.

Directors noted that the financial system appears sound. They welcomed the BSP's recent macroprudential measures to safeguard financial stability against systemic risks and noted the need for continued vigilance. While the pace of credit growth has slowed recently, the credit-to-GDP gap has widened. In this regard, Directors supported the BSP's plan to introduce a countercyclical buffer for banks and underscored the need to close data gaps on nonbank financial institutions and conglomerates. Directors encouraged the approval of the amendments to the BSP charter.

Directors welcomed the progress made by the authorities on structural reforms and encouraged them to deepen the reform efforts in seeking broader economic benefits. They supported the authorities' plan to replace the rice import quota system with one based on tariffs, while emphasizing the need to support small farmers affected by the reform. Directors noted the need to promote competition by opening new sectors of the economy to foreign investment, improve the business environment through better infrastructure, create more and better jobs through investment in human capital and labor market reforms, and modernize the bank secrecy legal framework.

|

Philippines: Selected Economic Indicators |

|||||||

|

|

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

|

|

|

|

|

|

|

Proj. |

Proj. |

|

(Annual percentage change, unless otherwise indicated) |

|||||||

|

National account |

|||||||

|

Real GDP |

7.1 |

6.1 |

6.1 |

6.9 |

6.7 |

6.5 |

6.7 |

|

Consumption |

5.5 |

5.3 |

6.5 |

7.4 |

6.0 |

6.5 |

6.5 |

|

Private |

5.6 |

5.6 |

6.3 |

7.1 |

5.9 |

5.8 |

5.9 |

|

Public |

5.0 |

3.3 |

7.6 |

9.0 |

7.0 |

11.3 |

10.7 |

|

Gross fixed capital formation |

11.8 |

7.2 |

16.9 |

26.1 |

9.5 |

18.6 |

11.7 |

|

Domestic demand |

6.8 |

5.7 |

8.7 |

11.7 |

6.9 |

9.7 |

8.0 |

|

Net exports (contribution to growth) |

-2.6 |

1.0 |

-3.1 |

-4.9 |

-0.8 |

-4.0 |

-2.2 |

|

Real GDP per capita |

5.2 |

4.3 |

4.3 |

5.2 |

5.2 |

4.4 |

4.6 |

|

Output gap (percent, +=above potential) |

0.5 |

0.3 |

-0.1 |

0.1 |

0.0 |

0.2 |

0.1 |

|

Labor market |

|||||||

|

Unemployment rate (percent of labor force) 1/ |

7.1 |

6.8 |

6.3 |

5.4 |

5.7 |

5.5 |

5.4 |

|

Underemployment rate (percent of employed persons) |

19.3 |

18.4 |

18.5 |

18.3 |

16.1 |

… |

… |

|

Employment (percent change) |

0.9 |

0.4 |

2.8 |

4.7 |

-1.6 |

2.5 |

2.4 |

|

Non-agriculture daily wages (Q4/Q4) 2/ |

2.2 |

0.0 |

3.2 |

2.1 |

4.3 |

4.3 |

… |

|

Price |

|||||||

|

Consumer prices (period average, 2012 basket) |

2.6 |

3.6 |

0.7 |

1.3 |

2.9 |

4.9 |

3.9 |

|

Consumer prices (end of period, 2012 basket) |

3.8 |

1.9 |

0.7 |

2.2 |

2.9 |

5.2 |

3.6 |

|

Residential real estate (Q4/Q4) |

… |

… |

… |

3.3 |

5.7 |

… |

… |

|

Money and credit |

|||||||

|

3-month PHIREF rate (percent, end of period) 3/ |

-0.4 |

1.8 |

2.7 |

2.0 |

3.3 |

4.0 |

… |

|

Credit to the private sector (percent of GDP) |

35.9 |

39.2 |

41.8 |

44.7 |

47.8 |

51.5 |

53.8 |

|

Credit to the private sector (percent change) |

17.2 |

19.6 |

12.4 |

16.4 |

16.6 |

20.0 |

15.8 |

|

Public finances (in percent of GDP) |

|||||||

|

National government overall balance 4/ |

-1.5 |

-0.6 |

-1.4 |

-2.4 |

-2.2 |

-2.8 |

-3.2 |

|

Revenue and grants |

14.8 |

15.1 |

15.4 |

15.2 |

15.6 |

16.0 |

16.2 |

|

Total expenditure and net lending |

16.3 |

15.7 |

16.8 |

17.6 |

17.9 |

18.8 |

19.4 |

|

General government gross debt |

45.7 |

42.1 |

41.5 |

39.0 |

39.9 |

39.5 |

38.9 |

|

Balance of payments (in percent of GDP) |

|||||||

|

Current account balance |

4.2 |

3.8 |

2.5 |

-0.4 |

-0.8 |

-1.5 |

-1.5 |

|

FDI, net |

0.0 |

0.4 |

0.0 |

-1.9 |

-2.6 |

-2.5 |

-2.3 |

|

Gross reserves (US$ billions) |

83.2 |

79.5 |

80.7 |

80.7 |

81.6 |

76.3 |

73.9 |

|

Gross reserves (percent of short-term debt) |

406.2 |

413.3 |

409.5 |

423.9 |

422.9 |

384.7 |

372.0 |

|

Total external debt |

28.9 |

27.3 |

26.5 |

24.5 |

23.3 |

21.3 |

19.5 |

|

Memorandum items: |

|||||||

|

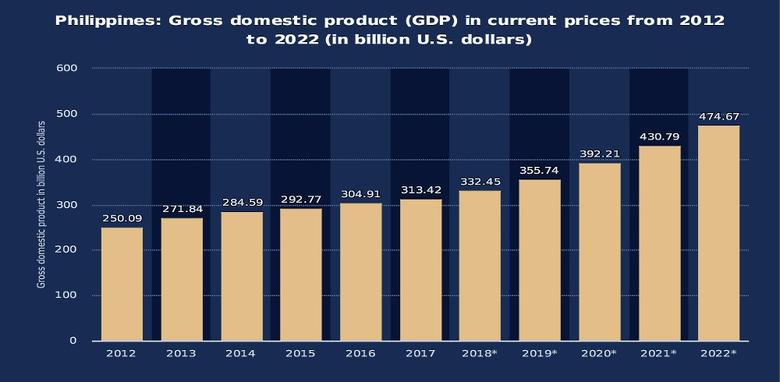

Nominal GDP (US$ billions) |

271.8 |

284.6 |

292.8 |

304.9 |

313.6 |

334.7 |

360.7 |

|

Nominal GDP per capita (US$) |

2,768 |

2,849 |

2,883 |

2,953 |

2,989 |

3,129 |

3,305 |

|

GDP (in billions of pesos) |

11,538 |

12,634 |

13,322 |

14,480 |

15,806 |

17,574 |

19,480 |

|

Real effective exchange rate (2005=100) |

109.9 |

109.5 |

116.8 |

113.2 |

108.6 |

… |

… |

|

Peso per U.S. dollar (period average) 5/ |

42.4 |

44.4 |

45.5 |

47.5 |

50.4 |

53.4 |

… |

|

Sources: Philippine authorities; World Bank; and IMF staff estimates and projections. |

|||||||

|

1/ Estimates exclude data of the entire Region VIII. |

|||||||

|

2/ In National Capital Region. Latest observation as of June 2018. |

|||||||

|

3/ Benchmark rate for the peso floating leg of a 3-month interest rate swap. Latest observation as of July 2018. |

|||||||

|

4/ IMF definition. Excludes privatization receipts and includes deficit from restructuring of the previous Central Bank-Board of Liquidators. |

|||||||

|

5/ Latest observation as of July 2018. |

|||||||

-----

Earlier:

2018, April, 16, 09:20:00

PHILIPPINES: KEY INVESTMENTSWBG - Investments in infrastructure and education, skills, and health, are not only key to sustaining high growth but will also ensure that poor and vulnerable families have access to better job opportunities. Delivering inclusive economic growth through good jobs remains the country’s most pressing challenge, according to the World Bank. |

2018, March, 28, 11:00:00

CHINA - PHILIPPINES COOPERATIONOGJ - The governments of China and the Philippines say they’re moving toward cooperative offshore oil and gas exploration.

|

2018, March, 5, 11:25:00

SOUTH CHINA SEA OILREUTERS - Any deal between the Philippines and a Chinese firm to jointly explore for gas in the Reed Bank of the South China Sea will be illegal unless China recognizes the southeast Asian nation’s sovereign rights there, a Philippine judge said on Monday. |

2017, April, 6, 18:45:00

SOUTH CHINA SEA SOVEREIGNTYChina claims almost all of a large stretch of sea between Taiwan, Malaysia, Indonesia, the Philippines, Brunei, Vietnam and Japan. The trouble is, between them, these seven other states all do too.

|

2016, July, 26, 19:00:00

PHILIPPINES NEED OFFSHOREThe Philippines relies overwhelmingly on imports to fuel its fast-growing economy. That reliance will grow further in a few years when the main source of domestic natural gas runs out, so the clock is ticking for it to develop offshore fields that China shows no sign of loosening its grip on. |

2016, July, 5, 18:15:00

SOUTHEAST ENERGY WARAbout $5 trillion in ship-borne trade passes every year though the energy-rich, strategic waters of the South China Sea, where China's territorial claims overlap in parts with Vietnam, the Philippines, Malaysia, Brunei and Taiwan. |

2015, June, 15, 18:40:00

CHINA & PHILIPPINES TALKSChina’s ambassador to the Philippines has suggested that the two countries sit down for talks on the most squeamish territorial dispute in Asia. The question of who controls the fishery-rich, 3.5 million-square-kilometer South China Sea, also full of oil and natural gas as well as major world shipping lanes, could proceed from military preparations to a calm negotiating room. The two governments – both unusually aggressive in asserting rival claims to the sea — might be able to work something out. The Philippines is talking now to Taiwan to agree on law enforcement in their own overlapping waters. |