2018-06-27 10:40:00

IMF: AUSTRIA'S GROWTH 3%

IMF - Austria: Staff Concluding Statement of the 2018 Article IV Mission

Living standards in Austria are high, and income inequality and poverty low. After several years of slow growth, output has accelerated markedly in 2017/18. This provides an opportunity to implement reforms to raise the economy's potential output, reduce unemployment further, and ensure long-term fiscal sustainability. Also, further strengthening the financial system is important as the global financial environment may become less benign.

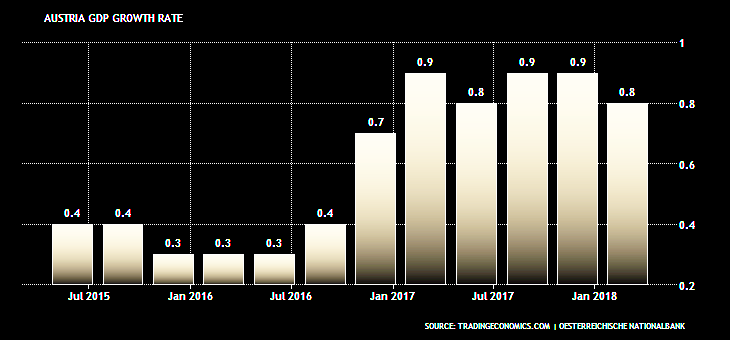

Austria's economy is robust. Supported by expansionary monetary and fiscal policies, growth has picked up markedly, to 3 percent in 2017 and 3.1 percent (y/y) in Q1 2018. A recovery in private investment and a favorable external environment as growth in Europe accelerated more broadly, have underpinned growth. Concomitantly, unemployment has declined recently. Inflation remains broadly stable, at 2 percent (y/y) in April.

The outlook has strengthened. We project growth in 2018 to remain at about 3 percent, supported by a rise in private consumption, still-strong investment and net exports. High investment is laying the foundations for continued robust expansion in the medium term, though growth is expected to gradually converge to its potential rate, which we estimate at around 1¾ percent.

The external position is strong, and broadly in line with fundamentals and desirable policies. Exports have held up well, and the current account surplus is expected to remain around 2 percent of GDP, underpinned by a rising share of trade in services, in which Austria has traditionally had a surplus as well as rising income receipts due to a strengthening international investment position.

The fiscal outturn in 2017 was better than expected. The structural deficit stood at 0.6 percent of GDP, largely because of the higher-than-anticipated economic growth, but also on account of savings on interest payments. Public debt fell by five percentage points, to 78.4 percent of GDP, due to the strong performance of the economy as well as asset recoveries of intervened banks.

The financial sector is sound. Austrian banks' capital adequacy has improved, although some momentum has been lost in 2017, compared to previous years. This in part reflects the phasing in of a systemic risk capital buffer of up to 2 percent (CET-1) in the thirteen largest banks, which will become fully effective in 2019. Vulnerabilities have been reduced, and profitability has risen, though largely due to reduced risk provisions. Banks have continued their cost cutting efforts, but progress has been slow. The supervisory framework has been strengthened.

Risks to the outlook are largely external, and would likely have a moderate impact if they were to materialize. Increasingly inward-oriented economic policies in some trading partners and reduced international policy coordination and collaboration, and structurally low growth in advanced economies would weaken Austria's economic and financial outlook. On the domestic side, if efforts to integrate immigrants were unsuccessful, this could reduce their contribution to the economy, slowing growth and increasing welfare spending.

This overall robust background offers an opportunity to address a number of longer-term challenges. Ensuring long-term fiscal sustainability, reducing unemployment durably, and consolidating financial stability are key tasks to address.

Fiscal Policy and Reforms

Rebuilding fiscal buffers and further lowering public debt are key for ensuring long-term fiscal sustainability . Therefore, Austria's medium-term objective (MTO) under the Stability and Growth Pact of a structural balance of -0.5 percent of GDP remains appropriate.

The government's medium-term fiscal consolidation plans are ambitious. The authorities are targeting a structural fiscal surplus by 2022 while at the same time reducing the taxes and social security contributions burden toward 40 percent of GDP. This requires significant expenditure cuts, and the savings so far identified are not fully sufficient to reach this target. Moreover, Austria's population is aging, which will lead to increasing spending pressures in pensions, health, and elderly care. In the mission's projection, these pressures will lead to a gradual widening of the fiscal deficit from 2022 onward.

The time is ripe for implementing efficiency-raising reforms. Structural fiscal reforms—including reforms in fiscal federal relations comprising stronger incentives for cost savings in the health system and subsidy reduction—could deliver a streamlining of spending. Overall, the savings potential from such reforms could be in the range of 2½–3 percent of GDP over the medium term. Also, further reforms to the pension system could ease future fiscal pressures.

In designing reforms, including the planned tax reform, equity considerations need to be taken into account. Austria's income inequality and poverty rates are relatively low, an achievement that should be preserved, though trade-offs between equity and incentives need to be carefully weighed. In this regard, the reduction in social security contributions for low-income earners is a step in the right direction (including to help their employment prospects). Further steps to lower the tax wedge, especially on low incomes, should follow, which could be financed by higher taxation of environmental pollution and wealth.

Reducing Unemployment Further

Structural unemployment may rise as there are indications that labor market mismatches are increasing. Therefore, driving down unemployment rates sustainably to levels before the GFC requires proactive policies to increase employability, and measures to strengthen demand for labor. Key measures are:

Improving education outcomes: Unemployment is highest among those with only compulsory schooling. Strengthening education would help prepare workers for jobs that increasingly demand higher (though not necessarily only academic) skills. In this regard, the recent increase up to the age of 18 of compulsory schooling or training, and the training guarantee for people under 25, are positive steps. Austria's strong and institutionally deep-rooted dual-education system is well-placed to boost skills.

Integrating foreigners (including accepted refugees) into the labor market: Foreign nationals—an increasing share of the labor force—frequently have lower levels of education and training than Austrians, but even at the same level of education, their unemployment rates are higher. Therefore, the specific hurdles that non-Austrians face, including acquiring recognized qualifications and language skills, need to be addressed. The authorities' efforts in this regard are welcome.

Active labor market policies (ALMPs): Targeted polices can help specific segments of the workforce. In particular, elderly and long-term unemployed workers have significant difficulty in again finding a job. However, costs and benefits of ALMP schemes will need to be weighed carefully.

Boosting labor demand: Policies to strengthen innovation and competition by lowering barriers to entrepreneurship, a shift in the tax mix away from labor, and higher public investment in ICT, would help maintain the currently high level of private investment and productivity, and with them potential output and employment. In some of these areas, planned steps are promising, such as expansion of the broadband network and better targeted financing for R&D.

Consolidating Financial Stability

Recent developments in the financial sector are encouraging, but its foundations need to be strengthened further. Large banks have reached capital levels under the sustainability package. The authorities' 2017 update of their regulatory guidance to focus on strengthening the business models of the major internationally active banks is appropriate. This would also help support further strengthening of capital positions to underpin longer-term resilience. The adoption of legislation to lay the basis for using targeted real-estate macroprudential tools is welcome.

Credit extension in Austria has recovered from post-crisis lows. Both credit to nonfinancial corporations and to households have accelerated and are now growing broadly in line with nominal GDP, and indebtedness remains below peers' levels.

Risks to the financial sector emanating from the real estate market are contained. While house prices nationally, especially in Vienna, appear overvalued, household indebtedness is low and stable, and the exposure of the financial system to the real estate market remains limited. Also, a large share of the population lives in rented accommodations, and is thereby shielded from adverse price developments. Therefore, new real-estate specific macroprudential measures do not appear to be needed at this point. The mission considers the authorities' approach of first collecting and analyzing more comprehensive data under new reporting requirements appropriate. However, with some indicative signs of eased lending standards, they need to remain vigilant and be prepared for pre-emptive action to head off stability risks if needed.

The current benign economic environment offers an opportunity to strengthen the financial system further. While the recent rise in profits is welcome, a significant part of these gains stems from one-off factors (reduced risk provisioning). Large banks need to continue implementing their adjustment plans and raising capital. This would prepare them for a possible deterioration in the macro-financial environment. As net interest income remains constrained in the low interest rate environment, this requires efforts to reduce structural costs (which may also involve investments in efficiency-enhancing infrastructure), to continue refocusing on core activities, and withdrawing from non-profitable and high-risk activities and locations. Supervisory and regulatory authorities need to remain firm to ensure banks maintain and further improve sound capitalization levels, reduce risks further, and implement their cost-cutting plans. Smaller deposit taking banks also need to cut costs, including through realizing synergies. However, the case for bail-in-able debt (MREL) in excess of minimum capital requirements is weak for them.

A stronger AML/CFT framework will help Austria maintain its position as a financial center. [1] The authorities need to continue to implement measures to strengthen their AML/CFT framework in line with their action plan adopted in response to the 2016 Financial Action Task Force (FATF) Mutual Evaluation Report. Several action plan items have already been addressed by legislative measures over the course of the last two years. Austria should further enhance the effectiveness of its AML/CFT framework, in particular by improving the investigation and prosecution of money laundering and the use of financial intelligence, and implement the recently-issued 5th EU AML Directive.

-----

Earlier:

2018, May, 18, 08:45:00

GAZPROM - AUSTRIA: +70.4%GAZPROM - The parties reviewed the issues of cooperation in the energy industry, focusing on, inter alia, substantial growth in Russian gas exports to Austria. According to preliminary data, from January 1 through May 14, 2018, Gazprom delivered to Austria 4.7 billion cubic meters of gas, an increase of 70.4 per cent from the same period of last year. |

2018, April, 27, 11:05:00

GAZPROM - AUSTRIA COOPERATIONGAZPROM - According to estimates, Russian gas exports to Austria between January 1 and April 24 exceeded the amount exported in the same period of last year by 79.2 per cent, with 4.2 billion cubic meters of gas delivered to consumers. |

2018, April, 11, 13:00:00

RUSSIAN GAS FOR AUSTRIA: +77%GAZPROM - from January 1 through April 8, 2018, Gazprom had supplied Austria with 3.7 billion cubic meters of gas, a rise of 77.2 per cent compared to the same period of last year. |

2018, February, 27, 14:10:00

RUSSIAN GAS FOR AUSTRIA UPGAZPROM - In early 2018, the demand for gas is still on the rise in the country. According to estimates, from January 1 through February 21, 2018, Gazprom delivered to Austria 1.8 billion cubic meters of gas, a rise of 60.6 per cent against the same period of 2017 (1.1 billion cubic meters). |

2017, October, 18, 19:00:00

GAZPROM FOR AUSTRIA: +48%From January 1 through October 15, 2017, Gazprom had supplied Austria with 6.4 billion cubic meters of gas, up 48.3 per cent or 2.1 billion cubic meters of gas versus the same period in 2016. Moreover, on October 4, 2017, the amount of gas delivered by Gazprom to Austria since the start of 2017 exceeded the full-year total for 2016 (6.13 and 6.1 billion cubic meters, respectively). |

2017, June, 5, 14:55:00

RUSSIAN GAS TO AUSTRIA: UP 79.5%Following last year’s increase of 38 per cent, Gazprom continued to boost its gas exports to the Austrian market. Specifically, from January through May 2017 Russian gas deliveries to Austria added 79.5 per cent compared to the same period of 2016. |

2016, December, 15, 18:45:00

GAZPROM - OMV AGREEMENTAlexey Miller, Chairman of the Gazprom Management Committee, and Rainer Seele, Chairman of the OMV Executive Board, signed the Basic Agreement regarding the asset swap. The signing ceremony took place in the presence of Hans Jörg Schelling, Minister of Finance of the Republic of Austria, and Anatoly Yanovsky, Deputy Minister of Energy of Russia. |