2019-10-16 11:55:00

MEXICO'S GROWTH 0.4%

IMF - October 11, 2019 - Economic growth has slowed sharply in an environment of elevated external and domestic risks. Nevertheless, the authorities' commitment to very strong policies and policy frameworks is reassuring. The challenge is to create conditions for strong, sustained, and inclusive growth, while maintaining macroeconomic stability. To this end, the mission recommends: (i) pursuing a more growth-friendly and inclusive fiscal policy mix that puts debt on a downward path, notably by raising non-oil revenues and improving the efficiency of spending; (ii) easing monetary policy further if inflation remains close to target and inflation expectations remain anchored; (iii) boosting financial inclusion and strengthening financial system resilience; and (iv) re-invigorating structural reforms, including steps to reduce corruption and crime

Context, outlook, and risks

1. Strong fundamentals have contributed to Mexico's resilience. The authorities' commitment to fiscal prudence is strong, monetary policy has succeeded in bringing inflation to target, and financial sector supervision and regulation remain robust. The flexible exchange rate is playing a key role in helping the economy adjust to external shocks. Mexico's external position remains broadly consistent with medium-term fundamentals and desirable policy settings. These strong policies have been instrumental in allowing Mexico to navigate a complex external environment successfully.

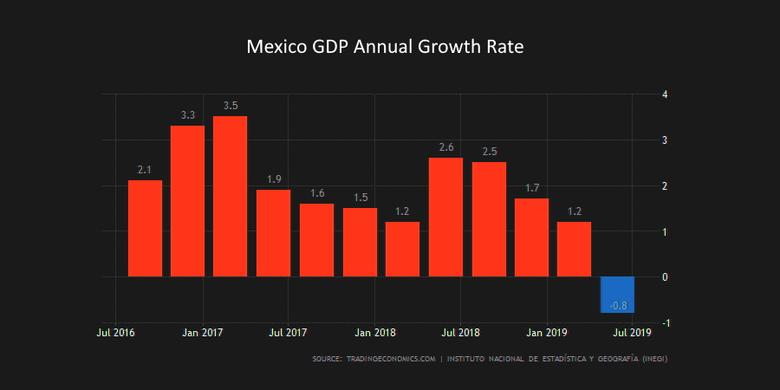

2. But growth has declined sharply, and fiscal pressures are mounting. Fiscal pressures have emerged in the context of new policy priorities and a commitment to not raise taxes during the first half of the administration's term. Drastic budget cuts raise concerns about their sustainability and their potential impact on human capital, while productivity-enhancing reforms have largely stalled.

3. The mission projects near-term growth to pick up only slowly and inflation to continue falling. Growth is projected to reach 0.4 percent in 2019, and to accelerate to 1.3 percent in 2020 on the back of a modest recovery in domestic demand as uncertainty subsides and monetary conditions ease further. Headline inflation is at Banxico's 3-percent target, while core inflation is expected to converge to it by mid-2020.

4. The balance of risks is tilted to the downside. The main external risks include weaker-than-projected global growth, volatility in global financial markets, and continued uncertainty about Mexico's trade relations with the U.S. On the domestic front, medium-term growth could be lower, and investors could reconsider Mexico's credit quality, should the administration weaken its commitment to fiscal prudence, strong institutions, and a favorable business environment. A downgrade of Pemex to non-investment status by a second major rating agency could lead to higher financing costs and spillovers to other corporations. On the other hand, concrete steps to enhance good governance and the rule of law, and advance structural reforms, would provide upside risks to growth.

Fiscal policy and structural fiscal reforms

5. The mission welcomes the commitment to fiscal prudence, but stresses the need for more ambitious targets to put the public debt ratio on a downward path. Keeping the PSBR at 2.2-2.4 percent of GDP over the medium term, as envisaged in the authorities' plans, would keep debt broadly stable at around 55 percent of GDP. While this level is sustainable in staff's view, more ambitious medium-term fiscal targets would help rebuild buffers and insure against downside risks and demographics-related spending pressures.

6. Additional measures are needed to meet the announced fiscal targets. The mission is of the view that budget projections are based on optimistic assumptions for nominal GDP growth, oil production, and tax revenue buoyancy, and remains concerned about the projected significant compression of spending on goods and services. Meeting the announced fiscal targets would require closing an emerging fiscal gap of 0.5-1.5 percent of GDP during 2020-24 with concrete actions; this would be imperative to safeguard the credibility of fiscal policy.

7. The authorities' top priority should be to raise non-oil tax revenues while making the tax system more progressive . Mexico's revenue performance significantly lags that of regional and international peers, with a strikingly weak VAT collection. The mission thus urges the authorities to undertake a comprehensive review of the tax system with a view to bringing forward plans for rationalizing tax expenditures and broadening the tax base. Consideration should be given to:

VAT. Taxing (non-export related) food items at the standard 16 percent rate alone would boost revenues by some 1 percent of GDP, while targeted benefits could offset the impact on the poor (an initially reduced rate could smooth the transition to the standard rate).

Income taxes. Rationalizing inefficient and regressive tax expenditures and widening the PIT top bracket could boost revenues and increase progressivity.

Excises. Guaranteeing retail fuel price growth below inflation by reducing the excise rate subject to a zero floor disproportionately benefits the rich and should be abolished.

Local taxes A reform of both the property and vehicle registration taxes would allow for a reduction in central government transfers to states and municipalities and thus encourage fiscal responsibility.

Border tax regime. This temporary (for 2019 and 2020) special policy regime creates distortions and likely erodes the tax base and should thus be abolished immediately or at least not be extended.

Tax administration. The mission welcomes recent steps to improve tax administration, namely: (i) the abolition of the right to offset excess VAT credits against other taxes; and (ii) strengthening sanction for tax evasion and closing loopholes. To further reduce fraud and improve compliance, the mission recommends adopting a comprehensive strategy to tackle VAT non-compliance in line with the recommendations of the recent Fund technical assistance, while addressing the lack of a high-coverage audit process for VAT returns. Integrating the income tax and social security administrations could reduce tax evasion over the medium-term.

8. Enhancing public expenditure efficiency could facilitate shifting spending toward a more growth-friendly and inclusive mix. To this end:

Public investment. The mission notes the need to increase non-energy related public investment—especially if the envelope must accommodate large-scale priority projects—but only in the context of a sustainable fiscal position and a comprehensive infrastructure plan that lays out priorities and financing options. Public investment management should be strengthened in line with the recent Public Investment Management Assessment.

Social protection spending. Efficiency gains could be achieved by rationalizing the numerous social protection programs and improving targeting, including by reducing errors of inclusion and exclusion, beneficiary overlaps, and program duplications.

Wage bill. Stricter standards and more transparency in the use of temporary personnel, along with the consistent application of merit-based recruitment and the establishment of a centralized payroll system would contain the wage bill. However, maintaining pay competitiveness will be important to ensure staff quality and mitigate corruption incentives.

Education spending. More careful audits of payrolls to identify ghost workers and curb absenteeism, along with a rebalancing of spending towards investment in equipment and facilities, will help increase the efficiency of education spending. Improving the quality of early-childhood education, access to education in low-coverage regions and for disadvantaged-background children would lead to better outcomes.

Pension system. The mission welcomes the reduction in management fees for pension funds and recommends further improving pension adequacy by increasing the contribution rate for the defined-contribution pension system, potentially by reducing contributions to the housing fund Infonavit to avoid incentives for firms to operate informally. Moreover, consideration could be given to increasing the effective retirement age. Finally, federal and local non-contributory pension pillars should be consolidated.

Health sector . The mission recommends seeking efficiency gains in health expenditure by reducing administrative and insurance costs. Investment should target rural and impoverished areas with deficient access to services. Improving the portability of insurance and building an information infrastructure compatible across sub-systems would improve continuity of care, health outcomes, and reduce beneficiary duplication.

Public procurement . Making further progress on centralizing procurement and adopting a digital platform could yield savings, while reducing the risks of corruption and bid rigging.

9. The mission recommends reconsidering Pemex's business plan with the aim of improving profitability, while also providing relief to the budget. The company's financial situation remains weak, its debt is elevated, and oil production had been dropping until very recently. The business plan limits cooperation with private firms in Pemex's upstream business to service contracts, envisages investing heavily in its loss-making downstream business, and lacks concrete ways to reduce operating costs. The mission recommends reconsidering these decisions as they place the onus of stabilizing Pemex squarely on the government. Most importantly, joint ventures with the private sector remain the most promising way to replace reserves and increase production given fiscal pressures.

10. Strengthening the fiscal framework would support the new administration's commitment to fiscal responsibility . As the mission has emphasized in the past: (i) the current fiscal framework could benefit from a well-calibrated debt anchor ; (ii) the structural spending rule should cover a broader expenditure envelope; (iii) the framework lacks a well-defined adjustment path to return to target after a shock; (iv) triggers for the use of escape clause should be significantly tightened ; and (iv) a non-partisan, adequately-sourced fiscal council should be created with a formal mandate to provide an independent evaluation of fiscal policy. It is encouraging that the new administration shares these views and intends to revamp the fiscal framework along these lines. The mission stands ready to provide support in these efforts, and also recommends putting in place a modern medium-term budget framework and implementing the recommendations of the 2018 Fiscal Transparency Evaluation.

Monetary policy

11. The mission welcomes the recent easing of monetary policy and sees scope to continue easing in the period ahead. Banxico's tight monetary stance was successful in bringing headline inflation back to the 3-percent target. Going forward, given the still-tight policy stance in the context of a large negative output gap, the mission recommends continuing to lower the policy rate so long as inflation remains close to the target and inflation expectations remain anchored, while being mindful of risks.

12. Improvements in the communication strategy have helped guide market expectations. The mission welcomes these improvements and urges Banxico to continue keeping its communication concise, while focusing on external developments only to the extent that these are relevant for the inflation trajectory.

13. Exchange rate flexibility should remain the key shock absorber. The flexible exchange rate has played an important role in gradually strengthening the non-oil balance as Mexico shifted from being a net oil exporter to net oil importer. Exchange rate flexibility will be indispensable to restore equilibrium in response to permanent shocks, while foreign exchange intervention should be limited to incidences of disorderly market conditions. The FCL provides an additional buffer, should downside risks materialize.

Financial stability

14. Financial sector resilience could be further boosted by closing gaps in the regulatory and supervisory framework. In line with the 2016 FSAP recommendations, the mission advocates: (i) increased operational independence, budget autonomy, and legal protection of the banking and securities supervisor; (ii) integration of prudential supervision functions under one authority for all financial institutions; (iii) enhancements to the definition of "common risk" and "related party"; and (iv) expansion of the resolution regime to cover financial holding companies and strengthening the authorities' powers to require banks to make changes to improve their resolvability.

15. Efforts to boost financial sector competition and inclusion should continue . The mission welcomes the authorities' efforts to improve financial inclusion through a diverse set of measures announced earlier in the year. Going forward, a multi-pronged strategic approach to boost lending and strengthen competition and inclusion should be a policy priority amid weakening economic activity. Specifically, priority should be given to initiatives that boost competition and transparency in financial products, reduce cash usage and improve financial infrastructure especially in terms of supporting SMEs. Finally, upcoming fintech secondary regulations should promote competition in the sector while preserving financial stability.

Structural reforms

16. There is a need to raise potential growth by reinvigorating the structural reform agenda. Despite important transformations of the Mexican economy, growth has continued to disappoint, and the medium-term outlook has weakened. Poverty and inequality have only modestly declined and have failed to do so in Mexico's South. Reinvigorating productivity-enhancing reforms is thus central to boosting growth, reducing poverty and inequality, and narrowing regional income disparities. Specifically:

Combating corruption and money laundering. The mission re-iterates the importance of more effective enforcement and inter-agency cooperation to counter corruption, and the need for the effective implementation of the 2014 National Anti-Corruption Strategy. With respect to anti-money laundering, the mission notes UIF's drive to increase the effectiveness of financial investigations. FGR should take the necessary measures to be able to effectively follow-up on UIF's referrals. The current lack of transparency of beneficial ownership of companies enables corruption, money laundering, tax evasion and other financial crime, and should urgently be addressed through an inter-agency task force. The mission expresses concern about reduced budget allocations to sector regulators and important autonomous entities such as the judicial branch, COFECE and CONEVAL.

Reducing Mexico's labor informality. The mission recommends strengthening enforcement and reinvigorating efforts to replace hiring and firing restrictions with an unemployment insurance scheme; and reducing entry costs for formal firms, e.g., by reducing the procedural costs and time burdens of starting and formalizing a business.

Improving the security situation. Enhancing the effectiveness of law enforcement and judicial institutions is critical to strengthening the rule of law.

17. There is also a need to continue addressing gender gaps. Lowering participation barriers for mothers remains a priority as gender gaps increase during child-bearing years, and women with more children participate less. Child care and maternity/paternity benefits are well below OECD peers and should be expanded. In addition, the mission is concerned over the cancelation of subsidies for child care facilities and their replacement with direct transfers. Promoting the financial inclusion of women should be one of the pillars of the government's upcoming financial inclusion initiatives.

18. Productivity growth would also benefit from strengthening competition and easing product market regulations. The mission advocates removing barriers to trade in services, especially in the transportation and logistics sector. It also urges restarting energy auctions and risk-sharing arrangements between Pemex and private firms.

19. Further adjustments in the minimum wage should be very gradual to avoid short-term disruptions and adverse formal employment effects. While acknowledging that increases in the minimum wage—large enough to ensure an increasing ratio of minimum-to-median wages—would help reduce inequality, the mission recommends caution in further adjustments to avoid discouraging formal employment.

-----

Earlier:

2019, February, 25, 11:50:00

PEMEX PRODUCTION DOWN TO 1.62 MBD

REUTERS - Mexico’s Pemex produced 1.62 million barrels of crude per day in January, less than any month in almost three decades, the state-owned oil company said on Friday, underscoring the challenges facing a government that vows to pump far more in a few years.

|

2018, November, 30, 11:20:00

MEXICO'S GAS DOWN

U.S. EIA - Dry natural gas production in Mexico has fallen 38% since 2012 because of declining reserves, a low price environment, and limited exploration and production of new wells. Mexico’s dry natural gas production was 2.4 billion cubic feet per day (Bcf/d) in October 2018, according to Petróleos Mexicanos (PEMEX). This level is down 7% from year-ago levels, when production averaged 2.5 Bcf/d, and down 21% from two years ago, when production averaged 3.0 Bcf/d.

|

2018, November, 11, 07:49:00

MEXICO'S GROWTH 2.1 - 2.3%

IMF - Mexico's growth is expected to accelerate modestly in the near term, reaching 2.1 percent in 2018 and 2.3 percent in 2019. Private consumption remains the main driver of activity, supported by manufacturing exports. Private investment strengthened somewhat in recent quarters but continues to be held back by uncertainty, including, until recently, about Mexico’s future trade relationship with the United States.

|