2020-01-20 11:35:00

TAJIKISTAN'S GDP UP 5.5%

IMF - January 17, 2020 - On January 13, 2020, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with the Republic of Tajikistan.

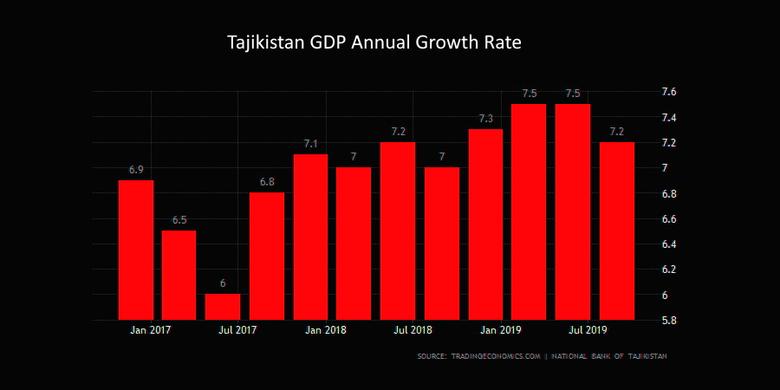

Reported economic activity has been strong in 2018-19. Inflation has picked up in the past year due to base effects and food price inflation in partner countries but remained within the National Bank of Tajikistan’s (NBT) target range. Weak remittances and exports and strong imports have contributed to a deterioration of the external current account. The real effective exchange rate has appreciated, and foreign exchange shortages have emerged. Fiscal policy has been expansionary with the overall 2019 deficit projected to reach 3.8 percent of GDP. Public and publicly guaranteed debt has been stable as the deficit has been financed from the proceeds of the 2017 Eurobond. Reforms to place the loss-making energy sector on a sound financial footing are underway. Nonetheless, debt vulnerabilities are rising on account of non-guaranteed borrowing by state-owned enterprises (SOE). The financial sector is recovering from the 2015-16 crisis, with a decline in nonperforming loans and improved profitability. The authorities have taken steps to strengthen bank supervision and regulation. However, two formerly-systemic banks remain insolvent and further reforms are needed to restore public confidence in banks.

The fiscal deficit is expected to remain high over the medium-term owing to the large Roghun hydro-power construction project, putting debt on an unsustainable path. Together with limited exchange rate flexibility, the fiscal deficit is expected to contribute to a weak external position, with the current account deficit over 5 percent of GDP. In a weak global environment, these factors are expected to weigh on confidence and growth is projected to moderate to 4 percent over the medium term. Inflation is expected to remain moderate.

Downside risks stem from potential cost overruns or difficulties in implementing large infrastructure projects would pose sizable fiscal risks. Delays in structural reforms, particularly to improve the governance of banks or state-owned enterprises, could result in additional fiscal liabilities. Slower-than-expected growth in emerging markets would reduce remittances, loans, and FDI and put further pressure on the external position and growth. Tajikistan’s risk of external debt distress remains high, suggesting heightened fiscal vulnerabilities to adverse shocks.

Executive Board Assessment

Executive Directors commended the authorities for the solid growth performance, poverty reduction, and improvements to bank supervision and regulation, as well as progress in further developing the monetary and macroprudential frameworks. Noting that continued large external and fiscal deficits create a challenging macroeconomic outlook over the medium term, Directors emphasized the importance of protecting macroeconomic stability and supporting sustainable growth. They encouraged further fiscal consolidation, greater exchange rate flexibility, measures to strengthen the financial sector, and structural reforms to improve the business environment and governance framework.

Directors encouraged fiscal consolidation measures to put debt on a downward trend, including broadening the tax base and gradually phasing out tax incentives. On public investment, they called for greater prioritization and improvements in efficiency to create fiscal space for important infrastructure projects. Targeted social assistance should be stepped up to protect vulnerable groups. Directors urged the authorities to avoid non-concessional borrowing and implement a comprehensive debt management strategy, with IMF technical assistance, to manage risks from large infrastructure projects and SOEs. Fiscal risks from the largest SOEs should be further mitigated through passage of the SOE law in line with IMF recommendations.

Directors emphasized the need for greater exchange rate flexibility to facilitate adjustment to shocks, help preserve external buffers, and support growth. Removing the exchange restriction and improving the transparency and functioning of the FX market should also be priorities, with due attention to dollarization and inflation considerations. Directors encouraged further efforts to strengthen the monetary policy framework and transmission. They considered that the National Bank of Tajikistan’s (NBT) planned transition to inflation targeting remains an appropriate medium-term goal and would be supported by enhancements to exchange rate flexibility and the NBT’s financial position and independence. As inflationary pressures have risen in recent months, Directors considered that tighter monetary policy might be needed to mitigate possible second-round effects.

Directors emphasized that, despite the reduction in NPLs and improved profitability of banks, more is needed to restore financial stability and boost confidence in the banking sector. In this regard, an important priority to be considered is the liquidation of two formerly-systemic insolvent banks and payout of insured depositors. Directors also highlighted the importance of continued efforts to strengthen bank governance and supervision, and implementation of AML/CFT policies to mitigate pressures on correspondent banking relationships and boost financial integrity.

Directors encouraged sustained and strong implementation of structural reforms to improve the business environment and foster higher and more job-rich growth in the medium term. They underscored the importance of undertaking measures to improve the governance of core economic institutions and SOEs and to enhance the rule of law and anti-corruption policies to boost investment and inclusive growth. Improvements in the quality and timeliness of economic data would strengthen economic analysis and policy making.

|

Table 1. Selected Economic Indicators, 2017–22 |

||||||

|

(Quota: SDR 174 million) |

||||||

|

(Population: 9.1 million; 2018) |

||||||

|

(Per capita GDP: US$827; 2018) |

||||||

|

(Poverty rate: 29 percent; 2017) |

||||||

|

(Main exports: mineral products, aluminum, cotton; 2018) |

||||||

|

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|

|

Est. |

Proj. |

|||||

|

National accounts |

(Annual Percent Change, unless otherwise indicated) |

|||||

|

Real GDP |

7.1 |

7.3 |

5.5 |

4.7 |

4.5 |

4.5 |

|

Headline CPI inflation (end-of-period) |

6.7 |

5.4 |

7.4 |

6.8 |

6.7 |

6.5 |

|

General government finances |

(Percent of GDP, unless otherwise indicated) |

|||||

|

Revenue and grants |

29.7 |

29.1 |

26.7 |

27.2 |

27.2 |

27.1 |

|

Tax revenue |

21.6 |

21.3 |

20.1 |

20.2 |

20.2 |

20.2 |

|

Expenditure and net lending |

35.6 |

31.9 |

30.4 |

31.5 |

31.5 |

31.4 |

|

Current |

17.0 |

17.2 |

17.7 |

17.9 |

17.9 |

17.7 |

|

Capital |

18.6 |

14.6 |

12.8 |

13.5 |

13.6 |

13.7 |

|

Overall balance (excl. PIP and stat. discrepancy) |

-3.4 |

1.6 |

0.5 |

1.5 |

1.5 |

1.5 |

|

Overall balance (incl. PIP and stat. discrepancy) |

-6.0 |

-2.8 |

-3.8 |

-4.3 |

-4.3 |

-4.3 |

|

Total public and publicly-guaranteed debt |

50.4 |

47.9 |

45.2 |

46.4 |

47.5 |

48.9 |

|

Monetary sector |

||||||

|

Broad money (12-month percent change) |

21.9 |

5.1 |

13.5 |

12.1 |

11.8 |

11.4 |

|

Reserve money (12-month percent change) |

21.0 |

7.0 |

12.1 |

11.7 |

11.6 |

11.1 |

|

Credit to private sector (12-month percent change) |

-20.2 |

1.3 |

7.8 |

9.3 |

9.6 |

9.8 |

|

Refinancing rate (in percent, eop/ latest value) |

16.0 |

14.8 |

... |

... |

... |

... |

|

External sector |

||||||

|

Current account balance |

2.2 |

-5.0 |

-4.5 |

-5.2 |

-5.3 |

-5.3 |

|

Trade balance (goods) |

-21.2 |

-25.1 |

-23.0 |

-23.3 |

-23.0 |

-22.8 |

|

FDI (net) |

0.9 |

3.3 |

3.0 |

2.4 |

2.1 |

1.8 |

|

Total public and publicly guaranteed external debt |

40.6 |

38.7 |

36.8 |

38.7 |

40.6 |

42.7 |

|

Memorandum items: |

||||||

|

Nominal GDP (in millions of somoni) |

61,093 |

68,844 |

77,351 |

86,130 |

95,593 |

105,622 |

|

Average exchange rate (somoni per U.S. dollar) |

8.55 |

9.15 |

… |

… |

… |

… |

|

Sources: Data provided by the Tajikistan authorities, and Fund staff estimates. |

||||||

-----

Earlier:

2018, August, 15, 10:40:00

RUSSIAN NUCLEAR IN EURASIA

WNN - Rusatom International Network - a subsidiary of Russian state nuclear corporation Rosatom - has signed a memorandum of understanding and cooperation with the Eurasian Development Bank (EDB). The memorandum provides for establishing common principles of bilateral cooperation with Armenia, Belarus, Kazakhstan, Kyrgyzstan, Tajikistan and other countries.

|