2018-08-03 09:30:00

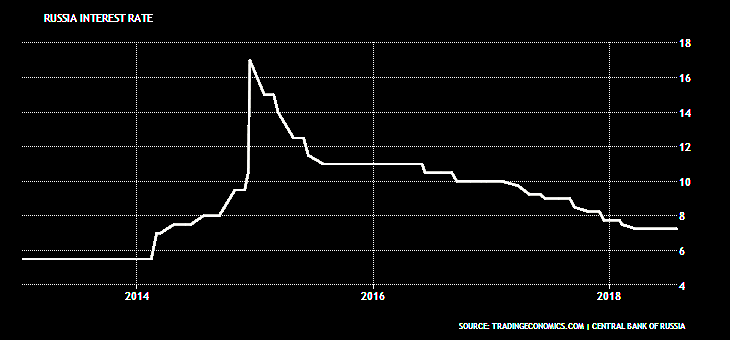

THE BANK OF RUSSIA KEY RATE 7.25%

BANK OF RUSSIA - The Bank of Russia keeps the key rate at 7.25% p.a.

On 27 July 2018, the Bank of Russia Board of Directors decided to keep the key rate at 7.25% per annum. Though annual inflation remains below the target, it is tending to return to 4%. The Bank of Russia forecasts that consumer prices will grow by 3.5–4% year-on-year at the end of 2018 and annual inflation will temporarily overshoot 4% in 2019 due to the planned increase of the value added tax. The annual consumer price growth rate will return to 4% in early 2020.

The balance of risks is shifted towards proinflationary risks. Uncertainty persists over how strongly the tax measures may affect inflation expectations and how the external conditions will develop. In making its key rate decisions the Bank of Russia will assess inflation risks, inflation dynamics and economic developments against the forecast. The Bank of Russia considers that monetary policy is highly likely to shift to a neutral stance in 2019.

Inflation dynamics. Annual inflation remains low. It stood at 2.3% in June and is expected to hold within the 2.5–2.6% range in July in line with the Bank of Russia's forecast. According to Bank of Russia estimates, a majority of annual inflation indicators reflecting the most sustainable price movements suggests that inflation is gradually returning to the target.

Inflation for main consumer basket product groups continued to show mixed dynamics in June. The annual price growth rate in the food market was near zero. Fruit and vegetable prices went down on the back of the last year's high base effect, among other reasons. That said, annual inflation in other food product categories rose from 0.8% in May to 1.1% in June. The annual price growth rate in the non-food market jumped to 3.7% (vs 3.4% seen in May), driven mainly by rising petrochemical prices. Petrol price movements affected inflation expectations which continued to rise in June. Real-time July data show that petrol prices ceased to increase as a result of the decision to cut petrochemical excise taxes. In these circumstances, household inflation expectations stabilised in July. The annual services price growth rate held close to 4% in June.

The Bank of Russia forecasts that annual inflation will stand at 3.5–4% at the end of 2018 and temporarily overshoot 4% in 2019 due to the planned increase of the value added tax. This increase will have a one-off effect on price dynamics. As a result annual consumer price growth rate will return to 4% in early 2020.

Monetary conditions are close to neutral. The Bank of Russia estimates that they are already causing almost no constraining impact on credit, demand and inflation dynamics. Monetary conditions evolve, among other things, under the influence of earlier decisions to cut the key rate. Deposits remain attractive for households at the current interest rate levels. The conservative approach of banks to screening borrowers and the revision of risk ratios on unsecured consumer loans (effective from 1 September 2018) create conditions for lending growth that would pose no risks to price and financial stability.

Given the effect of the planned fiscal measures on inflation and inflation expectations, monetary conditions should remain to some extent tight to limit the scale of secondary effects and stabilise annual inflation close to 4% over the forecast horizon.

Economic activity. The updated Rosstat statistics reflect steadier economic growth in 2017 — early 2018 than previous estimates. It does not materially change the Bank of Russia's view regarding the influence of business activity on inflation, considering that the reviewed data mostly concern investment goods production. The FIFA World Cup made a positive contribution to the annual GDP growth rate in Q2 (0.1–0.2 pps).

The Bank of Russia forecasts that in 2018 the Russian economy will post a 1.5–2% growth rate, which corresponds to its potential amid the remaining structural limitations.

Inflation risks. The balance of risks is shifted towards proinflationary risks. Main risks are related to a high uncertainty over the scale of secondary effects of the adopted tax decisions (primarily, the response of inflation expectations) and the external factors.

With regard to external conditions, accelerated yield growth in advanced economies and geopolitical factors may cause surges in volatility in financial markets and affect expectations for the exchange rate and inflation.

The Bank of Russia leaves mostly unchanged its estimates of risks associated with consumer and oil price volatility, wage movements and possible changes in consumer behaviour. These risks remain moderate.

In making its key rate decisions the Bank of Russia will assess inflation risks, inflation dynamics and economic developments against the forecast. The Bank of Russia considers that monetary policy is highly likely to shift to a neutral stance in 2019.

The Bank of Russia Board of Directors will hold its next key rate review meeting on 14 September 2018. The Board decision press release is to be published at 13:30 Moscow time.

-----

Earlier:

2018, March, 28, 10:45:00

THE BANK OF RUSSIA KEY RATE 7.25%CBRF - On 23 March 2018, the Bank of Russia Board of Directors decided to cut the key rate by 25 bp to 7.25% per annum. Annual inflation remains sustainably low. Inflation expectations are diminishing progressively. The Bank of Russia forecasts annual inflation to be 3-4% in late 2018 and remain close to 4% in 2019. In this environment the Bank of Russia will continue to reduce the key rate and will complete the transition to neutral monetary policy in 2018. |

2017, August, 3, 12:45:00

ИНВЕСТИЦИИ БОЛЬШЕ НА 4%Годовой темп прироста инвестиций в основной капитал во II квартале 2017 года, по оценке Банка России, ускорился до 3,5–4,5%. В III квартале прирост инвестиций сохранится на достаточно высоком уровне – 2,5–4%.

|

2017, August, 3, 12:40:00

БАНК РОССИИ: СТАВКА 9%Банк России принял решение сохранить ключевую ставку на уровне 9,00% годовых.

|

2016, November, 30, 18:50:00

IMF: EXTERNAL RISKS FOR RUSSIAThe expected fiscal consolidation and the subdued nature of the recovery are putting in place the conditions for the central bank to resume, in due course, monetary policy easing in a manner consistent with the 4 percent inflation target. However, the pace of easing should take into account the presence of external risks and the need to build credibility under the newly introduced inflation targeting regime. |