2018-06-18 13:45:00

SOUTH AFRICA: NO BENEFITS

IMF - South Africa: Staff Concluding Statement of the 2018 Article IV Mission

A challenging outlook

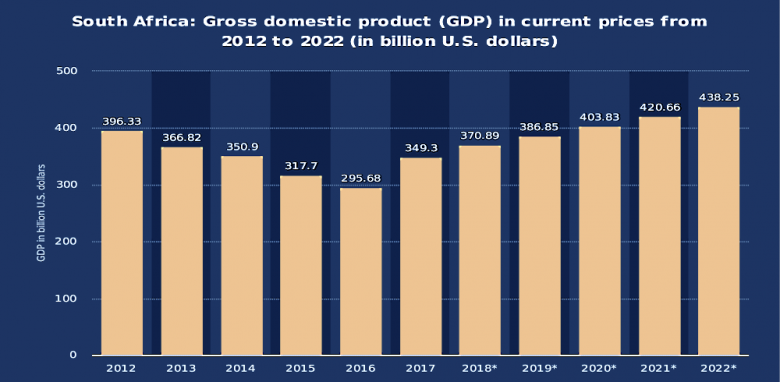

South Africa's potential is significant, yet growth over the past five years has not benefitted from the global recovery. The economy is globally positioned, sophisticated, and diversified, and several sectors—agribusiness, mining, manufacturing, and services—have capacity for expansion. Combined with strong institutions and a young workforce, opportunities are vast. However, several constraints have held growth back. Policy uncertainty and a regulatory environment not conducive to private investment have resulted in GDP growth rates that have not kept up with those of population growth, reducing income per capita, and hurting disproportionately the poor.

This year, growth is projected to be somewhat higher —at 1.5 percent—but still insufficient to make a meaningful dent in unemployment, poverty, and inequality. South Africa is one of the most unequal economies in the world. More than half of the population lives in poverty and 27 percent of the labor force is unemployed. Absent reform implementation, growth is unlikely to exceed 2 percent over the medium term.

Authorities' recent reform efforts

The authorities' stated priorities of strengthening governance and promoting employment present an opportunity to accelerate the growth momentum. Measures adopted to tackle corruption, such as changes in boards and/or management of major state-owned enterprises (SOEs), an inquiry into tax administration, actions to strengthen procurement, the signing of contracts with independent power producers, and in general, the intention to eliminate wasteful expenditure are welcome. However, to durably improve growth and lift people out of poverty, these actions need to be followed by strict enforcement of good regulations, such as the Public Financial Management Act, and the implementation of a broad set of reforms.

Structural reforms to create jobs and improve welfare for all South Africans

Materially turning the economy around toward strong and inclusive growth will require swift implementation of a bold reform agenda. Reforms in product and labor markets must span all sectors of the economy, and implementation carried out expeditiously.

- Reforms with a potential for quick payoffs should be implemented right away. These include maximizing the benefits of social grants for the poor by reducing intermediation costs; clarifying mining regulation to foster private investment in the sector; and allocating broadband spectrum to the private sector to increase competition, improve the quality of service, and reduce user charges. Other possible quick wins include mitigating skill shortages by addressing onerous visa requirements for hiring skilled workers.

- While more wide-reaching reforms may take longer to implement, these should also be promptly initiated. Increasing private-sector participation would support cost-effective energy distribution and transportation. Improving efficiency of SOEs would lower the costs to businesses and consumers, and reduce fiscal risks. Reducing red tape would lower entry barriers for businesses and strengthen competition. Enhancing flexibility in the labor market, improving basic education, and aligning training with business needs would help increase employment over time, particularly that of the youth.

- The introduction of the national minimum wage has the potential to benefit workers, but its impact should be carefully monitored, and complementary measures envisaged if undue effects on youth employment and small- and medium-sized enterprises ensue.

- Clearly articulating policy and regulatory decisions related to land reform in a fair, transparent, and market-friendly manner would help remove uncertainty, which is currently weighing on investor sentiment.

Role of fiscal, monetary, and financial sector policies to complement reforms

Fiscal policy to rebuild policy buffers

Public debt has risen, depleting buffers, and leaving little room for fiscal policy to support growth. On the back of high expenditure levels, public debt as a share of GDP has doubled during the last decade, reaching 53 percent of GDP in 2017, and pushing up public-sector gross financing needs. In the past fiscal year, the fiscal deficit was more than 1 percentage point of GDP above the budget target, as revenues underperformed, affected by low growth, and expenditures were pushed up by bailout costs from loss-making SOEs.

Fiscal consolidation is needed to strengthen public finances. The moderate fiscal consolidation envisaged in the 2018 budget is a step in the right direction. However, using IMF staff's more conservative growth projections, debt would continue to rise in the medium term. To ensure that debt remains contained at comfortable levels and policy buffers are replenished, staff recommends taking additional measures—yielding ¾–1 percent of GDP—over the next three years. This proposal reasonably balances the trade-off between adjustment and growth. Subjecting macroeconomic assumptions to independent scrutiny to set realistic expenditure ceilings, or alternatively adding a debt ceiling to the fiscal framework could also help achieve the debt objective.

Measures to contain spending and enhance tax collection are needed. A large public-sector wage bill relative to the size of the economy and to that in many peer emerging markets (EMs), is at the center of the fiscal expansion. Therefore, rationalizing the public-sector wage bill becomes a priority. Other adjustment measures, which will also enhance the ability of fiscal policy to address inequality, include boosting the efficiency of spending, such as education subsidies and transfers to public entities, and eliminating irregular and wasteful expenditure. Forcefully strengthening tax administration will complement these efforts.

Monetary policy to anchor inflation expectations at a lower level

Should fiscal consolidation stabilize debt, the monetary policy stance appears appropriate. However, monetary policy should be cautious given fiscal risks and the need to build buffers. While inflation expectations are well anchored, they remain close to the upper end of the inflation targeting band. Staff welcomes the authorities' increased focus on lowering inflation expectations toward the mid-point of the band, which could be complemented by explicitly adopting a mid-point within a range at an opportune time. Lower inflation will be better aligned with that of partners, avoid erosion of competitiveness, and benefit the poor. Staff welcomes enhancements in central bank communication, and encourages continued efforts to increase transparency. The floating rand cushions the economy against shocks, but opportunistically building international reserves would strengthen resilience.

Financial sector policy to maintain a sound financial system

Preserving financial sector stability is a priority. The authorities' introduction of the Twin Peaks regime provides a welcome overhaul of the regulatory framework. While the overall banking sector is well capitalized and profitable, monitoring pockets of vulnerabilities in small, non-systemic banks is essential. Devoting increased resources to regularly conduct top-down stress tests will be helpful. The planned entry of new banks can boost competition, reduce user charges, and improve access to credit for SMEs. Combined with the increased focus on the role of Fintech, greater competition can also help promote financial inclusion.

Balance of risks

Downside risks to the outlook are prominent. On the upside, quick and comprehensive reform implementation would boost business and consumer confidence and in turn productivity, investment, and growth. On the downside, however, spending pressures —arising for example from weak SOEs or increasing public sector compensation—would heighten financing costs and weigh on growth. Externally, tighter global financial conditions and capital flow volatility recently experienced by EMs bring to the fore a risk of sudden reversals in investor sentiment. Structurally weak growth in key advanced markets, or a disruption in trade due to growing protectionism could widen the fiscal and current account deficits, and dampen growth. Weakening growth in South Africa could have negative and lasting spillover effects on neighboring countries.

Action is needed now

The time is now to put the South African economy on a trajectory toward strong and inclusive growth. Removing policy and regulatory uncertainty, combined with forceful implementation of an ambitious reform agenda would further strengthen confidence, attract private investment durably, support job creation, and distinguish South Africa further from other EMs at a time sentiment towards EMs is weakening. Growth would then rise above the current level, and support better living standards for all South Africans.

-----

Earlier:

2018, February, 7, 07:20:00

SOUTH AFRICA'S EXPLORATIONTOTAL - Total has signed an agreement to sell a 25% interest in the Exploration Block 11B/12B, offshore South Africa, to Qatar Petroleum. The transaction remains subject to regulatory approval. |

2018, February, 2, 12:05:00

SOUTH AFRICA'S GAS UPEIA - South Africa is one of the world’s leading emitters of energy-related carbon dioxide (CO2), ranking fifteenth globally in 2015 and accounting for more than any other country in Africa. In an effort to reduce CO2 emissions, South Africa is planning to diversify its energy portfolio, replacing coal with lower CO2-emitting fuels such as natural gas and renewable sources. The country’s Intended National Determined Contribution, submitted as part of the Paris Agreement, plans for CO2 emissions to peak by 2025, remain flat for a decade, and begin to decline around 2035. |

2016, July, 8, 18:25:00

WBG: GLOBAL GROWTH DOWN TO 2.4%The World Bank is downgrading its 2016 global growth forecast to 2.4 percent from the 2.9 percent pace projected in January. The move is due to sluggish growth in advanced economies, stubbornly low commodity prices, weak global trade, and diminishing capital flows. |

2016, June, 7, 18:35:00

SOUTH AFRICA UPGRADE: $2.7 BLN“South Africa’s oil refineries are not ready and will not be ready to produce Euro 4 standard fuel, let alone Euro 6, which the world is moving to by 2017 or 2020 in preparation for the introduction of more fuel-efficient vehicles,” he said in an opinion piece in Johannesburg-based Business Report newspaper Tuesday. “Our present crude-oil stocks are suitable for producing products of lower specifications, which means we need to stockpile higher-quality grades of crude oil.” |