2019-06-25 12:50:00

U.S. FINANCIAL RISKS UP

IMF - On June 21, 2019, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with the United States.

The U.S. economy is in the longest expansion in recorded history. Unemployment is at levels not seen since the late 1960s, and economic activity is growing above potential, aided by a fiscal stimulus and supportive financial conditions. Real wages are rising, including for those at the lower end of the income distribution, and productivity growth appears to be recovering. Against this backdrop, inflationary pressures remain remarkably subdued.

Despite these positive macroeconomic outcomes, the benefits from this decade-long expansion have not been shared as widely as they could. Average life expectancy is falling, income and wealth polarization have increased, poverty has fallen but remains higher than in other advanced economies, and social mobility has steadily eroded.

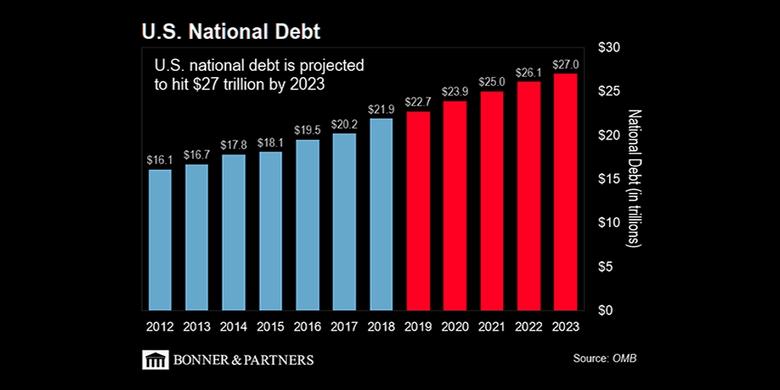

In addition, a number of medium-term risks are growing. The financial system appears healthy but vulnerabilities in leveraged corporates and, potentially, in the nonbank system are elevated by historical standards. An abrupt reversal of the recent supportive financial market conditions or a deepening of ongoing trade disputes represent material risks to the U.S. economy, with concomitant negative outward spillovers. The U.S. public debt-to-GDP ratio is on an unsustainable path and is expected to continue rising throughout the medium-term, as aging related spending rises.

The consultation focused on the policies needed to address these risks, preserve financial stability, support the standard of living for low- and middle-income households, and rebuild fiscal space.

Executive Directors welcomed the continued robust performance of the U.S. economy, which is about to mark its longest expansion in recorded history. They noted the achievements of low unemployment, rising real wages, and subdued inflation. Economic prospects remain favorable and risks were viewed to be broadly balanced. Nevertheless, Directors observed that public debt is on an unsustainable path, trade tensions and uncertainties are continuing, and medium-term risks to financial stability are rising. Continued vigilance, prudent macroeconomic policies, and supply-side reforms would be critical to securing strong, balanced, and inclusive growth, generating positive spillovers to the rest of the world.

Directors called on the authorities to address external imbalances through fiscal adjustment and supply-side reforms that enhance productivity and competitiveness. They encouraged the United States to work constructively and cooperatively with its trading partners to address distortions in the trading system and resolve trade tensions in a manner that promotes a more open, stable, and transparent rules-based international trade system.

Directors underscored the need to ensure that the benefits of the strong economy are broadly shared. They considered it a priority to address rising income inequality and improve social outcomes. To this end, they encouraged initiatives to reform the educational system, healthcare, and social programs. Specifically, Directors recommended expanding the Earned Income Tax Credit, providing family-friendly benefits, and improving healthcare coverage while tempering costs.

Directors stressed that policy adjustments are necessary to lower the fiscal deficit and put public debt on a gradual downward path over the medium term. They recommended that the authorities consider possible options to better control entitlement spending and raise indirect taxes. They considered that these efforts would create fiscal space to expand needed investments in infrastructure and human capital. They also saw scope for further improving the budgetary process.

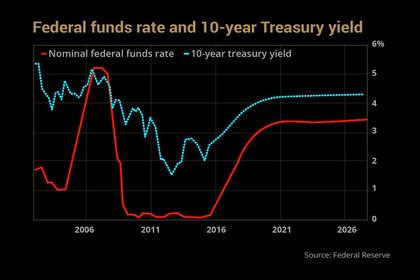

Directors welcomed the Federal Reserve’s pause in interest rate adjustments. They agreed that any further increases in the federal funds rate should be deferred until there are clearer signs of wage or price inflation. In this regard, they appreciated the authorities’ continued adherence to a data-dependent approach and clear, forward-looking communication. Directors also welcomed the authorities’ readiness to consider refinements to the monetary policy framework following the Federal Reserve’s review of its monetary policy strategy, tools, and communication.

Directors observed that the financial system appears healthy, with well-capitalized banks. However, risks are building up among leveraged corporations and, possibly, in the nonbank sector. An abrupt reversal of supportive financial market conditions could weigh on real activity and job creation, with negative outward spillovers. Directors emphasized the importance of enhancing the risk-based approach to regulation and supervision, strengthening the oversight of nonbanks, and addressing remaining data gaps.

Directors welcomed the authorities’ voluntary participation in the Fund’s enhanced governance framework on the supply and facilitation of corruption. They encouraged continued efforts to improve entity transparency and beneficial ownership information.

|

United States: Selected Economic Indicators (Percentage change from previous period, unless otherwise indicated) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

-----

Earlier:

2019, June, 21, 09:35:00

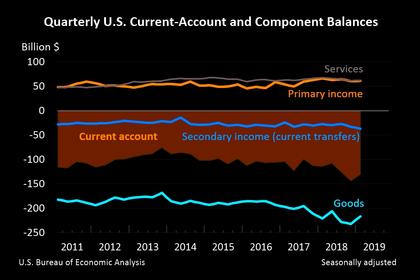

U.S. CURRENT-ACCOUNT DEFICIT DOWN TO $130.4 BLN

The U.S. current-account deficit decreased to $130.4 billion (preliminary) in the first quarter of 2019 from $143.9 billion (revised) in the fourth quarter of 2018, according to statistics released by the Bureau of Economic Analysis (BEA). The deficit was 2.5 percent of current-dollar gross domestic product in the first quarter, down from 2.8 percent in the fourth quarter.

2019, June, 20, 17:15:00

U.S. FEDERAL FUNDS RATE 2.25 - 2.5%

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent.

2019, June, 18, 17:15:00

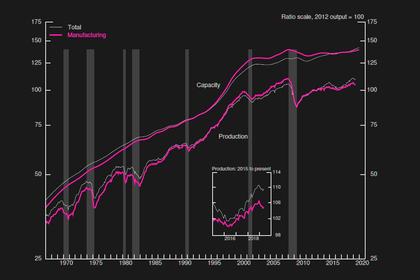

U.S. INDUSTRIAL PRODUCTION UP 0.4%

Industrial production rose 0.4 percent in May after falling 0.4 percent in April. The indexes for manufacturing and mining gained 0.2 percent and 0.1 percent, respectively, in May; the index for utilities climbed 2.1 percent. At 109.6 percent of its 2012 average, total industrial production was 2.0 percent higher in May than it was a year earlier. Capacity utilization for the industrial sector moved up 0.2 percentage point in May to 78.1 percent, a rate that is 1.7 percentage points below its long-run (1972–2018) average.