2020-01-31 11:15:00

KAZAKHSTAN'S GDP GROWTH 3.6%-3.8%

IMF - January 29, 2020 - On January 27, 2020, the Executive Board of the International Monetary Fund (IMF) concluded the 2019 Article IV consultation with the Republic of Kazakhstan.

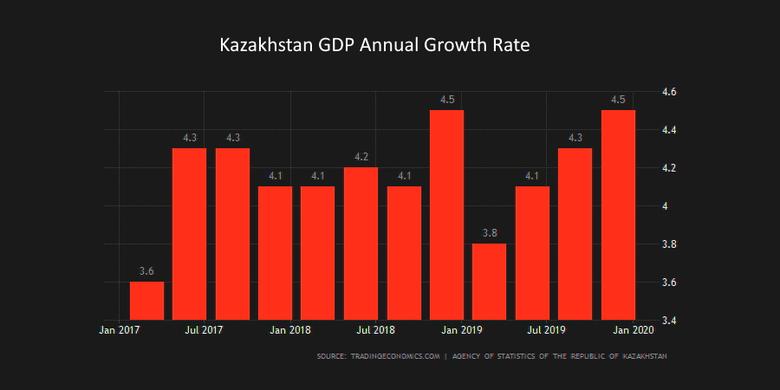

Kazakhstan’s recovery has continued, with growth in the first nine months of 2019 reaching 4.3 percent. High domestic demand driven by major oil and gas investments and government and household consumption supported by wage increases and consumer lending has underpinned the economy’s strong performance. Headline inflation picked up but has remained within the National Bank of Kazakhstan’s target band of 4–6 percent and stabilized in recent months. Lower oil prices and higher imports have weakened the external position, and the current account balance has deteriorated. The exchange rate depreciated in the second half of 2018 but has been relatively stable since then in the absence of large shocks. Over the next few years, growth is expected to slow down, largely reflecting flat oil production; non-oil growth is expected to remain robust. Risks are on the downside, reflecting trade tensions and commodity price volatility.

In response to demand pressures and inflationary risks, the NBK raised the policy rate by 25 basis points in September. Liquidity in the banking sector remains ample and credit growth is concentrated in the retail sector. Efforts have continued to clean up the banking sector, including through additional financial support from the state. Notwithstanding strong non-oil revenue performance, a looser fiscal stance is expected in 2019, due to new spending initiatives, including higher public sector wages, financial support to the vulnerable, and regional development initiatives.

Progress is being made with structural reform implementation, with many of the flagship “100 Concrete Steps” completed and the remaining ones broadly on track. The first public offering of a blue-chip public company took place in late 2018, KazAtomProm, and preparations for privatization of other large state-owned enterprises are underway. Steps have been taken to improve governance and address corruption vulnerabilities, but challenges remain.

Executive Directors agreed with the thrust of the staff appraisal. They noted Kazakhstan’s robust economic growth performance in 2019 supported by strong consumption and investment. They also welcomed the progress made in addressing long-standing financial sector issues and implementing structural reforms aimed at promoting private sector development and inclusive growth. At the same time, Directors recognized the challenges and risks the economy of Kazakhstan is facing, including from commodity price volatility.

Directors noted the pick-up of inflationary pressures in 2019 and concurred that the focus of monetary policy should remain on inflation. They noted that inflation targeting, and exchange rate flexibility have helped to absorb shocks. Directors encouraged the National Bank of Kazakhstan to continue to strengthen its monetary and exchange rate framework, including through greater independence, better coordination with the government, reducing dollarization, and improved effectiveness of monetary policy transmission. Increasing the transparency of policy and operations and further strengthening communications would boost credibility.

Directors supported the recently completed asset-quality review, which will help understand better the financial situation in the banking sector and identify corrective measures. Such measures could help lead to a strengthening of the sector. Directors underscored that any additional state support should go only to large and viable banks, subject to robust safeguards and in line with international best practices. Directors noted that Kazakhstan’s banks need to adopt a new business model with less reliance on state programs and funding and improved risk management and lending practices. Directors welcomed the formation of the new Agency for Regulation and Development of the Financial Market of the Republic of Kazakhstan. They noted that reorganization of the financial supervisory architecture could entail risks in the transition period, which should be managed carefully. Independence and adequate resourcing are key to establishing a strong financial regulator. Directors encouraged the authorities to request an FSAP assessment.

Directors agreed that a return to growth-friendly fiscal consolidation is necessary—following an easing of the fiscal stance in 2019 to accommodate social support and regional development outlays—while underscoring the importance of improving spending and investment efficiency. They supported the efforts to increase revenue collections through tax and customs administration reforms and urged the authorities to consider complementing these measures with tax policy changes to broaden the tax base and enhance progressivity. The authorities’ intentions to upgrade Kazakhstan’s fiscal policy framework are welcome and should be guided by the principles of simplicity and clarity, broad coverage, flexibility, and enforceability. The revamped framework would benefit from supporting public financial management (PFM) reforms and greater transparency. Directors noted that a PFM assessment and a fiscal transparency evaluation would be useful.

Directors reiterated the importance of decisive structural reform implementation in the context of the authorities’ economic diversification agenda. They emphasized the pivotal role of continuing improving business climate, investing in infrastructure, strengthening property rights, enhancing competition, and streamlining state support. Further improvements in governance and reducing corruption vulnerabilities would help to attract additional investment and promote private-sector-led inclusive growth.

|

Population (2018): 18.4 million |

Per capita GDP (2018 - est., US$): 9,401 |

||||

|

Quota: SDR 1,158.40 million |

Literacy rate: 99.8% (2015) |

||||

|

Main export: crude oil, metals, minerals |

Poverty rate: 2.5% (2017) |

||||

|

Key export markets: EU, China, Russia |

|||||

|

2017 |

2018 |

2019 |

2020 |

2021 |

|

|

(proj.) |

|||||

|

Output |

|||||

|

Real GDP growth (%) |

4.1 |

4.1 |

4.1 |

3.6 |

3.8 |

|

Real oil |

8.7 |

8.4 |

-0.3 |

0.0 |

1.4 |

|

Real non-oil |

2.7 |

2.7 |

5.6 |

4.8 |

4.5 |

|

Crude oil and gas condensate production (million tons) |

86 |

90 |

90 |

90 |

91 |

|

Employment |

|||||

|

Unemployment (%) |

4.9 |

4.9 |

4.9 |

4.9 |

4.9 |

|

Prices |

|||||

|

Inflation (%) |

7.3 |

5.3 |

5.6 |

5.5 |

5.0 |

|

General government finances 1/ |

|||||

|

Revenue (% GDP) |

19.8 |

21.4 |

19.9 |

20.1 |

20.4 |

|

Of which: oil revenue |

5.9 |

7.4 |

6.8 |

6.4 |

6.1 |

|

Expenditures (% GDP) |

24.1 |

18.9 |

20.1 |

20.1 |

19.7 |

|

Fiscal balance (% GDP) |

-4.3 |

2.5 |

-0.2 |

0.1 |

0.6 |

|

Non-oil fiscal balance (% GDP) |

-10.2 |

-4.9 |

-7.0 |

-6.4 |

-5.4 |

|

Gross public debt (% GDP) |

19.9 |

20.3 |

20.7 |

21.0 |

20.7 |

|

Money and credit |

|||||

|

Broad money (% change) |

-1.7 |

7.0 |

0.8 |

5.6 |

5.8 |

|

Credit to the private sector (% GDP) |

25.8 |

22.7 |

21.4 |

21.5 |

21.8 |

|

NBK policy rate (%, eop) |

10.3 |

9.3 |

… |

… |

… |

|

Balance of payments |

|||||

|

Current account (% GDP) |

-3.1 |

-0.2 |

-2.8 |

-2.8 |

-3.2 |

|

Net foreign direct investments (% GDP) |

-2.3 |

-2.7 |

-3.6 |

-3.6 |

-3.6 |

|

NBK reserves (in months of next year's imports of G&S) |

8.0 |

7.5 |

7.2 |

7.3 |

7.3 |

|

NFRK assets (in months of next year's imports of G&S) |

15.1 |

14.1 |

14.7 |

14.9 |

15.2 |

|

External debt (% GDP) |

100.2 |

88.5 |

91.2 |

87.0 |

82.5 |

|

Exchange rate |

|||||

|

Exchange rate (y-o-y percent change; Tenge per U.S. dollar; eop) |

-0.3 |

15.6 |

… |

… |

… |

|

Sources: Kazakhstani authorities and Fund staff estimates and projections. |

|||||

|

1/ The fiscal accounts in 2017 include a state support to the banking sector of 4 percent of GDP. |

|||||

-----