2018-02-14 10:05:00

IEA: OIL DEMAND GROWTH 1.6 MBD

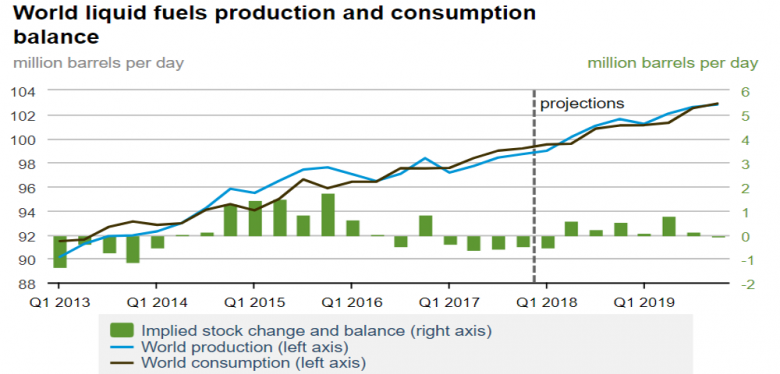

IEA - This month's OMR is abbreviated to allow time for us to complete our annual five-year outlook that will be published in our report Oil 2018 on 5 March. Meanwhile, new and revised data shows a modest tightening of the balance in the early part of 2018, but the main message remains unchanged from last month and it is very clear: in 2018, fast rising production in non-OPEC countries, led by the US, is likely to grow by more than demand. For now, the upward momentum that drove the price of Brent crude oil to $70/bbl has stalled; partly due to investors taking profits, but also as part of the corrections we have seen recently in many markets. Most importantly, the underlying oil market fundamentals in the early part of 2018 look less supportive for prices.

Our demand growth estimate for 2017 remains strong at 1.6 mb/d, reinforced by November data for the US. For 2018, the more positive global economic picture published by the International Monetary Fund is a key factor in raising our growth outlook to 1.4 mb/d. It was thought that the significant increase in the dollar price of crude oil since the middle of 2017 would dampen growth, and this might be the case to some extent, but the impact of higher prices has been partly offset in some countries by currency appreciations.

It is clear that strong demand growth in 2017, alongside a modest increase last year in non-OPEC output, and the cuts made by leading producers, has contributed to the extraordinarily rapid fall in OECD oil stocks. A year ago, they were 264 mb above the five-year average and now they are only 52 mb in excess of it, with stocks of oil products actually below the benchmark. Although the OECD is not the whole world, the leading oil producers who agreed to cut output identified the level of the group's stocks as an indicator of the progress of their initiative. With the surplus having shrunk so dramatically, the success of the output agreement might be close to hand. This, however, is not necessarily the case: oil price rises have come to a halt and gone into reverse, and, according to our supply/demand balance, so might the decline in oil stocks, at least in the early part of this year.

The main factor is US oil production. In just three months to November, crude output increased by a colossal 846 kb/d, and will soon overtake that of Saudi Arabia. By the end of this year, it might also overtake Russia to become the global leader. All the indicators that suggest continued fast growth in the US are in perfect alignment; rising prices leading, after a few months, to more drilling, more completions, more production, and more hedging. In early 2018, the situation is reminiscent of the first wave of US shale growth that, riding the tide of high oil prices in the early years of this decade, made big gains in terms of market share and eventually in 2014 forced a historic change of policy by leading producers. Today, having cut costs dramatically, US producers are enjoying a second wave of growth so extraordinary that in 2018 their increase in liquids production could equal global demand growth. This is a sobering thought for other producers currently sitting on shut-in production capacity and facing a renewed challenge to their market share. Another sobering thought is that it is not just a matter of production: trade patterns are changing. Recently we read of a shipment of condensate from the US to the UAE. Such a development would have seemed incredible a few years ago, now it looks like the shape of things to come.

The components of the oil market balance are dynamic and a lot can change in the next few months: the deteriorating situation in Venezuela is one obvious candidate, and the apparent buoyancy of the global economy could deliver higher demand growth than we currently anticipate. As a result, prices could be maintained at recent levels even as US production rises. If so, most producers will be happy, but if not, history might be repeating itself.

-----

Earlier:

2018, February, 5, 07:45:00

EXXON ENERGY OUTLOOK - 2040EXXONMOBIL - Despite efficiency gains, global energy demand will likely increase nearly 25 percent. Nearly all growth will be in non-OECD countries (e.g. China, India), where demand will likely increase about 40 percent, or about the same amount of energy used in the Americas today.

|

2018, February, 2, 12:20:00

HEAVY ASIAN DEMANDU.S. FRB - In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1-1/4 to 1‑1/2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

|

2017, December, 18, 12:35:00

INEVITABLE OIL CHANGESOPEC - Sustainable oil market stability is crucial to attract the level of investment necessary for future demand growth; In the longer term, oil will remain a vital and integral part of the energy mix; Global energy and oil demand will grow in the long term;

|

2017, November, 15, 15:15:00

IEA: GLOBAL ENERGY DEMAND UP BY 30%Global energy needs rise more slowly than in the past but still expand by 30% between today and 2040. This is the equivalent of adding another China and India to today’s global demand.

|

2017, November, 9, 14:00:00

OPEC: 2040 GLOBAL ENERGY CHANGESWithin the grouping of Developing countries, India and China are the two nations with the largest additional energy demand over the forecast period, both in the range of 22–23 mboe/d.

|

2017, October, 16, 12:20:00

WORLD OIL DEMAND UP BY 1.5 MBDWorld oil demand growth in 2017 is now expected to increase by 1.5 mb/d, representing an upward revision of around 30 tb/d from last previous report, mainly reflecting recent data showing an improvement in economic activities. Positive revisions were primarily a result of higher-than-expected oil demand from the OECD region and China. In 2018, world oil demand is anticipated to grow by 1.4 mb/d, following an upward adjustment of 30 tb/d over the previous report, due to the improving economic outlook in the world economy, particularly China and Russia.

|

2017, September, 29, 12:25:00

U.S. HIGHEST PETROLEUM DEMANDTotal petroleum deliveries in August moved up by 1.3 percent from August 2016 to average 20.5 million barrels per day. These were the highest August deliveries in 10 years, since 2007. Compared with July, total domestic petroleum deliveries, a measure of U.S. petroleum demand, decreased 0.6 percent. For year-to-date, total domestic petroleum deliveries moved up 1.3 percent compared to the same period last year. |