2020-02-19 11:55:00

GLOBAL OIL DEMAND 2020: 100.73 MBD

OPEC - 12 February 2020 - Monthly Oil Market Report

Oil Market Highlights

Crude Oil Price Movements

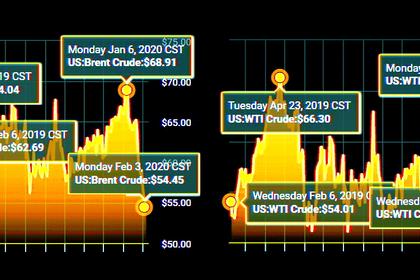

The January OPEC Reference Basket (ORB) value ended $1.38, or 2.1%, lower, month-on-month (m-o-m), averaging $65.10/b. In January, ICE Brent averaged $1.50, or 2.3%, m-o-m lower at $63.67/b, while NYMEX WTI dropped $2.28, or 3.8%, averaging $57.53/b. Year-to-date (y-t-d), ICE Brent was $3.43, or 5.7%, higher at $63.67/b, while NYMEX WTI was up by $5.98, or 11.6%, at $57.53/b, compared to a year earlier. The market structure of both ICE Brent and DME Oman remained in backwardation in January, despite the sharp decline in oil prices due to expectations of slowing global oil demand, while NYMEX WTI slipped to contango in late January. However, by early February Brent switched to contango as well. Hedge funds and other money managers reduced their net long positions in January as geopolitical tensions receded and focus turned to concerns about the impact of the Coronavirus on global economy and oil demand growth.

World Economy

Slowing 2H19 output led to a downward economic growth revision for 2019 to 2.9%. The Coronavirus-related impact, in combination with a weakening economy in the Euro-zone and India, triggered the 2020 GDP growth downward revision by 0.1 pp, reaching 3.0%. US growth remains at 2.3% for 2019 and at 1.9% for 2020. Euro-zone growth remains at 1.2% for 2019, but was lowered by 0.1 pp to 0.9% for 2020. Similarly, Japan's growth is unchanged at 1.1% for 2019, but was revised down by 0.1 pp to reach 0.6% for 2020. China's growth was revised down by 0.1 pp to 6.1% for 2019 and by 0.5 pp to 5.4% for 2020. Also, India's growth was revised down by 0.3 pp to 5.2% for 2019 and down by 0.3 pp to 6.1% for 2020. Brazil's growth remains unchanged at 1.0% for 2019 and at 2.0% for 2020. Russia's growth remains unchanged at 1.1% for 2019 and at 1.5% for 2020. While the magnitude of the coronavirus-related impact remains to be seen, ongoing solid economic performance in the US and other important OECD economies, improving global trade relations in combination with stimulus measures in China and continuing accommodative monetary policies are expected to support global growth.

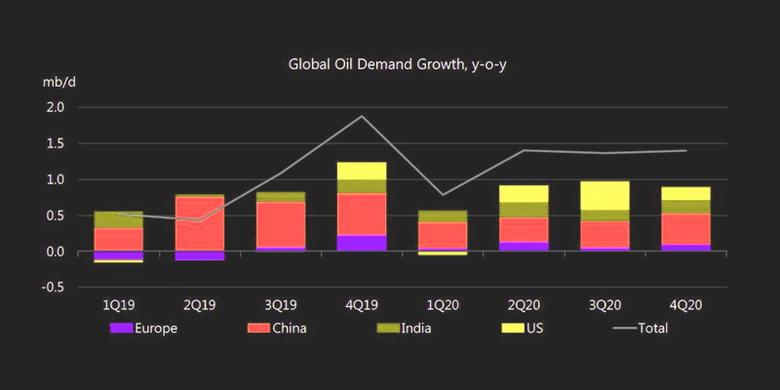

World Oil Demand

In 2019, world oil demand growth is revised down by 0.02 mb/d, from last month's assessment; amid weaker-than-expected oil demand growth data from OECD America in most parts of the year. Now, world oil demand is estimated to have grown by 0.91 mb/d and average 99.74 mb/d in 2019. Oil demand growth in 2020 is revised down by 0.23 mb/d from the previous month's assessment. With this, global oil demand is now forecast to grow by 0.99 mb/d and average 100.73 mb/d for 2020, with OECD oil demand growing by 0.01 mb/d in 2020, while non-OECD oil demand is growing by 0.98 mb/d. The outbreak of the Coronavirus in China during 1H20 is the major factor behind this downward revision.

World Oil Supply

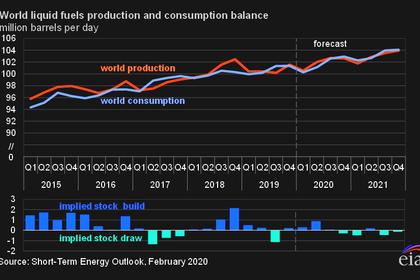

The non-OPEC liquids production growth for 2019 is revised up by 0.02 mb/d from the previous month's assessment and is now estimated at 1.88 mb/d, to average 64.36 mb/d. With this, US liquids production growth y-o-y is revised up by 11 tb/d to average 1.68 mb/d. In contrast, the non-OPEC liquids production growth forecast for 2020 is revised down by 0.10 mb/d from last month's assessment and is projected to grow by 2.25 mb/d to average 66.60 mb/d. The large downward revisions to the US liquids production forecast are partially offset by other regions' upward adjustments. The US liquids production growth forecast for 2020 is revised down by 166 tb/d, to grow by 1.26 mb/d y-o-y. The US is expected to remain the main growth driver in 2020, along with Norway, Brazil, Canada, Guyana and Australia. OPEC NGLs production in 2019 is estimated to have grown by 0.04 mb/d to average 4.80 mb/d and for 2020 is forecast to grow by 0.03 mb/d to average 4.83 mb/d. In January, OPEC crude oil production has fallen by 509 tb/d m-o-m to average 28.86 mb/d, according to secondary sources.

Product Markets and Refining Operations

Product markets in January showed mixed results. In the USGC, high product inventory levels – particularly for gasoline – and poor heating oil demand continued to weigh on US refining economics. In Europe, product markets witness considerable gains, as all products – except for gasoil – were supported by firm exports to the Middle East on the back of heavy turnarounds in that region. Meanwhile in Asia, product markets witnessed a mild upside, driven by solid high sulphur fuel oil (HSFO) gains although all other product crack spreads experienced losses. High sulphur fuel oil markets continued the upward trend for the second consecutive month, supported by increasingly tighter supplies from refineries amid lower feedstock prices and stronger import requirements from the Middle East.

Tanker Market

Dirty tanker spot freight rates in January continued the roller coast movement seen since September, this time giving back almost half the gains seen the month before. However, rates remained some 50% higher than the same month last year, as the market remained optimistic about an improvement in rates in 2020. Seasonal factors were a key contributor to the decline. The outbreak and rapid spread of the coronavirus temporarily upended the tanker market starting at the end of January, disrupting trade with China, the world's largest crude importer. It remains to be seen when and how this health challenge will be resolved, but is certain to weigh on rates in February. After rising steadily since September 2019, clean tanker rates fell back in January, but remain slightly higher than the same month last year. Rates benefited from a strong start to the year, but have fallen in recent weeks driven by seasonal factors.

Stock Movements

Preliminary data for December showed that total OECD commercial oil stocks rose by 6.8 mb m-o-m to stand at 2,918 mb, which was 45 mb higher than the same time one year ago, and around 30 mb above the latest five-year average. Within the components, crude stocks fell by 15 mb m-o-m to stand at 38 mb above the latest five-year average, while product stocks rose by 22 mb, m-o-m to remain 9 mb below the latest five-year average. In terms of days of forward cover, OECD commercial stocks rose by 0.6 days m-o-m in December to stand at 61 days, which was 0.8 days above the same period in 2018, but 0.1 days below the latest five-year average.

Balance of Supply and Demand

Demand for OPEC crude in 2019 remained unchanged from the previous report to stand at 30.6 mb/d, 1.0 mb/d lower than the 2018 level. Demand for OPEC crude in 2020 was revised down by 0.2 mb/d from the previous report, to stand at 29.3 mb/d, around 1.3 mb/d lower than the 2019 level. The main reason behind the oil demand growth revision and hence the demand for OPEC crude, is the outbreak of the Coronavirus and its expected impact on China's oil demand and, by extension, global oil demand.

-----

Earlier:

2020, February, 17, 12:05:00

OIL PRICE: ABOVE $57

Brent was at $57.27 a barrel, WTI rose 3 cents to $52.08 a barrel,

2020, February, 12, 12:15:00

OPEC+ PRODUCTION DOWN BY 500 TBD

OPEC members and allied oil producers, the so-called OPEC+, have agreed to cut their crude oil production by an additional 500,000 bbl/d until their next meeting in early March 2020.

2020, February, 12, 12:12:00

OIL PRICES 2020-21: $61-68

EIA forecasts Brent prices will average $61/b in 2020; with prices averaging $58/b during the first half of the year and $64/b during the second half of the year. EIA forecasts the average Brent prices will rise to an average of $68/b in 2021.

2020, February, 5, 11:25:00

OIL MARKET: WITHOUT A PANIC

"Any overreaction...is not in the interest of the general public, let alone the oil market. We have the consensus that we would not like to see this."