2018-09-21 10:45:00

UNEXPECTED OIL PRICES

SHANA - Oil market has been experiencing special conditions in recent months. On one hand, oil prices have followed an upward trend while on the other, US President Donald Trump is imposing oil sanction on Iran and calling on OPEC countries to help his anti-Iran campaign.

However, Iran's former national representative to OPEC Javad Yarjani says Iran may not be completely driven out of global oil market as it sits atop the world's largest hydrocarbon reserves.

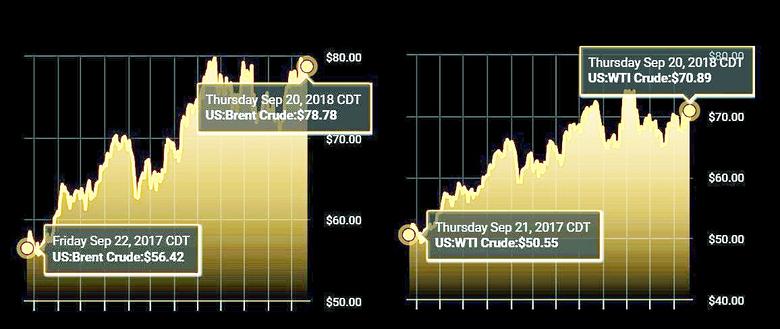

Oil prices have seen ups and downs over the past one year and particularly after Donald Trump took office as US president in January 2017. Over recent months, oil prices have gained ground. What do you think of the future of oil prices? Will this upward trend continue in the coming months?

What is common in oil market is that no price levels could be forecast for the future there. Only its unpredictability is predictable. Rarely may you find an expert to say with full certainty in which direction oil prices are headed. A variety of factors are involved in the oil market, some of which are fundamental and directly affect prices; like supply and demand and volume of reservoirs. In the meantime, there are some other factors like geopolitical issues, wars and political disputes between producers and consumers, which are not among fundamental factors but indirectly, affect prices. Therefore, one cannot say with certainty where the prices are headed now.

However, what has happened over the past one year has driven up oil prices, which was predictable.

We have to note that based on events that preceded the US's pullout from the JCPOA (Iran's nuclear deal with six world powers), it might be argued that the prices would move up. The reason is clear. Major oil exporting countries had concluded that prices needed to go up. Some of producers were faced with budget deficit or for example Saudi Arabia is planning to list Aramco shares on stock market. Therefore, a variety of factors were unified so that high oil prices would be in the best interests of producers. It may be concluded that the upward trend of oil prices was the outcome of OPEC-non-OPEC in 2016.

But in this decision, OPEC was not the only factor as non-OPEC producers led by Russia, were also involved in the upward trend of oil prices.

Yes, of course! By that time Russia was restructuring its own economy and army. Therefore, revenue from oil and gas exports largely helped Russia reach its economic and security objectives. The unfavorable conditions prevailing in the oil market in 2016 and the price slump to below $30 in that year in January pushed Russia as the largest non-OPEC producer and exporter of oil to close ranks with OPEC for driving prices up.

But after the US's unilateral pullout from the JCPOA and President Trump's announcement of planned re-imposition of sanctions on Iran in November, the prices were up again. It was predictable, wasn't it?

We cannot yet say where the prices would go for sure. On one hand, the possible exit of part of Iran's oil from the market would drive prices up, but on the other, there are allegations that certain countries can fill Iran's void in the market. That remains shrouded in ambiguity and may not be solid-based. Now we have to see whether such claims would be translated into action or they would be limited to words. Therefore, I reiterate once more that we cannot say with certainty which direction the prices would take.

Speculation continues about oil price hikes after Iran's elimination from the market. Conflicting figures have been bandied about, from $100 to $400.

If we start from the pessimistic aspect, we should keep in mind that never have such figures as $400 been experienced in the oil history. That may happen when a group of oil producers quit supply in the market altogether, which is unlikely to happen. Furthermore, the global economy cannot tolerate prices above $100 a barrel, and conditions would get tough. Several years ago we experienced $140 prices. I remember well the world economy was fraught with concerns. It was not limited to consumers. OPEC was also worried about high oil prices because sustained high prices could seriously damage the global economy and minimize demand. Therefore, everyone helped keep prices within a certain limit. For its part, OPEC adopted decisions which would help reduce prices. Of course, the global economic crisis finally sharply drove down prices to below $40 a barrel in December that year. OPEC cut 1.2 million from its output in a bid to keep the price decline in check.

As far as Iran's exit from oil market is concerned, I don't think they could completely drive Iran out. First and foremost, no country will accept to be deprived of its main source of exports, and Iran would use every tool at its disposal to sell its oil and will not bow to US demands. Second, we have to see what position Europe, China and India would take after Iran's oil export is sanctioned. All these issues may affect the prices. But it is evident that political intervention in the oil market would lead to more negative results for global economy.

How can issues like President Trump's offer of unconditional talks with Iran affect oil prices?

I reiterate that the complicated structure of oil market would not allow any definite forecast on this issue. All of us know that oil is traded on paper not physically.

The way oil news is reflected and oil market analyses impact the minds of billionaires who are investing in the oil market because they buy and sell oil based on reports of price reporting agencies and of course in the hope of higher oil prices.

The US is unlikely to be able to fully ban Iran's oil sales in light of current global economic conditions. Anyway, the US is imposing unlawful and unilateral sanctions on Iran's petroleum sector. Iran is not subject to international embargo and the European Union has thus far shown support for Iran. That is why oil market conditions have got complicated.

Yes, that's it. Many analysts are of the opinion that Iran may by no means be dropped off the oil market. Even if the Trump administration intends to risk such a thing, it has to wait for its impacts on regional geopolitics, global economy and the Middle East. Iran's oil enjoys a significant standing in global economy. Many countries are well aware that in case Iran's oil exports are completely cut the global economy will be affected.

Some countries like Saudi Arabia have announced their readiness to provide any extra oil. Iran has not been mentioned directly, but it goes without saying that Saudi Arabia meant it would make up for any shortages resulting from the imposition of sanctions on Iran. Of course other countries like Kuwait and Iraq have also raised their output. Do you think that Saudi Arabia will be able to supply extra oil in case Iran's oil is dropped off the market?

Under the current circumstances, the oil market conditions have become extremely complicated. On one side, Trump imposes sanctions on Iran's oil and on the other he calls on Saudi Arabia to raise its output by 2 mb/d. Saudi Arabia responded to the US without making clear whether or not it would be able to boost its output by 2 mb/d.

To be realistic, Saudi Arabia has largely invested in its petroleum industry in recent years as it did not face restrictions created for Iran's petroleum industry due to international sanctions. As a result, Saudi Arabia says it would be able to bring its production to more than 12.5 mb/d. In the meantime, analysts believe that even if Saudi Arabia manages to supply 12.5 mb/d such output trend would not be sustainable.

In case Saudi Arabia decides to produce oil at full capacity, the global oil production surplus will decline and it would plunge the oil market into complicated and dangerous conditions. Suppose that an unpredictable war breaks out or an oil producer experiences a sharp slump in production. Under such circumstances, extra production capacity would rush to help the economy by giving assurances that sufficient oil would be available for consumption all across the globe.

According to secondary sources, Saudi Arabia's production level has been close to 11 mb/d over the past 18 years, which is now below 10.5 mb/d. Of course Saudi Arabia has boosted its production capacity, but experts believe that it could not fully compensate for shortages emanated from embargo on Iran's oil and that would negatively affect the market.

Secondary sources also confirm that Iraq, Kuwait and United Arab Emirates raised their production in July. To what extent do you think these countries would be able to make up for shortages in the market?

Before answering your question, I deem it necessary to say that over recent years we have witnessed investment by some OPEC members with a view to increasing their oil production. However, due to financial issues or special political conditions we have seen that their production has not increased as planned. Now in response to your question, we have to take into consideration a variety of parameters. First and foremost, everyone knows that eliminating Iran from the global oil market would in the long term leave negative impacts on the global economy. Although some countries have said they would be able to make up for supply shortages the main question is to know if they would be able to raise their output sustainably and on the long term. Second, OPEC member states increase their production within the framework of the organization's policy. Now, if they supply more than their allocated quota to bring down oil prices, will their budget face any problem? Naturally, these must be a balance in decisions. I don't think that these countries would be able even collectively to make up for Iran's oil shortage in the global markets.

What do you think of the current level of interaction among OPEC member states?

Rarely did someone think of cooperation among OPEC member states in the 174th meeting of the OPEC Conference. Despite all pressure exerted by the US government on member states to increase production, you said that OPEC decided to stick with the 2016 production ceiling. That was a breakthrough for OPEC. If we base everything on the past, it seems that OPEC would get off this crisis, too. Should it fail to overcome this crisis, the countries that sought to undermine OPEC would realize their objectives. However, one thing is clear; elimination of OPEC would further harm countries favoring its collapse.

The Russians have also claimed that they could boost their production by more than 200,000 b/d. Is that true?

You must know that in the aftermath of the collapse of the Union of Soviet Socialist Republics (USSR), Russian oil firms have made great success in boosting their oil production, raising their output from 6.25 mb/d in 2000 to nearly 12 mb/d in collaboration with international companies. But now their combined output stands at 11 mb/d. We also know that Russian companies are under sanctions and it is not clear if they would be able to add 200,000 b/d to their output. The figures given by Russian firms for output hike are for marketing purposes.

However, I believe that none of oil exporting countries must accompany sanctions against other producing nations because oil embargo would definitely affect the economy on the global scale. If assurances are given of sufficient oil supply, sustained oil embargo would gradually harm every other country and the same nations are likely to face sanctions one day. Therefore, the minimum action to be taken by OPEC member states is to close ranks, which would benefit both producers and consumers.

In your view, does Mr. Trump favor high or low oil prices? When we juxtapose oil embargo on Iran and Venezuela we conclude that the current US administration is not interested in oil price decline.

This issue can't be deal with so simply. It is no secret to anyone that due to the incorporation of driving private cars in the American citizens' everyday life, high gasoline price is a key factor in that country. Therefore, high oil prices would push gasoline prices, which would cause public discontent among Americans. In light of the key November elections in the US, Mr. Trump does not seem to be favoring oil price hikes at least until elections end.

US shale oil companies favor high oil prices in order to pocket more profits. It is noteworthy that following the OPEC agreement in November 2014 and the subsequent flow of oil to market we witnessed a sharp fall in oil prices. That pushed shale oil producers to reduce costs and make their production economical. Therefore, in case oil prices fall again the shale oil firms would not halt work. On the other hand, oil production has jumped significantly in the US and this country is likely to become an oil exporter. That is why this group of producers prefers higher oil prices. Major international oil companies in the US favor price hikes to the extent to justify future investment in this industry so that the rate of return on investment in oil would be lucrative enough. Therefore, it is hard to say with certainty whether or not the US is after increasing or decreasing oil prices.

What price do you think the US economy favors now?

The price of each gallon of gasoline in the US for end-user is a key factor in the application of policies in that country. As an importer and consumer of oil, they do not agree with high oil prices 100 percent. On the other hand, since oil producing countries there, particularly shale producers, would be able to develop under conditions of high oil prices, they oppose very low prices. Therefore, due to the conflict of interests in that country, the current level of prices must serve the interests of all these groups.

On one hand Mr. Trump claims to be seeking unconditional talks with Iran, while on the other, he is imposing stiff sanctions on Iran. He has also called on countries doing business with Iran to pull out of Iran or face penalties. In your view, is Mr. Trump reliable in his claims about Iran?

Apart from his track record in the first four-year term in office, every president in the US is willing to mark history in the second round of his presidency if his reelected. For instance, the Nixon administration is known for the resumption of ties with China although he failed to serve out his second term in office. Or Mr. [Bill] Clinton sought in vain to reestablish diplomatic ties with Iran. Mr. [Barack] Obama was also willing to resume full diplomatic ties with Iran, but he failed, too. Now, despite all his threats against Iran, Mr. Trump may be seeking to undo all achievements of Mr. Obama, the former US president. That is in full harmony with Zionist regime's anti-Iran policy. Therefore, expression of readiness for unconditional talks with Iran seems to be aimed at causing further vision inside Iran. In his possible second term in office, Mr. Trump will be trying to register a positive track record. Resolution of hostility with Iran after 40 years could be a marking event in the name of Mr. Trump.

-----

Earlier:

2018, September, 19, 14:07:00

OIL PRICE: NEAR $79 AGAINREUTERS -Brent crude futures LCOc1 were up 2 cents at $79.05 a barrel by 0854 GMT, having gained 1.3 percent on Tuesday following media reports that Saudi Arabia, the world’s largest oil exporter, was comfortable with prices above $80. U.S. crude futures CLc1 were up 15 cents at $70.00, after gaining 1.4 percent the day before. |

2018, September, 19, 13:47:00

OIL PRICES: $70 - $80PLATTS - Current global oil prices at around $70-80/b are due to the volatile situation on the market and include a premium for risks associated with sanctions and oil supply cuts, but they are expected to fall to around $50/b in the long term, Russian energy minister Alexander Novak said Tuesday.

|

2018, September, 17, 15:20:00

РОССИЯ И САУДОВСКАЯ АРАВИЯ: СТАБИЛЬНОСТЬ НА РЫНКЕМИНЭНЕРГО РОССИИ - Министры обсудили динамику спроса и предложения на рынке с фокусом на макроэкономические тренды и потенциальные сценарии развития ситуации в среднесрочной перспективе. Стороны подтвердили приверженность обеспечению стабильности на рынке и готовность оперативно реагировать на изменения рыночной конъюнктуры, чтобы совместно с партнерами обеспечить стабильность рынка в любых условиях.

|

2018, September, 14, 12:40:00

IEA: OIL PRICES COULD RISEIEA - If Venezuelan and Iranian exports do continue to fall, markets could tighten and oil prices could rise without offsetting production increases from elsewhere.

|

2018, September, 12, 11:35:00

OIL PRICES 2018-19: $73-$74U.S. EIA - EIA expects Brent spot prices will average $73/b in 2018 and $74/b in 2019. EIA expects West Texas Intermediate (WTI) crude oil prices will average about $6/b lower than Brent prices in 2018 and in 2019. NYMEX WTI futures and options contract values for December 2018 delivery that traded during the five-day period ending September 6, 2018, suggest a range of $56/b to $85/b encompasses the market expectation for December WTI prices at the 95% confidence level. |

2018, August, 8, 12:05:00

OIL PRICES 2018 - 19: $72 - $71EIA - Brent crude oil spot prices averaged $74 per barrel (b) in July, largely unchanged from the average in June. EIA expects Brent spot prices will average $72/b in 2018 and $71/b in 2019. EIA expects West Texas Intermediate (WTI) crude oil prices will average about $6/b lower than Brent prices in 2018 and in 2019.

|

2018, July, 11, 09:25:00

OIL PRICES 2018 - 19: $73 - $69EIA - Brent crude oil spot prices averaged $74 per barrel (b) in June, a decrease of almost $3/b from the May average. EIA forecasts Brent spot prices will average $73/b in the second half of 2018 and will average $69/b in 2019. EIA expects West Texas Intermediate (WTI) crude oil prices will average $6/b lower than Brent prices in the second half of 2018 and $7/b lower in 2019. NYMEX WTI futures and options contract values for October 2018 delivery that traded during the five-day period ending July 5, 2018, suggest a range of $56/b to $87/b encompasses the market expectation for October WTI prices at the 95% confidence level. |