2020-03-16 10:20:00

AFRICA HOPES FOR GAS

GP - As 2020 begins, Africa's gas market is left with a mixed bag of achievements that only partly confirms a prediction by the International Gas Union (IGU) in early 2019 that the continent's natural gas segment is "facing a potential turning point."

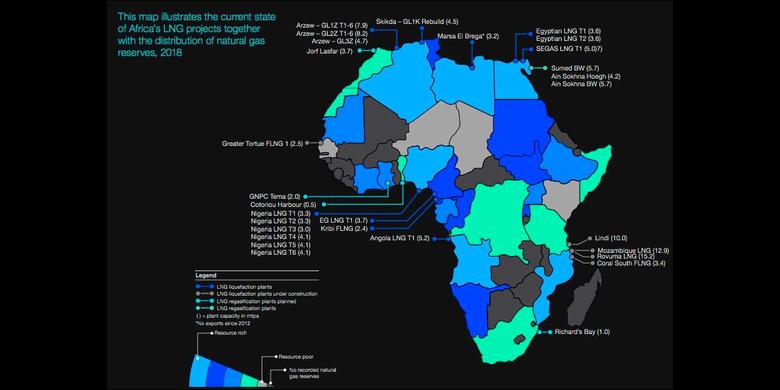

Africa hopes to exploit its 509.6 Tft3 of proven natural gas reserves, which amount to nearly 7.3% of global total reserves of 6,951.8 Tft3. A growing interest is seen in both offshore and onshore hydrocarbon assets and the on-and-off fast-tracking of announced investments to monetize previous gas discoveries.

Nigeria, Algeria, Egypt and Libya have estimated proven natural gas reserves of 188.8 Tft3, 153.1 Tft3, 75.5 Tft3 and 50.5 Tft3, respectively. Mozambique (with 130 Tft3–180 Tft3) and Tanzania (with 57 Tft3) are the "new kids on the block" that could shape Africa's production trends going forward.

Even more promising for Africa's gas future is Italian energy giant Eni's discovery in March 2019 of more natural gas reserves at the 739-km2 Nour North Sinai concession, 50 km north of the Sinai Peninsula. In August 2019, Eni announced remarkable performance of its Zohr gas field after production peaked at more than 2.7 Bft3d—another indication of the reversal of Egypt's gas industry downturn earlier in the past decade.

Despite maturing fields in producing countries, such as Algeria and Nigeria, greater output of natural gas is expected as Africa strives to discard dirty sources of fuel in the production of electricity and embrace cleaner sources like natural gas, wind and solar. Channeling a portion of the natural gas produced in Africa for power production would also help mitigate the roughly $120 B Africa needs to narrow the electricity deficit across the continent. At present, an estimated 600 MM people in Africa are not connected to the electrical grid.

Already, some countries have integrated future gas production or imports into their electricity generation programs. For example, South Africa is seeking greater partnership with Mozambique, which has been producing gas from its Pande and Temane fields prior to the huge discoveries in the Rovuma basin by Anadarko (Area 1) and Eni (Area 4). The Pande/Temane fields supply South Africa's domestic gas requirements through an 865-km pipeline owned by South African chemical company Sasol.

Race for LNG faces hurdles. Power generation is not the only driver in the race to ramp up natural gas production in Africa. Demand for LNG in the Asian and European markets has also appetized production in markets such as Mozambique and Nigeria, where conducive gas monetization policies have catalyzed not only more natural gas exploration but also production and processing.

However, expectations of a rapid increase in Africa's liquefaction capacity were held back in 2019 by a mixture of lackluster economic performance, regulatory and fiscal policy uncertainties in producing countries, and reluctance by potential LNG offtakers to sign contracts with international oil companies because of global pricing instability. LNG projects lined up for progress in Mozambique, Senegal, Mauritania, Tanzania, Nigeria and Equatorial Guinea have faced more delays as the governments and international gas companies haggle over financing and sector policy issues.

Mozambique is still reeling from the effects of Tropical Cyclone Idai, which killed more than 1,300 people in March 2019 and caused destruction estimated at $2.2 B across Mozambique, Zimbabwe and Malawi. As a result, Mozambique is facing the worst debt crisis in its history, which is directly impacting two LNG projects eyeing final investment decisions (FIDs). Mozambique's debt has ballooned by 30% to nearly $14.8 B, according to the International Monetary Fund (IMF).

However, the IMF is optimistic on the recovery of the Mozambican economy and the fast-tracking of the LNG projects. "LNG can be a game-changer for economic transformation, development and inclusive growth, potentially lifting millions out of poverty if the right policies are put in place," commented Abebe Aemro Selassie, IMF Director–African Department, in November 2019.

The Mozambique LNG project would be the country's first onshore liquefaction project. It includes the development of the Golfinho and Atum fields in Rovuma basin's Offshore Area 1, The two fields hold an estimated 60 Tft3 of gas resources. Achievement of FID will depend on the project developers signing enough LNG buyers.

France's Total acquired the assets from US firm Anadarko, under a $3.9-B deal for the latter company's 26.5% share in the project. If completed, the project will consist of two liquefaction trains with an annual capacity of 12.9 metric MMtpy of LNG, with production expected to commence in 2024.

Also in Mozambique, ExxonMobil is leading a group of partners to develop the $20-B Rovuma LNG project, the world's biggest liquefaction facility outside of Qatar, with FID pushed back to 2020. FID was initially expected by the end of 2019. The Rovuma LNG project would produce, liquefy and market natural gas from three reservoirs of the Mamba complex located in the Rovuma basin's Area 4 block.

The Rovuma project includes the construction of two natural gas liquefaction trains, with a total LNG nameplate capacity of 15.2 metric MMtpy and associated onshore facilities. The project partners also announced government approval of LNG sales and purchase agreements for the total LNG output. In October 2019, ExxonMobil announced the award of an engineering, procurement and construction (EPC) contract to JGC, Fluor and TechnipFMC for the project.

In Tanzania, despite celebration over the discovery of more than 57 Tft3 of gas, progress in developing a proposed, 10-metric-MMtpy, two-train liquefaction terminal has been mired in delays cause by the government's ambivalence toward the country's extractive industries policy.

Although Tanzania's energy minister said that talks on the implementation of the $30-B project would transpire in mid-2019, little progress has been made between the government and the project parties, including Equinor and ExxonMobil. The Norwegian and U.S. companies hold permits for the deepwater Block 2 associated with the project. The project was initially scheduled to reach FID in 2016/2017, with LNG plant startup expected 4 yr–5 yr years later. As of mid-2019, Tanzania expects a consortium of international oil companies to begin building the terminal in 2022.

Equinor also has not renewed its Block 2 exploration license with Tanzania following the permit's expiry in June 2018. The Tanzanian government has not publicly clarified the status of the asset. Despite this, Equinor confirmed that the block continues to be in operation while the process related to the grant of a new exploration license for the block is ongoing.

Unlike Tanzania, West Africa gas producer Equatorial Guinea took a firm decision to terminate Ophir Energy's permit for Block R in early 2019, despite the company's publicized efforts to realize value for the gas it discovered. Ophir Energy described the country's action as "a very frustrating outcome" and made an additional, non-cash impairment to the asset of more than $300 MM.

Prior to its effective dismissal, Ophir Energy had unsuccessfully sought to secure financing to salvage its interest in the Fortuna LNG project in Equatorial Guinea under a partnership with OneLNG, a JV between Schlumberger and Golar LNG that collapsed in May 2019.

Delays have also been experienced in Nigeria, where the construction of a seventh liquefaction train at the Nigeria LNG project on Bonny Island is planned to boost capacity from 22 metric MMtpy to 30 metric MMtpy. Although FID was initially slated for 2018, it was not made until December of 2019. The equity partners include Total, Shell, Eni and Nigeria National Petroleum Corp. (NNPC)."

Some progress on Train 7 was announced in September 2019, when Nigeria LNG issued a letter of intent for the EPC contract to SCD JV Consortium, which comprises Italy's Saipem, Japan's Chiyoda and South Korea's Daewoo.

Meanwhile, in 2019, BP announced an equity investment in the Mauritania/Senegal joint FLNG project of Greater Tortue Ahmeyim. According to the project reports, Golar LNG subsidiary Gimi MS Corp. will convert the Gimi LNG carrier into an FLNG vessel to support the development of BP's Greater Tortue/Ahmeyim gas field. The converted vessel would have a capacity of 2.5 metric MMtpy of LNG under a 20-yr contract with BP, with operations planned to commence in 4Q 2022.

Future direction for Africa's gas. Despite the African LNG market's many missed targets for 2019, the U.S. Department of Commerce's International Trade Administration believes that several countries in sub-Saharan Africa are on the cusp of emerging as major gas producers.

Furthermore, as the IGU aptly predicts, Africa's natural gas future has plenty of room to grow. "Recent discoveries across the continent could fit well with Africa's push for industrial growth and its need for reliable electricity supply," the IGU stated.

Over the longer term, the International Energy Agency's (IEA's) "Africa Case" scenario in its "Africa Energy Outlook 2019" report, released in November 2019, foresees Africa's transformation into a major natural gas player. In this scenario, Africa's gas production would more than double by 2040, and the share of gas in the continent's energy mix would expand to roughly 24% by that year.

The IEA also foresees Mozambique and Egypt becoming major natural gas exporters to the rest of the world over the next two decades. If Mozambique can recover from its financial issues and keep its LNG plans in line, then the Rovuma basin may yield some lucrative opportunities for exporters.

-----