2019-06-13 16:10:00

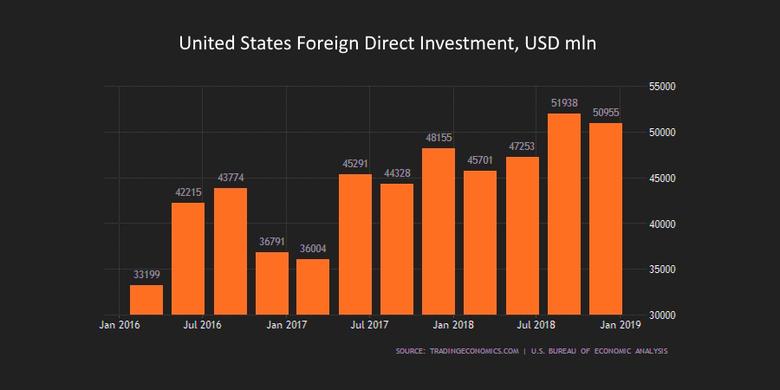

U.S.: THE PLACE FOR INVESTMENT

U.S. DT - Keynote Address by Deputy Secretary Justin Muzinich to the German-American Conference in Berlin: Strengthening Transatlantic Resilience in Turbulent Times

INTRODUCTION: IMPORTANCE OF THE TRANSATLANTIC RELATIONSHIP

Thank you Steve for the introduction, and thanks to the American Council on Germany and Atlantik-Brücke for inviting me today. I see a number of friends in the audience, and it is a real pleasure to be here with you.

I have come directly from the G-20 meetings in Japan because of my belief in the importance of today's topic: Strengthening Transatlantic Resilience in Turbulent Times. Together, the U.S. and Europe account for roughly a third of world GDP and half of global personal consumption. This partnership is vital to my country's economic future, and to Europe's.

However, the close alliance and friendship we have with Germany, and with all of Europe, is about much more than economics. It is a community of values that we cherish, and live by, and are prepared to defend. Our shared belief in liberty and democracy makes this partnership a cornerstone of world stability.

Few moments in time have symbolized these shared values more than the fall of the Berlin Wall, an event we mark the 30th Anniversary of this year. At a decisive point in the Cold War, President Reagan stood at the Brandenburg Gate and declared, prophetically, that "the wall cannot withstand freedom." Germany was divided for a time – Europe was divided for a time – but in the end, no ideology could overcome what President Reagan called "the moral courage of free men and women." Time and events have proven the power of our ideals to bring forth material progress and human flourishing in our countries. And yet we know that our values are unfortunately not shared by all regimes. That is why we must keep this vital partnership strong. Today I would like to discuss a few common opportunities and challenges we face, where cooperation can make all the difference.

INTERNATIONAL TAXATION

First is the international tax system. Historically, this system relied on the basic concept of physical presence, meaning a country can tax a firm physically located within its borders. Today, more and more of a typical firm's assets have shifted from hard assets, such as physical plants, to intangibles like intellectual property and brand value. By one estimate, intangible asset values of S&P companies increased from 17 percent in 1975 to 84 percent in 2015. Intangible assets are, of course, the easiest to move around, and over time they have been shifted to low-tax countries. In many cases, this divides a firm between one country where it has factories or customers, and another where the intangible assets sit and profits accumulate. So taxes are not always collected where commerce occurs.

This is a problem common to us all, and it begs for a common solution. Some governments have already taken unilateral action in the form of digital taxes. This is the wrong approach because the issue is much broader than the digital economy – the problem is intangible assets generally. But it is also the wrong choice in a more profound sense. We have for decades had stable and mutually agreed principles for international taxation. New and untested unilateral measures put that at risk. At the very least, they will create confusion. They also bring the threat of double taxation of multinational businesses, which would be a real hindrance to expansion, job creation, and growth generally. The United States is actively engaging at the OECD to settle on a long-term, multilateral solution. We have a proposal on the table, and we're open to discussion and suggestions for how to implement it. Germany has been especially helpful on this issue, and we believe that with continued close cooperation, we can move other countries in the right direction.

INVESTMENT SECURITY

A second area where cooperation will be vital is investment security. This is an increasingly important topic, as cutting edge technology acquisition has become a means for nation-state military and economic advancement. Frontier technologies such as 5-G, AI, and quantum computing hold tremendous promise, but we know that they can also be applied to less benign purposes, threatening liberty rather than enhancing it.

The United States regards inward investment as important for technological advancement and growth, but only when entirely consistent with national security. Through the Committee on Foreign Investment in the United States—also known as CFIUS—we have a robust process for reviewing foreign investment for national security risks. In fact, Congress expanded our authority to review transactions in a bipartisan bill last year.

This new law also strengthened our ability to coordinate with like-minded partners. Right now, through the G7 and the OECD, we are working closely with the German government, and we welcome Germany's recent expansion of investment security to key industries including defense, critical infrastructure, and the media.

The United States also strongly supports the European Union's recently passed regulation for investment screening. As the EU implements this framework, we stand ready to share from our 30 plus years of experience in this area. It is still early enough for all of us to ensure that technology is harnessed to make our lives better, rather than being used to make us more vulnerable.

COUNTERING ILLICIT FINANCE

The next area that is ripe for greater cooperation is the ongoing duty to counteract money laundering and terrorist financing. The U.S. and Europe have been very effective along these lines. Our joint efforts have made it more difficult for terrorists and criminals to misuse the international financial system. For example, through the work of the Financial Action Task Force, FATF, virtually all countries are subject to a rigorous peer review that examines their ability to prevent money laundering and terrorist financing.

We appreciate the European Council's rejection of the European Commission's recently proposed list of jurisdictions that pose a high risk of money laundering. Approving this new list would have undermined FATF, and confused financial institutions. The unanimous decision of EU member states opposing this list allows us to focus on the serious illicit finance challenges that require U.S. -EU coordination. Among these are the need to ensure that cryptocurrency is not used for malign ends... and the task of preventing corrupt money flows in Venezuela, where Maduro and his inner circle have enriched themselves by stealing the assets of the Venezuelan people. Maduro is driving his country further and further into economic and humanitarian collapse. We were pleased to see Germany and the majority of other European nations recognize interim President Juan Guaido's government. And when there is a transition of power in that country, the United States will work with our European partners to support the revival of democracy and prosperity in Venezuela.

FINANCIAL REGULATORY APPROACH

Cooperation will yield good outcomes in a fourth area, international financial supervision. Modern markets and institutions have global reach, so effective regulation requires strong dialogue to keep us moving in a direction that serves the interests of us all.

Here the trend in Europe is pretty clear –centralization of what was previously a more fragmented approach. This development is pro-growth, and it serves the broader goals of the European project. However, a shift to pan-European supervision also presents challenges for U.S. institutions, particularly in capital markets. A regulatory shift can lead to uncertainty over key questions, such as who is the supervisor and what are the rules.

At Treasury, we have tried to do our share of listening on financial regulatory policy. In writing regulations under our recent tax reform, we listened to concerns from a broad range of taxpayers, including European financial institutions. In December, we provided substantial relief for foreign-parented financial groups, including an exception for payments to foreign branches in the United States.

We hope the spirit of listening and cooperation can continue on both sides. Along these lines, we suggest continuing to interpret regulatory "equivalence" in its original sense: that a different regulatory framework can nevertheless deliver equivalent outcomes for supervision. In other words, where appropriate, U.S. regulators should defer to Europe when it comes to regulating European financial institutions; and European regulators should defer to the U.S. when it comes to regulating U.S. financial institutions. All the various national regulatory regimes will never be fully harmonized or identical. So if the goal is to have truly global markets, it's critical that we hold onto the concept of equivalence.

ECONOMIC GROWTH

The four areas of cooperation I've just discussed are, of course, related to a broader shared challenge, which is to achieve vigorous, sustained economic growth across the nations of this partnership. Let me take a few moments to describe our Administration's approach.

With faster growth as a prime objective, the United States in December 2017 enacted the first major re-write of our tax code in more than three decades.

We designed the new tax system to deliver relief to middle-income households by lowering tax rates and providing various credits to reduce the overall burden. However, we wanted more than a lower tax burden. We also wanted higher pre-tax wages. Rising wages are critical to achieving good distributional outcomes, since for many Americans wages, rather than earnings from asset ownership, are the main source of income. Over the preceding decade, even as the asset markets recovered, wages didn't go up much. A key reason was that productivity growth had slowed – and productivity growth had slowed because capital investment had slowed. Between 2008 and 2016, net investment in real capital stock decreased to 1.1 percent annual growth from a post-World War Two average of 3.2 percent.

In response, we adopted a number of policies to make the United States a more attractive place to invest, including these:

Reducing the corporate tax rate from 35 percent to 21 percent, and cutting rates for small businesses.

Moving the United States from a worldwide system of taxation to a territorial system.

And allowing for immediate expensing of capital equipment.

While the law is still relatively recent, the early evidence is positive.

Private nonresidential investment grew at 6.9 percent in 2018, more than double the average rate from 2009 to 2016;

Greater investment helped GDP expand by 3 percent from the fourth quarter of 2017 to the fourth quarter of 2018, the fastest Q4 to Q4 pace since 2005; and it expanded 3.1 percent in the first quarter of the year;

Increased investment also helped wages grow by more than 3 percent in the last year, the fastest in a decade;

And the unemployment rate is 3.6 percent, the lowest since 1969. Notably, unemployment rates for women, African Americans, and Hispanics are at or near their lowest ever.

It's an encouraging picture – and of course the real story is the creative genius of the free enterprise system. Government doesn't create prosperity – but it can create the conditions that enable it. We recommend our policies to other countries. And in Germany in particular we see an opportunity to encourage domestic investment, consumption and growth. Together we can build a foundation for global prosperity.

TRADE

Another area of policy that is important to both our countries is trade. I'd like to briefly touch on that, along with Iran, before wrapping up

We are increasing our cooperation on issues of mutual concern with the European Union and Japan in a trilateral process, particularly as it relates to China. By now it's clear to almost everyone that China's policies of forced technology transfer, market-distorting subsidies, tariffs, and non-tariff barriers are highly unfair and damaging. Past attempts to have these practices reversed have failed. The U.S. is now seeking changes that are meaningful and enduring. At one point we were close to a deal, but unfortunately the Chinese negotiators walked back previous commitments. Our efforts have widespread bipartisan support in the United States because they are seen as both fair and in the national interest. It's equally clear, I think, that a significant change in China's practices will also yield benefits to Germany and the EU. It is my hope that these benefits, along with our shared sense of fairness and good practice, will lead to broad EU and German support for what we're trying to achieve.

IRAN

A word now about Iran. There are obviously a variety of views on the Iran Deal itself, but since the signing of the JCPOA, Iran has continued its malign activity by testing ballistic missiles, promoting regional instability and supporting terrorism.

We can continue to work together to counter Iran's ballistic missile program. We can also target the regime's illicit financial networks in order to disrupt its funding for terrorism. To this end, we would encourage Germany to follow the UK's recent move to designate Lebanese Hizballah as a terrorist organization. We share the same ultimate vision – a peaceful Middle East, free of terrorism and nuclear proliferation.

CONCLUSION

In that spirit, let me conclude by thanking all of you for the work you have done on behalf of the transatlantic partnership, as well as for the friendship between the United States and Germany. We are very committed to maintaining the strength of this relationship. We have established the U.S. -- German Structured Economic Dialogue, and hosted a German delegation three weeks ago. At Treasury we have a valuable exchange with the German Finance Ministry. Secretary Mnuchin has a good dialogue with Minister Scholz, and this is my second trip to Germany in the last two months.

It doesn't take great historic events, or anniversaries, to remind us that the partnership between the United States and Germany is genuine and enduring, and the same is true of our partnership with Europe. Thirty years ago Willy Brandt famously said, "Now what belongs together will grow together." He was speaking of a reunified Germany, but the sentiment also applies to the transatlantic relationship. At times our opinions on policies will differ, but on the scale of world affairs, these differences are small compared to the values we share.

Our determination to uphold liberty and democracy binds us together and is an extraordinary influence for good in our world. If we live up to our own responsibilities in our own time, we will extend that influence far into the future, and leave our own legacy of prosperity, security, and peace.

Thank you very much.

-----

Earlier:

2019, June, 7, 11:35:00

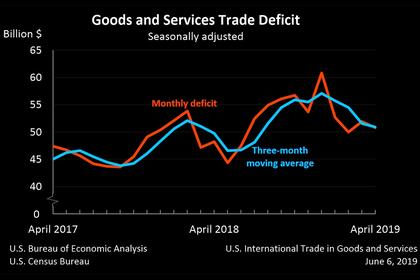

U.S. TRADE DEFICIT UPDOWN ANEW

Year-to-date, the goods and services deficit increased $4.1 billion, or 2.0 percent, from the same period in 2018. Exports increased $8.3 billion or 1.0 percent. Imports increased $12.4 billion or 1.2 percent.

2019, June, 3, 12:30:00

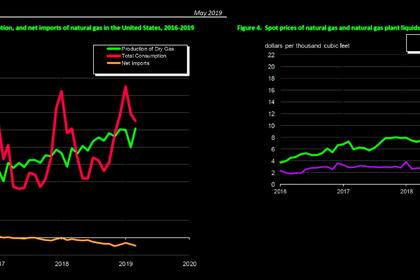

U.S. GAS PRODUCTION UP

In March 2019, for the 23rd consecutive month, dry natural gas production increased year to year for the month. The preliminary level for dry natural gas production in March 2019 was 2,771 billion cubic feet (Bcf), or 89.4 Bcf/d. This level was 9.2 Bcf/d (11.5%) higher than the March 2018 level of 80.2 Bcf/d.

2019, May, 30, 17:50:00

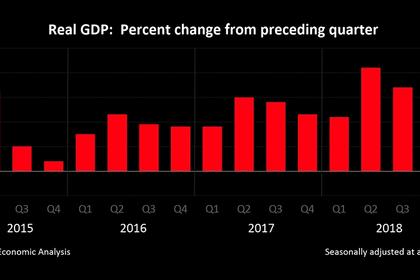

U.S. GDP UP 3.1%

U.S. real gross domestic product (GDP) increased at an annual rate of 3.1 percent in the first quarter of 2019 (table 1), according to the "second" estimate released by the Bureau of Economic Analysis. In the fourth quarter, real GDP increased 2.2 percent.