2018-11-15 15:47:00

OPEC: OIL DEMAND 2019: 100 MBD

OPEC - Monthly Oil Market Report, November 2018

Oil Market Highlights

Crude Oil Price Movements

The OPEC Reference Basket (ORB) ended October higher, increasing by $2.21, or 2.9% month-on-month (m-o-m), to average $79.39/b, the highest monthly average since October 2014. Crude oil futures also peaked in early October, hitting a four-year high, with ICE Brent reaching $86.29/b, as the market focused on concerns over potential oil supply shortages. ICE Brent increased by $1.52 m-o-m, or 2%, reaching $80.63/b in October, while NYMEX WTI rose by 67¢, m-o-m, or 1.0%, averaging $70.76/b. Year-to-date, ICE Brent was $20.54, or 39%, higher at $73.58/b, while NYMEX WTI increased $17.63, or 36%, to $67.23/b, compared with the same period a year earlier. The Brent-WTI spread widened by 85¢ reaching $9.87/b. Brent and Dubai backwardation structures eased over the month, coming under pressure from higher crude oil production and an oil price correction that concentrated in the prompt months. In the US, the WTI price structure flipped into contango for the first time since last May, reflecting weak supply and demand fundamentals in Cushing, Oklahoma. Hedge funds and other money managers slashed their combined speculative net length positions to end the month at their lowest levels in more than a year.

World Economy

The global economic growth forecast for 2018 remains unchanged at 3.7%, while the 2019 forecast was revised down slightly by 0.1 percentage point (pp) to now stand at 3.5%, on the back of a slowing dynamic amid rising trade tensions, monetary tightening, particularly in the US, and mounting challenges in emerging markets and developing economies. In the OECD, growth in the US is assessed to be unchanged at 2.9% in 2018, but was revised slightly upward to 2.6% in 2019. Euro-zone growth was revised down to 1.9% for 2018 and to 1.7% for 2019. GDP growth in Japan remains at 1.1% in both 2018 and 2019 each. In the non-OECD countries, both India’s and China’s growth forecasts were revised slightly downward to 7.5% and 6.5% for 2018, respectively, and lowered to 7.2% and 6.1%, respectively, for 2019. Growth in Brazil remains unchanged at 1.1% in 2018 and at 1.8% in 2019. Russia’s GDP growth forecast is also unchanged at 1.6% in 2018 and 1.7% in 2019.

World Oil Demand

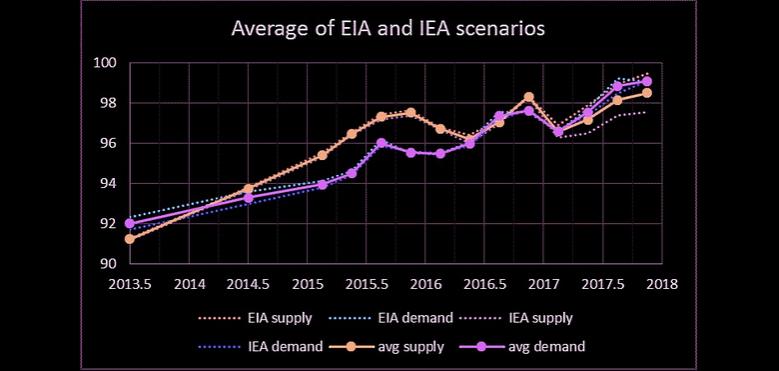

In 2018, oil demand growth is anticipated to increase by 1.50 mb/d y-o-y, a downward revision from the previous month of 40 tb/d, mainly due to weaker-than-expected oil demand data from the Middle East and, to a lesser extent, China during 3Q18. Expected total oil demand for the year is anticipated to reach 98.79 mb/d. In 2019, world oil demand growth is forecast to grow by 1.29 mb/d y-o-y, about 70 tb/d lower than last month’s projection, with total world consumption to reach 100.08 mb/d. The OECD region will contribute positively to oil demand growth, increasing by 0.25 mb/d y-o-y, while the non-OECD region is assumed to see larger growth by 1.04 mb/d in 2019.

World Oil Supply

Non-OPEC oil supply growth in 2018 is estimated at 2.31 mb/d, an upward revision of 0.09 mb/d from the previous month’s assessment. The US, Canada, Kazakhstan and Russia are expected to be the main drivers for this growth, while Mexico, Norway, Vietnam and China are expected to show the largest declines. With this, total non-OPEC supply for 2018 is now estimated at 59.86 mb/d. In 2019, non-OPEC oil supply growth was revised up by 0.12 mb/d from the previous month, forecast to stand at 2.23 mb/d and is now projected to reach an average of 62.09 mb/d. The upward revision comes despite a downward adjustment for oil supply in Canada, China, Brazil and Mexico. The US, Brazil, Canada and the UK are expected to be the main growth drivers, while Mexico, Norway, Vietnam and Indonesia are still expected to see the sizeable declines. OPEC NGLs in 2018 and 2019 are expected to grow by 0.10 mb/d and 0.11 mb/d to average 6.34 mb/d and 6.45 mb/d, respectively. In October, OPEC crude oil production increased by 127 tb/d to average 32.90 mb/d, according to secondary sources.

Product Markets and Refining Operations

Product Markets in the Atlantic Basin during October showed a mixed performance. In the US, product markets strengthened on the back of positive performance at the middle and the bottom of the barrels, as lower product output, due to peak maintenance season and considerable gasoil and jet/kerosene inventory drawdowns, provided a boost to refining margins. In Europe, product markets lost ground as gasoline cracks plummeted to new lows, exhibiting the highest y-o-y decline since December 2017. This, coupled with naphtha weakness weighed on cracks, despite support from the middle and bottom of the barrels. In Asia, product markets lost some ground as severe weakening at the top of the barrel, owing to regional gasoline oversupply, outweighed support from the bottom of the barrel, attributed to lower gasoil and fuel oil output.

Tanker Market

Sentiment in the dirty tanker market strengthened considerably in October, as freight rates for all classes showed improvements on all major trading routes. Average dirty tanker spot freight rates rose by 28%, compared to a month earlier. Gains in the dirty tanker sector were driven by higher seasonal tonnage demand, weather delays in different regions, and ship replacements, among other factors. Nevertheless, tanker market gains in October were affected by higher bunker prices, thus raising operational cost. On the other hand, clean tanker freight rates also experienced gains in both directions of Suez, albeit to a lesser degree.

Stock Movements

Preliminary data for September showed that total OECD commercial oil stocks rose by 5.5 mb m-o-m to stand at 2,858 mb. This was 111 mb lower than the same time one year ago, and 25.3 mb below the latest five-year average. Crude stocks indicated a deficit of 29.6 mb, while products stocks witnessed a surplus of 4.3 mb. However, OECD commercial stocks remain 287 mb above the January 2014 level. In terms of days of forward demand cover, OECD commercial stocks fell by 0.4 days m-o-m in September to stand at 59.3 days. This was 2.7 days below the same period in 2017 and 2.1 days lower than the latest five-year average.

Balance of Supply and Demand

Demand for OPEC crude in 2018 is estimated at 32.6 mb/d, 0.9 mb/d lower than the 2017 level. In 2019, demand for OPEC crude is forecast at 31.5 mb/d, around 1.1 mb/d lower than the estimate 2018 level.

-----

Earlier:

2018, November, 14, 12:20:00

ИНТЕРВЬЮ АЛЕКСАНДРА НОВАКА ТЕЛЕКАНАЛУ "РОССИЯ 24" ОБ ИТОГАХ ЗАСЕДАНИЯ МОНИТОРИНГОВОГО КОМИТЕТА СТРАН ОПЕК+Глава Минэнерго России подчеркнул, что все участники соглашения ОПЕК+ выполняют взятые на себя обязательства, при этом мониторинг ситуации на нефтяном рынке будет продолжен. |

2018, November, 14, 12:15:00

OIL MARKET UNCERTAINTYCNBC - Saudi Arabia, OPEC's biggest producer and the world's top crude exporter, intends to cut shipments by 500,000 barrels a day in December, Khalid al Falih, the country's energy minister said on Sunday. Russian Energy Minister Alexander Novak said on Sunday he wasn't convinced the oil market would be oversupplied in 2019. Russia is the world's second biggest oil producer after the United States and, along with Saudi Arabia, plays an influential role in the oil alliance.

|

2018, November, 12, 12:25:00

CONFORMITY LEVEL 104%OPEC - In advance of the scheduled meetings in December 2018, the JMMC directed the JTC to continue closely monitoring oil market conditions and further refine the scenario analysis based on updated data, with regard to options on new 2019 production adjustments, which may require new strategies to balance the market. |

2018, November, 12, 12:20:00

РОССИЙСКО-САУДОВСКИЕ ПЕРСПЕКТИВЫМИНЭНЕРГО РОССИИ - «Российско-саудовские отношения обладают солидными перспективами в сфере энергетики. Нами рассматриваются ряд масштабных совместных проектов, которые выведут российско-саудовское сотрудничество на принципиально новый уровень», - отметил российской министр.

|

2018, November, 12, 12:10:00

OIL PRICES WILL UPCNBC - "In the 2020's we are going to have a clear physical shortage of oil because nobody is allowed to fully invest in future oil production," Michele Della Vigna, Head of EMEA Natural Resources Research at Goldman Sachs told CNBC Friday.

|

2018, November, 9, 15:35:00

SAUDIS OIL RECORD: 10.67 MBDPLATTS - Saudi Arabia pumped 10.67 million b/d in the month, its most in the 30-year history of the Platts OPEC survey, while key ally the UAE also set an all-time high at 3.17 million b/d. Libya produced its most since June 2013 at 1.10 million b/d.

|

2018, November, 9, 15:20:00

GLOBAL OIL INVENTORIES WILL UPU.S. EIA - Global inventories are projected to increase and put downward pressure on crude oil prices. |