2018-08-10 10:10:00

INDIA'S GROWTH 7.3%

IMF - On July 18, 2018, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with India.

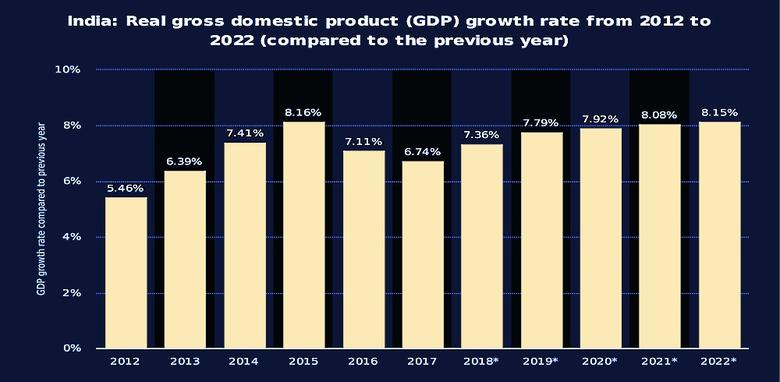

Stability-oriented macroeconomic policies and progress on structural reforms continue to bear fruit. Following disruptions related to the November 2016 currency exchange initiative and the July 2017 goods and service tax (GST) rollout, growth slowed to 6.7 percent in FY2017/18, but a recovery is underway led by an investment pickup. Headline inflation averaged 3.6 percent in FY2017/18, a 17-year low, reflecting low food prices on a return to normal monsoon rainfall, agriculture sector reforms, subdued domestic demand, and currency appreciation. With demand recovering and rising oil prices, medium-term headline inflation has risen to 4.9 percent in May 2018, above the mid-point of the Reserve Bank of India (RBI)'s headline inflation target band of 4 percent ± 2 percent. External vulnerabilities remain contained but have risen. The current account deficit (CAD) widened to 1.9 percent of GDP in FY2017/18, on rising imports and oil prices. Gross international reserves rose to US$424.5 billion (about 8 months of prospective imports of goods and services) at the end of March 2018, but declined to US$407.8 billion in the third week of June 2018. Persistently-high household inflation expectations and large general government fiscal deficits and debt remain key macroeconomic challenges. Systemic macro-financial risks persist, as the weak credit cycle could impair growth and the sovereign-bank nexus has created vulnerabilities.

The near-term macroeconomic outlook is broadly favorable. Growth is forecast to rise to 7.3 percent in FY2018/19 and 7.5 percent in FY2019/20, on strengthening investment and robust private consumption. Headline inflation is projected to rise to 5.2 percent in FY2018/19, as demand conditions tighten, along with the recent depreciation of the rupee and higher oil prices, housing rent allowances, and agricultural minimum support prices. The current account deficit is projected to widen further to 2.6 percent of GDP on rising oil prices and strong demand for imports, offset by a slight increase in remittances. As inflation pressures have risen, monetary policy was tightened in early June 2018. Fiscal consolidation is expected to resume in FY2018/19, with the FY2018/19 Union Budget deficit target of 3.3 percent of GDP (equivalent to 3.6 percent of GDP in IMF terms). Financial sector reforms have been undertaken to address the twin balance sheet problems, as well as to revive bank credit and enhance the efficiency of credit provision by accelerating the cleanup of bank and corporate balance sheets. Over the medium-term, the outlook will continue to improve with growth expected to rise to 7¾ percent, and macro-financial and structural policies are priorities to help boost inclusive growth and harness the demographic dividend.

Economic risks are tilted to the downside. On the external side, risks include a further increase in international oil prices, tighter global financial conditions, a retreat from cross-border integration including spillover risks from a global trade conflict, and rising regional geopolitical tensions. Domestic risks pertain to tax revenue shortfalls related to continued GST implementation issues and delays in addressing the twin balance sheet problems and other structural reforms.

Executive Board Assessment

Executive Directors welcomed the strong economic growth and commended the authorities for the important and wide‑ranging reforms. While noting the broadly positive outlook, Directors observed that risks are tilted to the downside from external factors, such as higher global oil prices and tighter global financial conditions, as well as domestic financial vulnerabilities. Against this background, they underscored the need for continued prudent macroeconomic policies and renewed emphasis on macro‑financial and structural reforms.

Directors noted that continued fiscal consolidation is needed to reduce public debt. They stressed the need to take advantage of the projected acceleration of growth to achieve a public debt level of 60 percent of GDP by FY2022/23, as recommended by India's Fiscal Responsibility and Budget Management Review Committee. Directors also emphasized the need to reach this year's budget target and to take corrective actions if required. In this context, they encouraged the authorities to enhance goods and service tax compliance, while noting the scope for continuing to simplify the framework.

Directors supported the recent tightening of monetary policy. With upside inflation risks, further gradual tightening was likely needed to anchor expectations and maintain monetary policy credibility. Directors welcomed the authorities' commitment to a flexible exchange rate, noting that foreign exchange intervention should remain two‑sided and limited to addressing disorderly market conditions.

Directors stressed the need to focus on macro‑financial and structural policies, and welcomed a range of complementary initiatives taken to address high non‑performing loans in public sector banks and the large corporate sector leverage. They underscored the importance of accelerating the implementation of these initiatives, backed by a comprehensive plan to improve the governance, internal controls, and operations of public sector banks, including by considering more rapid withdrawal of public ownership.

Directors welcomed that the capital flow management framework was moving in the direction of greater liberalization, notably in the area of foreign direct investment. They stressed that India would benefit from further liberalization of trade and foreign investment, and welcomed the authorities' commitment to a multilateral rules‑based trade system.

Directors emphasized the importance of modernizing labor laws and regulations and other measures to help increase formal employment, particularly the employment of women. They considered that these measures would lead to increased productivity growth and help India harness the demographic dividend from the large number of younger workers.

Directors welcomed the important progress that has been made in strengthening the supply side of the economy through large infrastructure investments. Land reforms remain essential to facilitate and expedite infrastructure development, to raise productivity in the agricultural sector, and to foster rapid inclusive growth.

|

India: Selected Social and Economic Indicators, 2014/15–2019/20 1/ |

||||||

|

I. Social Indicators |

||||||

|

GDP (2017/18) |

Poverty (percent of population) |

|||||

|

Nominal GDP (in billions of U.S. dollars): |

2,602 |

Headcount ratio at $1.90 a day (2011): |

21.2 |

|||

|

GDP per capita (U.S. dollars) (IMF staff est.): |

1,942 |

Undernourished (2015): |

14.5 |

|||

|

Population characteristics (2016/17) |

Income distribution (2011, WDI) |

|||||

|

Total (in billions): |

1.32 |

Richest 10 percent of households: |

29.8 |

|||

|

Urban population (percent of total): |

33.1 |

Poorest 20 percent of households: |

8.3 |

|||

|

Life expectancy at birth (years, 2015/16): |

68.3 |

Gini index (2011): |

35.2 |

|||

|

II. Economic Indicators |

||||||

|

2014/15 |

2015/16 |

2016/17 |

2017/18 |

2018/19 |

2019/20 |

|

|

Est. |

Projections |

|||||

|

Growth (in percent) |

||||||

|

Real GDP (at market prices) |

7.4 |

8.2 |

7.1 |

6.7 |

7.3 |

7.5 |

|

Industrial production |

4.0 |

3.3 |

4.6 |

4.4 |

… |

… |

|

Prices (percent change, period average) |

||||||

|

Consumer prices - Combined |

5.8 |

4.9 |

4.5 |

3.6 |

5.2 |

4.8 |

|

Saving and investment (percent of GDP) |

||||||

|

Gross saving 2/ |

33.0 |

30.7 |

29.7 |

28.8 |

29.6 |

30.0 |

|

Gross investment 2/ |

34.2 |

31.8 |

30.3 |

30.6 |

32.2 |

32.2 |

|

Fiscal position (percent of GDP) 3/ |

||||||

|

Central government overall balance |

-4.5 |

-4.1 |

-3.7 |

-4.0 |

-3.6 |

-3.5 |

|

General government overall balance |

-7.2 |

-7.0 |

-6.7 |

-7.0 |

-6.6 |

-6.5 |

|

General government debt 4/ |

67.8 |

69.6 |

68.9 |

70.4 |

68.7 |

67.2 |

|

Cyclically adjusted balance (% of potential GDP) |

-7.1 |

-7.1 |

-6.7 |

-6.9 |

-6.6 |

-6.5 |

|

Cyclically adjusted primary balance (% of potential GDP) |

-2.4 |

-2.4 |

-1.8 |

-1.9 |

-1.6 |

-1.6 |

|

Money and credit (y/y percent change, end-period) |

||||||

|

Broad money |

10.9 |

10.1 |

10.1 |

9.5 |

11.4 |

11.8 |

|

Bank credit to the private sector |

9.3 |

10.6 |

8.0 |

9.8 |

13.6 |

13.3 |

|

Financial indicators (percent, end-period) |

||||||

|

91-day treasury bill yield (end-period) |

8.3 |

7.3 |

5.8 |

6.1 |

… |

… |

|

10-year government bond yield (end-period) |

7.8 |

7.5 |

6.7 |

7.4 |

… |

… |

|

Stock market (y/y percent change, end-period) |

24.9 |

-9.4 |

16.9 |

11.3 |

… |

… |

|

External trade (on balance of payments basis) |

||||||

|

Merchandise exports (in billions of U.S. dollars) |

316.5 |

266.4 |

280.1 |

309.0 |

349.7 |

385.0 |

|

(Annual percent change) |

-0.6 |

-15.9 |

5.2 |

10.3 |

13.2 |

10.1 |

|

Merchandise imports (in billions of U.S. dollars) |

461.5 |

396.4 |

392.6 |

469.0 |

546.6 |

592.2 |

|

(Annual percent change) |

-1.0 |

-14.1 |

-1.0 |

19.5 |

16.5 |

8.3 |

|

Terms of trade (G&S, annual percent change) |

3.0 |

6.0 |

1.4 |

-2.8 |

-2.9 |

1.8 |

|

Balance of payments (in billions of U.S. dollars) |

||||||

|

Current account balance |

-26.8 |

-22.1 |

-15.2 |

-48.7 |

-70.6 |

-68.3 |

|

(In percent of GDP) |

-1.3 |

-1.1 |

-0.7 |

-1.9 |

-2.6 |

-2.2 |

|

Foreign direct investment, net ("-" signifies inflow) |

-31.3 |

-36.0 |

-35.6 |

-30.3 |

-38.7 |

-47.1 |

|

Portfolio investment, net (equity and debt, "-" = inflow) |

-42.2 |

4.1 |

-7.6 |

-22.1 |

-0.9 |

-7.3 |

|

Overall balance ("-" signifies balance of payments surplus) |

-61.4 |

-17.9 |

-21.6 |

-43.6 |

4.2 |

-14.4 |

|

External indicators |

||||||

|

Gross reserves (in billions of U.S. dollars, end-period) |

341.6 |

360.2 |

370.0 |

424.5 |

420.4 |

434.7 |

|

(In months of next year's imports (goods and services)) |

8.5 |

8.9 |

7.6 |

7.5 |

6.8 |

6.5 |

|

External debt (in billions of U.S. dollars, end-period) |

474.7 |

485.0 |

471.8 |

514.4 |

559.3 |

609.5 |

|

External debt (percent of GDP, end-period) |

23.3 |

23.1 |

20.8 |

19.8 |

20.2 |

20.0 |

|

Of which: Short-term debt 5/ |

9.1 |

9.1 |

9.1 |

8.4 |

9.0 |

9.2 |

|

Ratio of gross reserves to short-term debt (end-period) |

1.8 |

1.9 |

1.8 |

1.9 |

1.7 |

1.5 |

|

Debt service ratio 6/ |

7.6 |

8.8 |

7.8 |

7.9 |

8.3 |

8.5 |

|

Real effective exchange rate (annual avg. percent change) |

7.0 |

5.8 |

1.6 |

3.1 |

… |

… |

|

Exchange rate (rupee/U.S. dollar, end-period) |

62.6 |

68.3 |

64.8 |

65.0 |

… |

… |

|

Memorandum item (in percent of GDP) |

||||||

|

Fiscal balance under authorities' definition |

-4.1 |

-3.9 |

-3.5 |

-3.5 |

-3.3 |

-3.2 |

|

Sources: Data provided by the Indian authorities; Haver Analytics; CEIC Data Company Ltd; Bloomberg L.P.; World Bank, World Development Indicators; |

||||||

|

and IMF staff estimates and projections. |

||||||

|

1/ Data are for April–March fiscal years. |

||||||

|

2/ Differs from official data, calculated with gross investment and current account. Gross investment includes errors and omissions. |

||||||

|

3/ Divestment and license auction proceeds treated as below-the-line financing. |

||||||

|

4/ Includes combined domestic liabilities of the center and the states, and external debt at year-end exchange rates. |

||||||

|

5/ Short-term debt on residual maturity basis, including estimated short-term NRI deposits on residual maturity basis. |

||||||

|

6/ In percent of current account receipts, excluding grants.

|

||||||

-----

Earlier:

2018, August, 8, 11:55:00

INDIA'S OIL IMPORTS UPREUTERS - Indian refiners’ interest in U.S. crude will be welcome news to shale producers looking for buyers outside of China, which is likely to scale back imports as the trade dispute between the administration of President Donald Trump and Beijing escalates. |

2018, August, 6, 12:45:00

INDIA VS CHINA POPULATIONWBG - China, with 1.4 billion people, is the most populous country in the world in 2017. However, India, the second most populous country with 1.3 billion people, is projected to surpass China’s population by 2022. China’s total fertility rate (the number of children per woman) has also declined sharply since the 1970s. |

2018, July, 25, 09:40:00

IRANIAN OIL FOR INDIA: №2REUTERS - India, Iran’s top oil client after China, shipped in 5.67 million tonnes, or about 457,000 barrels per day (bpd), of oil, from the country in the first three months of this fiscal year, Dharmendra Pradhan told lawmakers in a written reply. |

2018, July, 25, 09:05:00

INDIA'S NUCLEAR POWERWNN - India is in active talks with French and US companies on projects to build new nuclear power plants at Jaitapur and Kovvada, the country's minister of state, Jitendra Singh, has confirmed to parliament. |

2018, June, 27, 10:45:00

ARABIAN INVESTMENT FOR INDIA: $44 BLNAOG - Sheikh Abdullah said: “This agreement strengthens the already close ties between the UAE and the Kingdom of Saudi Arabia and between the UAE and India. The UAE is unwavering in its commitment to its strategic multi-lateral relationships with both Saudi Arabia and India, as well as being a reliable partner in India’s energy security. We look forward to exploring further opportunities to expand our energy partnerships and to collaborating on new, broader, opportunities that will further strengthen and deepen the long-standing economic links between our three countries.” |

2018, May, 30, 13:45:00

INDIA IGNORES SANCTIONSBLOOMBERG - India, a long-time buyer of oil from both Iran and Venezuela, only complies with United Nations-mandated sanctions and not those imposed by one country on another, said foreign minister Sushma Swaraj at a press conference in New Delhi on Monday. |

2018, May, 16, 12:15:00

INDIA'S OIL DEMAND UP 4.5%BLOOMBERG - India’s oil consumption surged 4.5 percent in April as industrial activity gathered pace in Asia’s third-largest economy and sales of trucks and buses soared. |