2019-03-20 10:55:00

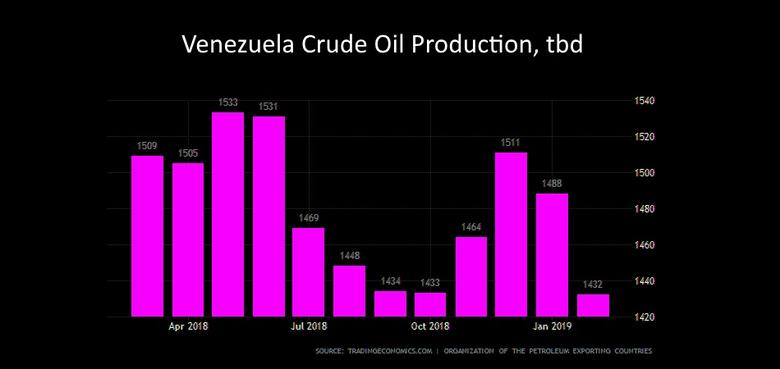

VENEZUELA'S OIL PRODUCTION 1.2 MBD

IEA - The electricity crisis in Venezuela has paralysed most of the country for significant periods of time. Although there are signs that the situation is improving, the degradation of the power system is such that we cannot be sure if the fixes are durable. Until recently, Venezuela's oil production had stabilised at around 1.2 mb/d. During the past week, industry operations were seriously disrupted and ongoing losses on a significant scale could present a challenge to the market. As it happens, 1.2 mb/d is also the size of the output cuts agreed by OPEC countries and some non-OPEC producers. The cuts were implemented in January and compliance by OPEC reached 94% in February, with Saudi Arabia cutting back by about 170 kb/d more than required. The non-OPEC countries are complying more slowly at a rate of 51%, with Russia reducing its output very gradually. Due to the cuts, OPEC members are sitting on about 2.8 mb/d of effective spare production capacity (Iran and Venezuela are excluded from the calculation), with Saudi Arabia holding two-thirds of it. Much of this spare capacity is composed of crude oil similar in quality to Venezuela's exports. Therefore, in the event of a major loss of supply from Venezuela, the potential means of avoiding serious disruption to the oil market is theoretically at hand.

Before the seriousness of the situation in Venezuela became apparent, our oil balances for the first half of 2019, which have not changed significantly since our last Report, suggested that the market is tightening. On the basis of solid oil demand growth, modest declines in OPEC production due to Iran and Venezuela, and rising US output, the market could show a modest surplus in 1Q19, before flipping into deficit in 2Q19 by about 0.5 mb/d. This does not take into account Saudi Arabia's announced plans to reduce its exports further in April.

Although we must await developments in Venezuela, if there were to be a collapse in production, it could provide an opportunity for other producers who can supply comparable barrels. Venezuela currently ships about 400 kb/d to both China and India. Elsewhere, other producers have already taken advantage of Venezuela's problems: as exports to the US have slumped following the imposition of sanctions, Russia has taken the opportunity to increase its shipments to the US from relatively modest levels to around 150 kb/d.

Geopolitics has added another complication to the global oil market. At the same time, production cuts have increased the spare capacity cushion. This is especially important now as economic sentiment is becoming more pessimistic and the global economy could be entering a vulnerable period.

A key theme is the growing importance of the US in global markets. Rising production there is not a new story; what is game changing is that the US in 2021 will become a net oil exporter on an annual average basis. With Canadian production also increasing, and most of its exports moving to US refineries, this frees up US crude for export. This year US seaborne oil trade will move into surplus with net exports rising to nearly 4 mb/d of by 2024. The rising profile of the US not only brings greater choice to consumers, but, crucially, it enhances security of supply, especially when, as now, there are heightened geopolitical concerns.

-----