2019-12-13 10:00:00

AUSTRALIA'S ECONOMY GROWTH 2.2%

IMF - December 13, 2019 - AUSTRALIA: Staff Concluding Statement of the 2019 Article IV Consultation Mission

- Economic growth should continue to recover gradually toward its medium-term potential, with inflation remaining below the target range in the near term. Risks to the outlook are tilted to the downside amid subdued domestic confidence, heightened global policy uncertainty and the risk of a faster slowdown in China.

- In this context, macroeconomic policies should remain accommodative, and the expected reduction in state-level infrastructure spending in FY2020/21 should be reconsidered. If downside risks materialize, stronger fiscal and monetary stimulus would be warranted. Macroprudential policy should stand ready to tighten in case of increasing risks to financial stability.

- Continued efforts are warranted to foster strong, inclusive, and sustainable growth. Priorities for structural reforms include supporting business investment, strengthening innovation capacity, making the tax system more efficient, and pursuing policies to limit greenhouse gas emissions.

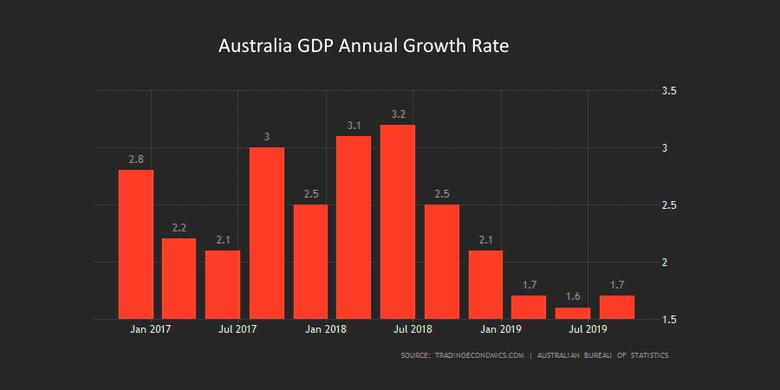

Economic growth has gradually improved from the lows in the second half of 2018 but has remained below potential. Growth has been supported by public spending, including on infrastructure, and net exports, which have held up well despite headwinds from global policy uncertainty and China’s economic slowdown. However, domestic private demand has remained weak amid subdued confidence, with a widening output gap. In addition, the ongoing drought has been a drag on economic growth. Wage growth has remained sluggish, reflecting persistent labor market slack, and inflation and measures of inflation expectations have dropped to below Australia’s 2 to 3 percent target range. Following a marked adjustment over the past two years, housing prices have started to recover, particularly in Sydney and Melbourne.

Growth should continue to recover at a gradual pace. Following growth of about 1.8 percent in 2019, the economy is expected to expand by 2.2 percent in 2020. Private domestic demand is expected to recover slowly, supported by monetary policy easing and the personal income tax cuts. An incipient recovery in mining investment is also expected to contribute to growth. In addition, the house price recovery will likely reduce the drag on consumption from earlier, negative wealth effects. That said, residential and non-mining business investment are expected to take longer to recover. Over the medium term, growth is expected to reach the mission’s estimate of potential growth of about 2½ percent, supported by infrastructure spending and structural reforms. With continued labor market slack, underlying inflation will likely stay below the target range until 2021.

Risks to the outlook remain tilted to the downside.

· On the external side, Australia is especially exposed to a deeper-than-expected downturn in China through exports of commodities and services. A renewed escalation of U.S.-China trade tensions could further impair global business sentiment, discouraging investment in Australia. A sharp tightening of global financial conditions could squeeze Australian banks’ wholesale funding and raise borrowing costs in the economy.

· On the domestic side, private consumption could be weaker should a cooling in labor markets squeeze household income. Adverse weather conditions, including a more-severe-than-expected drought, could further disrupt agriculture, dampening growth. On the upside, looser financial conditions could re-accelerate asset price inflation, boosting private consumption but also adding to medium-term vulnerabilities given high household debt levels.

With below-potential growth, weakening inflation expectations, and continued downside risks, the macroeconomic policy mix should remain accommodative.

· Monetary policy has been appropriately accommodative, and continued data-dependent easing will be helpful to support employment growth, inflation and inflation expectations.

· The consolidated fiscal stance is appropriately expansionary for FY2019/20. Fiscal policy will be supportive for demand via reductions in personal income and small business corporate taxes, additional infrastructure spending, and the government’s announced support measures for small- and medium-sized enterprises (SMEs). However, fiscal policy aggregated across all levels of government will be contractionary in FY2020/21, as state-level infrastructure investment is expected to decline. States should reconsider this and attempt to at least maintain their current level of infrastructure spending as a share of GDP to continue addressing infrastructure gaps and supporting aggregate demand.

The authorities should be ready for a coordinated response if downside risks materialize. Australia has substantial fiscal space it can use if needed. In addition to letting automatic stabilizers operate, Commonwealth and state governments should be prepared to enact temporary measures such as buttressing infrastructure spending, including maintenance, and introducing tax breaks for SMEs, bonuses for retraining and education, or cash transfers to households. In case stimulus is necessary, the implementation of budget repair should be delayed, as permitted under the Commonwealth government’s medium-term fiscal strategy. In addition, unconventional monetary policy measures such as quantitative easing may become necessary in such a scenario as the cash rate is already close to the effective lower bound.

The macroprudential policy stance remains appropriate but should stand ready to tighten in case of increasing financial risks. Australian banks remain adequately capitalized and profitable, but vulnerable to high exposure to residential mortgage lending and dependent on wholesale funding. While the risk structure of mortgage loans has been significantly improved, renewed overheating of housing markets and a fast pick-up in mortgage lending remain risks in a low-interest-rate environment. The Australian Prudential Regulation Authority (APRA) should continue to expand and improve the readiness of the macroprudential toolkit. This should include preparations, for potential use in the event of a rapid housing credit upswing, for introducing loan-to-value and debt-to-income limits, and possibly a sectoral countercyclical capital buffer targeting housing exposures.

Strong reform efforts to bolster the resilience of the financial sector should continue. The mission supports the authorities’ plan to further enhance banks’ capital framework, including strengthening their loss-absorbing capacity and resilience. In addition, encouraging banks to further lengthen the maturity structure of their wholesale funding would help mitigate ongoing structural liquidity risks. The authorities’ commitment to implement the recommendations made by the Hayne Royal Commission by end-2020 is welcome. The improvement in lending standards further enhances financial sector resilience, and reducing the uncertainty in the enforcement of responsible lending obligations would prevent excessive risk aversion in the provision of credit. The authorities should implement the APRA Capability Review’s recommendations to strengthen APRA’s resources and operational flexibility, enhance its supervisory approach in assessing banks’ governance and risk culture, and strengthen enforcement efforts. In addition, reinforcing financial crisis management arrangements and strengthening the AML/CFT regime should remain priorities, in line with the findings of the 2018 Financial Sector Assessment Program (FSAP).

Housing supply reforms remain critical for restoring affordability. More efficient long-term planning, zoning, and local government reform that promote housing supply growth, along with a particular focus on infrastructure development, including through “City Deals”, should help meet growing demand for housing.

Efforts to boost private investment and innovation should be stepped up. Non-mining business investment, including R&D, has been sluggish, contributing to lower productivity growth. Reducing domestic policy uncertainty, supporting SMEs’ access to finance, and accelerating structural reforms would help to improve the investment environment. Building on reforms in the 2015 Harper Review, Australia can further improve product market regulations, including by simplifying business processes through the work of the Deregulation Taskforce. The ongoing policy priority on skills and education reforms is welcome to improve the environment for innovation, and consideration should be given to faster implementation of the recommended measures in the Australia 2030: Prosperity through Innovation report. Government initiatives to relieve SME financing constraints are welcome, including the Australian Business Securitization Fund and the Australian Business Growth Fund. Incentives for banks to lend more to businesses, including through reducing the concentration in mortgages, can help support business investment, as can the promotion of venture capital. Supporting new investment through tax measures, possibly including targeted investment allowances, as well as further improving the effectiveness of government R&D support for younger firms, would also be helpful.

Australia’s continued efforts supporting international cooperation are welcome. The mission welcomes the authorities’ support to enhance the effectiveness of the WTO and pursuit of the Regional Comprehensive Economic Partnership (RCEP), which aims to liberalize trade and improve quality and environmental standards and labor mobility throughout the Asia and Pacific region. Developing a national, integrated approach to energy policy and climate change mitigation, and clarifying how existing and new instruments can be employed to meet the Paris Agreement goals, would help reduce policy uncertainty and catalyze environmentally-friendly investment in the power sector and the broader economy.

Further reforms can help to promote female labor market participation and reduce youth underemployment. There is scope to increase full-time employment for Australian women and addressing persistently high underemployment particularly among youth. The 2018 Child Care Subsidy program and the forthcoming Mid-Career Checkpoint program are expected to support women in work. This could lay the foundation for a broader review of the combination of taxes, transfers, and childcare support to reduce disincentives for female labor force participation. Pursuing ongoing reforms in vocational training can help reduce youth underemployment.

Broad fiscal reforms would help promote efficiency and inclusiveness. Australia should continue to reduce distortions in its tax system to promote economic efficiency and in doing so should be mindful of distributional consequences considering income inequality. Recent reforms in personal and corporate income taxes have helped to improve the efficiency of the tax system. A further shift from direct to indirect taxes could be made by broadening the goods and services tax (GST) base and reducing the statutory corporate income tax rate for large firms. The impact of these reforms could be made less regressive for households through targeted cash transfers. Transitioning from a housing transfer stamp duty to a general land tax would improve efficiency by easing entry into the housing market and promoting labor mobility, while providing a more stable revenue source for the States. Such reforms could be complemented by reducing structural incentives for leveraged investment by households, including in residential real estate.

The mission would like to thank the authorities and counterparts in the private sector, think tanks, and other organizations for frank and engaging discussions.

-----

Earlier:

2019, December, 6, 13:20:00

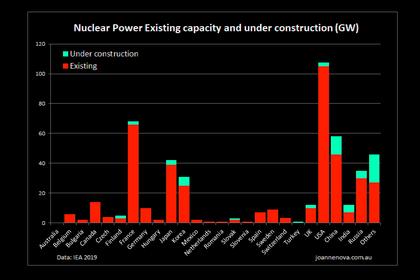

NUCLEAR POWER FOR AUSTRALIA

The use of nuclear energy is currently banned under federal law in Australia. Over half those surveyed - 54% - were unaware of this.