2018-09-21 10:20:00

WORLD OIL DEMAND: 100.23 MBD

OPEC - Monthly Oil Market Report September 2018

Oil Market Highlights

Crude Oil Price Movements

In August, the OPEC Reference Basket declined by $1.01 m-o-m, settling at $72.26/b. Crude oil futures were also down for the month. Price declines were mainly due to worries that the ongoing global trade disputes would lower oil demand, strengthening US dollar, US stock builds and reported supply increases. ICE Brent was $1.11 lower at $73.84/b compared to the previous month, while NYMEX WTI was down $2.74 at $67.85/b and DME Oman dropped 24¢ to $72.67/b. However, year-to-date (y-t-d) ICE Brent was still $19.86 higher at $72.00/b, while NYMEX WTI increased by $17.12 to $66.42/b and DME Oman was up $18.70 at $69.55/b. The Brent-WTI spread widened to average $6.00/b. Speculative net long positions ended mixed, with those of NYMEX WTI lower. As for market structure, the backwardation in Dubai remained unchanged, while that of WTI eased. The contango structure for Brent for the rest of the year deepened amid increasing supplies. The discount of sour to sweet crudes decreased due to an anticipated tightening of sour crude, while sweet crude availability was ample.

World Economy

The global GDP growth forecast remains at 3.8% for 2018 and 3.6% for 2019. In the OECD, growth in the US is assessed unchanged at 2.9% in 2018 and 2.5% in 2019. Euro-zone growth remains at 2.0% for 2018 and 1.9% for 2019. GDP growth in Japan is revised down by 0.1 pp to 1.1% in both 2018 and 2019.

Meanwhile, in the non-OECD, India's forecast is revised up to 7.6% for 2018, while remaining unchanged at 7.4% for 2019. China's GDP growth remains at 6.6% for 2018 and 6.2% for 2019. Growth in Brazil is revised down by 0.4% to reach 1.2% in 2018, but a rebound to 2.0% is anticipated in 2019. Russia's GDP growth forecast is also revised lower to 1.6% in 2018 and down to 1.7% in 2019.

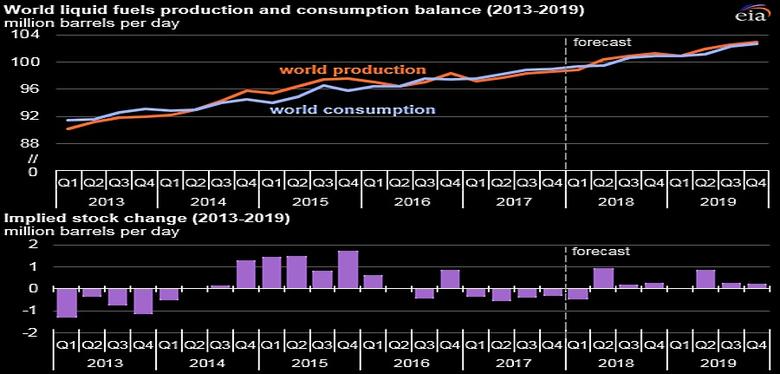

World Oil Demand

In 2018, world oil demand is expected to grow by 1.62 mb/d, a minor downward revision from last month's projection. In the OECD region, oil demand saw healthy growth in all three main OECD regions, particularly in the Americas over 1H18. In contrast, the non-OECD region, mainly Latin America and the Middle East, saw weaker oil requirements in 1H18 as well as slower economic projections, which has led to a net downward revision of 20 tb/d from last month's report. Total oil demand for 2018 is now estimated at 98.82 mb/d. In 2019, world oil demand growth is forecast to rise by 1.41 mb/d, a minor downward adjustment of 20 tb/d from the previous month's assessment, mainly reflecting the less optimistic economic projections in the non-OECD regions of Latin America and the Middle East compared to last month. Total world oil demand in 2019 is now projected to surpass 100 mb/d for the first time and reach 100.23 mb/d.

World Oil Supply

Non-OPEC oil supply in 2018 is expected to grow by 2.02 mb/d, a downward revision of 64 tb/d. The US, Canada, Kazakhstan the UK, and Brazil remain to be the main drivers for growth, while Mexico and Norway are projected to show the largest declines. Total non-OPEC supply for 2018 is now estimated at 59.56 mb/d.

Non-OPEC oil supply in 2019 is forecast to grow by 2.15 mb/d, a minor upward revision of 17 tb/d. The US, Brazil, Canada, and the UK are expected to be the main growth drivers, while Mexico and Norway remain to be the largest declines. Non-OPEC supply is now forecast to average 61.71 mb/d for the year. OPEC NGLs in 2018 and 2019 are expected to grow by 0.12 mb/d and 0.11 mb/d to average 6.36 mb/d and 6.47 mb/d, respectively. In August, OPEC crude oil production increased by 278 tb/d to average 32.56 mb/d, according to secondary sources.

Product Markets and Refining Operations

Refinery margins at all main trading hubs recorded gains in August as several refinery outages prompted product supply disruptions, which led to strengthening at the top and middle of the barrel. In the US, product markets strengthened, supported mainly by higher product exports, particularly to Latin America. In Europe, declining Amsterdam-Rotterdam-Antwerp product inventories resulted in tighter product balances, which provided substantial support to refining margins. Meanwhile in Asia, refining margins strengthened on the back of lower refinery intakes caused by unplanned shutdowns and bullish market sentiment.

Tanker Market

In August, dirty vessel spot freight rates increased by 5% on average compared to a month earlier. This was mainly driven by higher freight rates for VLCC and Aframax, while average Suezmax freight rates showed a decline. Enhanced activity and delays on the US Gulf Coast (USGC) and Asia supported freight rates in August. In the clean tanker market, spot freight rates remained under pressure as high vessel availability continued, while tonnage demand remained limited, therefore resulting in rate declines in both the eastern and western directions of Suez.

Stock Movements

Data for July showed that total OECD commercial oil stocks rose by 8.1 mb m-o-m, standing at 2,830 mb, which is 194 mb lower than a year ago and 43 mb below the latest five-year average, but remain 260 mb above the January 2014 level. Compared to the latest five-year average, crude stocks indicated a deficit of 0.2 mb, while product stocks witnessed a deficit of 43 mb. In terms of days of forward demand cover, OECD commercial stocks rose by 0.1 days m-o-m in July to stand at 59.1 days, which is 2.3 days below the latest five-year average.

Balance of Supply and Demand

In 2018, demand for OPEC crude is expected at 32.9 mb/d, which is 0.5 mb/d lower than in the previous year. In 2019, demand for OPEC crude is forecast at 32.1 mb/d, around 0.9 mb/d lower than a year earlier.

More information is here.

-----

Earlier:

2018, September, 19, 14:07:00

OIL PRICE: NEAR $79 AGAINREUTERS -Brent crude futures LCOc1 were up 2 cents at $79.05 a barrel by 0854 GMT, having gained 1.3 percent on Tuesday following media reports that Saudi Arabia, the world’s largest oil exporter, was comfortable with prices above $80. U.S. crude futures CLc1 were up 15 cents at $70.00, after gaining 1.4 percent the day before. |

2018, September, 19, 13:47:00

OIL PRICES: $70 - $80PLATTS - Current global oil prices at around $70-80/b are due to the volatile situation on the market and include a premium for risks associated with sanctions and oil supply cuts, but they are expected to fall to around $50/b in the long term, Russian energy minister Alexander Novak said Tuesday. |

2018, September, 17, 15:20:00

РОССИЯ И САУДОВСКАЯ АРАВИЯ: СТАБИЛЬНОСТЬ НА РЫНКЕМИНЭНЕРГО РОССИИ - Министры обсудили динамику спроса и предложения на рынке с фокусом на макроэкономические тренды и потенциальные сценарии развития ситуации в среднесрочной перспективе. Стороны подтвердили приверженность обеспечению стабильности на рынке и готовность оперативно реагировать на изменения рыночной конъюнктуры, чтобы совместно с партнерами обеспечить стабильность рынка в любых условиях. |

2018, September, 12, 11:35:00

OIL PRICES 2018-19: $73-$74U.S. EIA - EIA expects Brent spot prices will average $73/b in 2018 and $74/b in 2019. EIA expects West Texas Intermediate (WTI) crude oil prices will average about $6/b lower than Brent prices in 2018 and in 2019. NYMEX WTI futures and options contract values for December 2018 delivery that traded during the five-day period ending September 6, 2018, suggest a range of $56/b to $85/b encompasses the market expectation for December WTI prices at the 95% confidence level. |

2018, September, 5, 10:55:00

SAUDIS OIL PRICE: $70 - $80REUTERS - “The Saudis need oil at about $80 and they don’t want prices to go below $70. They want to manage the market like this,” one of the sources told. |

2018, August, 8, 12:05:00

OIL PRICES 2018 - 19: $72 - $71EIA - Brent crude oil spot prices averaged $74 per barrel (b) in July, largely unchanged from the average in June. EIA expects Brent spot prices will average $72/b in 2018 and $71/b in 2019. EIA expects West Texas Intermediate (WTI) crude oil prices will average about $6/b lower than Brent prices in 2018 and in 2019. |

2018, July, 12, 10:45:00

OPEC: OIL DEMAND UP BY 1.65 MBDOPEC - In 2018, oil demand is expected to grow by 1.65 mb/d, unchanged from the previous month’s assessment, with expectations for total world consumption at 98.85 mb/d. In 2019, the initial projection indicates a global increase of around 1.45 mb/d, with annual average global consumption anticipated to surpass the 100 mb/d threshold. The OECD is once again expected to remain in positive territory, registering a rise of 0.27 mb/d with the bulk of gains originating in OECD America. The non-OECD region is anticipated to lead oil demand growth in 2019 with initial projections indicating an increase of around 1.18 mb/d, most of which is attributed to China and India. Additionally, a steady acceleration in oil demand growth is projected in Latin America and the Middle East. |