2019-07-20 11:55:00

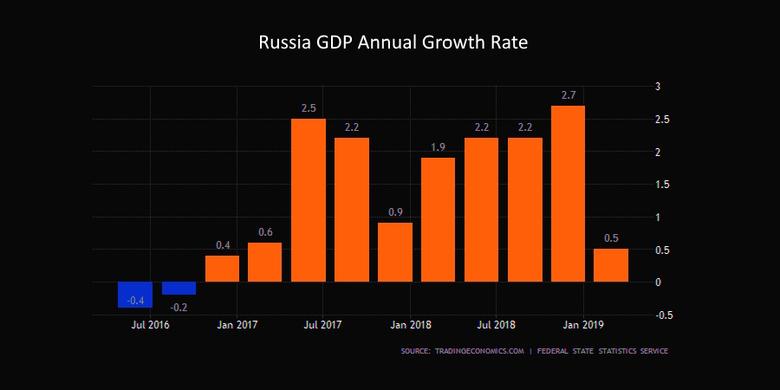

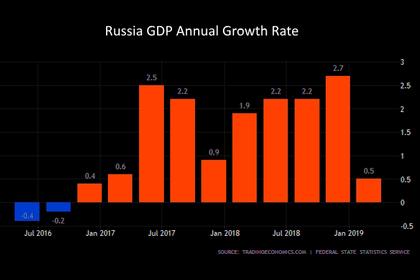

RUSSIA'S GDP UP 1.2%

IMF- On July 12, 2019, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with the Russian Federation.

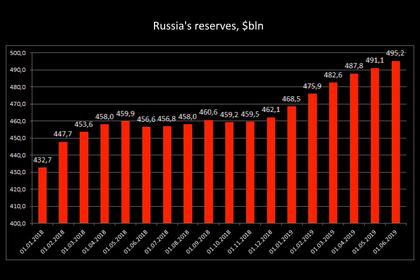

Russia’s economy continues to show moderate growth, under sound macroeconomic policies but with structural constraints and the effects of sanctions. Output grew by 2.3 percent in 2018, driven by exports and consumption, which was supported by growth in real wages and higher labor demand. Investment registered a moderate increase compared to the previous year. After reaching historical lows earlier in 2018, inflation picked up in the second half of the year. One-off factors (such as ruble depreciation as well as food and fuel price increases) rather than demand pressures were the major drivers of the increase.

Growth is projected at 1.2 percent in 2019, reflecting a weak first quarter estimate, lower oil prices and the impact of the higher VAT rate on private consumption. At the same time, GDP growth should be supported by an increase in public sector spending in the context of the national projects announced in 2018. Inflation has begun to fall and is expected to return to the 4 percent target by early 2020. The medium-term growth outlook remains modest. Public infrastructure spending under the national projects together with increase labor supply due to pension reform could have a positive effect on the growth rate of potential output. However, absent deeper structural reforms, long-run growth is projected to settle around 1.8 percent.

Executive Board Assessment

Executive Directors agreed with the thrust of the staff appraisal. Executive Directors commended the authorities for their sound macroeconomic policy framework, which helped reduce policy uncertainty, and mitigate the effects of external shocks. Directors noted that, despite the ongoing recovery, the medium-term outlook remains modest. They called for continued strong policy efforts and comprehensive structural reforms to accelerate potential growth, address institutional weaknesses and governance issues, strengthen the financial sector, and lift productivity and investment.

Directors agreed that a neutral fiscal policy stance is currently appropriate. However, they noted that additional fiscal consolidation would be needed in the long-term to ensure inter-generational equity. Directors agreed that the fiscal rule anchors fiscal policy and helps shield the economy from fluctuations in oil prices, thus facilitating economic diversification. They emphasized that further changes to the rule, especially after the slight relaxation last year, should be avoided to firmly establish its credibility. Directors encouraged the authorities to refrain from quasi-fiscal activities through the National Welfare Fund (NWF) and that they should continue to invest NWF funds into high-quality foreign assets.

Directors welcomed the authorities’ implementation of the pension reform and their plans to boost spending on health, education, and infrastructure. However, they emphasized that the spending plans should be well-targeted toward strengthening growth, and efficiently implemented. Directors noted that Russia’s fiscal revenue framework could benefit from tax base broadening and further growth-friendly shifts in taxation to incentivize labor supply, reduce labor informality, and attract new investment. They recommended that oil sector taxation should be simplified, and subsidies on domestic fuel consumption phased out. Directors noted that expenditure on social assistance needs to be better targeted to have a stronger impact on reducing poverty.

Directors supported continued easing of monetary policy, given the recent inflation outturns. They welcomed the Central Bank of Russia’s plans to maintain its careful and data-driven approach in setting monetary policy, as inflation expectations are not yet firmly anchored. Directors encouraged the CBR to further refine its monetary policy communications strategy.

Directors encouraged the authorities to continue to enhance bank supervision and regulation. This should include strengthening asset quality reviews and reducing related-party loans. They also recommended continued efforts to complete the consolidation of the banking sector. Directors welcomed the authorities’ recent macroprudential measure to curb unsecured consumer lending. However, they noted that additional measures may be needed if lending growth does not moderate. Directors underscored the importance of having a credible strategy for returning rehabilitated banks to the private sector in a way that is consistent with increasing competition among banks.

Directors underscored that ambitious structural reforms will be important to raise growth. They noted that priority should be given to creating a more vibrant private sector, and reducing the footprint of the state. However, Directors emphasized the importance of first enhancing competition by facilitating the entry and exit for firms and strengthening the institutional architecture in which firms compete. They welcomed the government’s advances in the fiscal transparency agenda and underscored that further progress is needed, including to report the government’s obligations under Public Private Partnerships, reduce the share of classified expenditure in the budget, and strengthen State Owned Enterprise governance.

------

Earlier:

2019, July, 9, 17:15:00

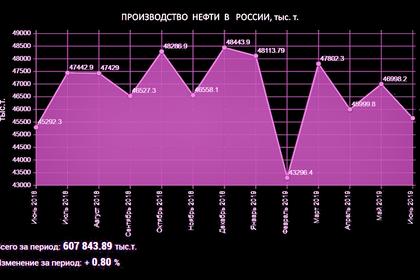

RUSSIA'S OIL PRODUCTION DOWN TO 10.79 MBD

Industry sources said Russian oil output fell to 10.79 million barrels per day (bpd) in early July, lower than the level agreed under a deal on curbing supply reached with OPEC and other producers.

2019, July, 4, 16:45:00

СТРАТЕГИЯ ОПЕК+

“Что особо важно: мы договорились постоянно мониторить ситуацию. Если появятся какие-либо угрозы для рынка, мы в любой момент можем собраться и решить, что необходимо делать. При угрозе дефицита, к примеру, мы можем вынести решение об увеличении производства”, - подчеркнул Александр Новак.

2019, July, 4, 16:40:00

БАНК РОССИИ: СНЯТЬ СТРУКТУРНЫЕ ОГРАНИЧЕНИЯ

Главные ограничения для развития, на мой взгляд, – внутренние. И поэтому в своем выступлении сегодня я хотела бы остановиться на том, какую роль в данной ситуации могли бы сыграть финансовый сектор и политика Центрального банка и что нужно с точки зрения экономической политики в целом, чтобы ситуация изменилась.

Ответ на этот вопрос известен: нужно снять структурные ограничения.

2019, July, 4, 16:30:00

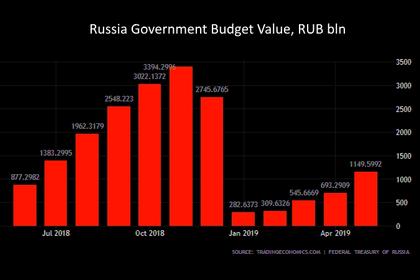

ДОХОДЫ РОССИИ +256,9 МЛРД.РУБ.

МИНФИН РОССИИ - Ожидаемый объем дополнительных нефтегазовых доходов федерального бюджета, связанный с превышением фактически сложившейся цены на нефть над базовым уровнем, прогнозируется в июле 2019 года в размере +256,9 млрд руб.

2019, July, 4, 16:25:00

ФОНД НАЦИОНАЛЬНОГО БЛАГОСОСТОЯНИЯ РОССИИ $59,7 МЛРД.

МИНФИН РОССИИ - По состоянию на 1 июля 2019 г. объем ФНБ составил 3 762 958,8 млн. рублей, что эквивалентно 59 657,9 млн. долл. США

2019, July, 3, 11:45:00

ХАРТИЯ ОПЕК+: ДОЛГОСРОЧНОЕ СОТРУДНИЧЕСТВО

“Хартия сотрудничества стран-производителей нефти должна стать фундаментом нашей будущей кооперации. Благодаря такой диалоговой платформе мы сможем не только на постоянной основе продолжить отслеживать ситуацию на нефтяных рынках, но и при необходимости оперативно реагировать на возникающие перекосы, в регулярном режиме обсуждать как на министерском, так и экспертом уровнях актуальные вопросы развития отрасли”, - подчеркнул Министр энергетики Российской Федерации и сопредседатель заседания Александр Новак.

2019, July, 2, 14:25:00

ЦЕНА URALS: $65,63

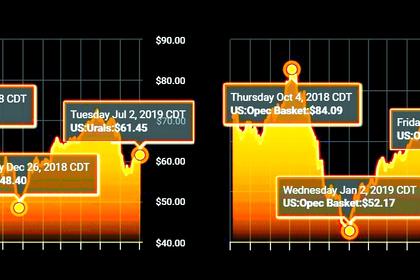

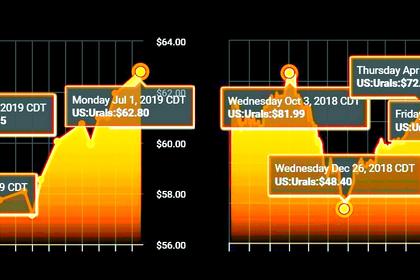

Средняя цена нефти марки Urals по итогам января – июня 2019 года составила $ 65,63 за баррель.