2020-04-08 11:50:00

OIL PRICES 2020-21: $30-$46

U.S. EIA - April 7, 2020 - SHORT-TERM ENERGY OUTLOOK

Forecast Highlights

Global liquid fuels

Although all market outlooks are subject to many risks, the April edition of EIA's Short-Term Energy Outlook is subject to heightened levels of uncertainty because the impacts of the 2019 novel coronavirus disease (COVID-19) on energy markets are still evolving. The COVID-19 pandemic has caused significant changes in energy fuel supply and demand patterns. Crude oil prices, in particular, have fallen significantly since the beginning of 2020, largely driven by the economic contraction caused by COVID-19 and a sudden increase in crude oil supply following the suspension of previously agreed upon production cuts among the Organization of the Petroleum Exporting Countries (OPEC) and partner countries. Similar uncertainties persist across EIA's outlook for other energy sources, including natural gas and electricity. Despite recent news of OPEC+ emergency meetings within the next few days to discuss production levels, without an agreement actually in place, EIA assumes no re-implementation of an OPEC+ agreement during the forecast period. If there is ultimately an agreement, this forecast will incorporate that information into its ensuing release.

EIA forecasts that the United States will return to being a net importer of crude oil and petroleum products in the third quarter of 2020 and remain a net importer in most months through the end of the forecast period. This is a result of higher net imports of crude oil and lower net exports of petroleum products. Net crude oil imports are expected to increase because as U.S. crude oil production declines, there will be fewer barrels available for export. On the petroleum product side, net exports will be lowest in the third quarter of 2020, when U.S. refinery runs are expected to decline significantly.

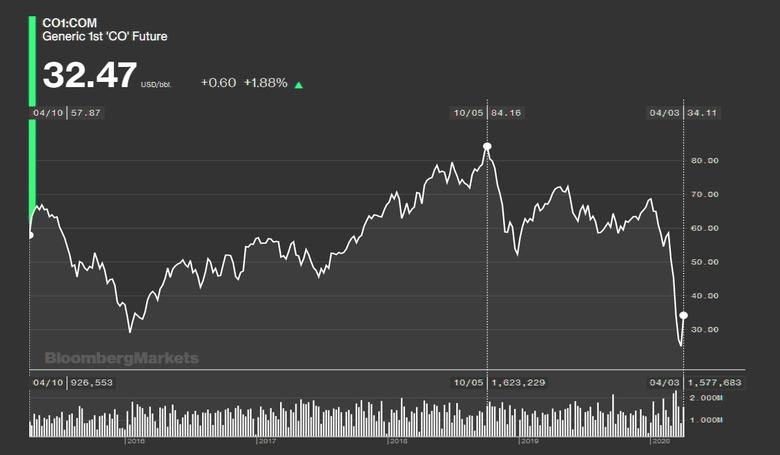

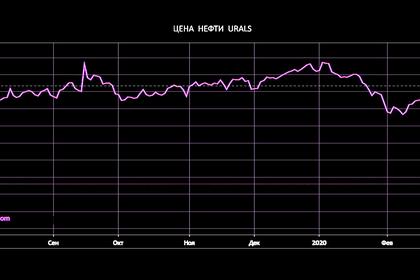

Brent crude oil prices averaged $32/barrel (b) in March, a decrease of $24/b from the average in February and the lowest monthly average since January 2016. EIA forecasts Brent crude oil prices will average $33/b in 2020, $10/b lower than in last month's STEO and down from an average of $64/b in 2019. EIA expects prices will average $23/b during the second quarter of 2020 before increasing to $30/b during the second half of the year. EIA forecasts that average Brent prices will rise to an average of $46/b in 2021, $10/b lower than forecast last month, as a return to declining global oil inventories puts upward pressure on prices.

EIA estimates global petroleum and liquid fuels consumption averaged 94.4 million barrels per day (b/d) in the first quarter of 2020, a decline of 5.6 million b/d from the same period in 2019. EIA expects global petroleum and liquid fuels demand will decrease by 5.2 million b/d in 2020 from an average of 100.7 million b/d last year before increasing by 6.4 million b/d in 2021. Lower global oil demand growth for 2020 in the April STEO reflects growing evidence of significant disruptions to global economic activity along with reduced expected travel globally because of COVID-19.

EIA expects that global liquid fuels inventories will grow by an average of 3.9 million b/d in 2020 after falling by about 0.2 million b/d in 2019. EIA expects inventory builds will be largest in the first half of 2020, rising at a rate of 5.7 million b/d in the first quarter and increasing to builds of 11.4 million b/d in the second quarter as a result of widespread travel limitations and sharp reductions in economic activity. Firmer demand growth as the global economy begins to recover and slower supply growth will contribute to global oil inventory draws beginning in the fourth quarter of 2020. EIA expects global liquid fuels inventories will decline by 1.7 million b/d in 2021.

EIA forecasts significant decreases in U.S. liquid fuels demand during the first half of 2020 as a result of COVID-19 travel restrictions and significant disruptions to business and economic activity. EIA expects that the largest impacts will occur in the second quarter of 2020, before gradually dissipating over the course of the next 18 months. EIA expects U.S. motor gasoline consumption to fall by 1.7 million b/d from the first quarter of 2020 to an average of 7.1 million b/d in the second quarter, before gradually increasing to 8.9 million b/d in the second half of the year. U.S. jet fuel consumption will fall by 0.4 million b/d from the first quarter of 2020 to average 1.2 million b/d in the second quarter. U.S. distillate fuel oil consumption would see a smaller decline, falling by 0.2 million b/d to average 3.8 million b/d over the same period. In 2020, EIA forecasts that U.S. motor gasoline consumption will average 8.4 million b/d, a decrease of 9% compared with 2019, while jet fuel and distillate fuel oil consumption will fall by 10% and 5%, respectively over the same period.

For the April–September 2020 summer driving season, EIA forecasts U.S. regular gasoline retail prices will average $1.58 per gallon (gal), down from an average of $2.72/gal last summer (Summer Fuels Outlook). The lower forecast gasoline prices reflect lower forecast crude oil prices and significantly lower gasoline demand in the second quarter of 2020 driven by COVID-19 travel restrictions and disruptions to domestic economic activity. For all of 2020, EIA expects U.S. regular gasoline retail prices to average $1.86/gal and gasoline retail prices for all grades to average $1.97/gal.

EIA has revised its current forecast of domestic crude oil production down from the March STEO, as a result of lower crude oil prices. EIA forecasts U.S. crude oil production will average 11.8 million b/d in 2020, down 0.5 million b/d from 2019. In 2021, EIA expects U.S. crude production to decline further by 0.7 million b/d. If realized, the 2020 production decline would mark the first annual decline since 2016. Typically, price changes impact production after about a six-month lag. However, current market conditions, combined with the COVID-19 pandemic, will likely reduce this lag as many producers have already announced plans to reduce capital spending and drilling levels.

Natural gas

In March, the Henry Hub natural gas spot price averaged $1.74 per million British thermal units (MMBtu). Warmer-than-normal temperatures in March reduced demand for space heating and put downward pressure on prices. EIA forecasts that prices will begin to rise at the end of the second quarter of 2020 as U.S. natural gas production declines and natural gas use for power generation increases the demand for natural gas. EIA forecasts that Henry Hub natural gas spot prices will average $2.11/MMBtu in 2020 and then increase in 2021, reaching an annual average of $2.98/MMBtu because of lower natural gas production compared to 2020.

EIA expects residential consumption of natural gas to average 12.9 billion cubic feet per day (Bcf/d) in 2020, down 5.8% from the 2019 average primarily because of warmer-than-normal weather in the first quarter. Similarly, EIA expects commercial consumption of natural gas to average 9.0 Bcf/d in 2020, a decrease of 7.1%, as a result of warm weather and the slowing economy. EIA forecasts industrial natural gas consumption to average 22.9 Bcf/d in 2020, about the same as in 2019. The industrial forecast is down from the previously expected 6.5% growth in the March STEO, as less manufacturing activity in 2020 weakens the growth potential for industrial natural gas consumption.

U.S. dry natural gas production set a record in 2019, averaging 92.2 Bcf/d. EIA forecasts dry natural gas production will average 91.7 Bcf/d in 2020, with monthly production falling from an estimated 94.4 Bcf/d in March to 87.5 Bcf/d in December. Natural gas production declines the most in the Appalachian and Permian regions. In the Appalachian region, low natural gas prices are discouraging producers from engaging in natural gas-directed drilling, and in the Permian region, low oil prices reduce associated gas output from oil-directed wells. In 2021, forecast dry natural gas production averages 87.5 Bcf/d, rising in the second half of 2021 in response to higher prices.

EIA estimates that total U.S. working natural gas in storage ended March at 2.0 trillion cubic feet (Tcf), 17% more than the five-year (2015–19) average. In the forecast, inventories rise by 1.9 Tcf during the April through October injection season to reach almost 3.9 Tcf on October 31.

EIA forecasts that U.S. liquefied natural gas exports will average 6.6 billion cubic feet per day (Bcf/d) in the second quarter of 2020 and 6.0 Bcf/d in the third quarter of 2020. Liquefied natural gas exports in the third quarter 2020 are 0.3 bcf/d lower compared with the March STEO forecast because of lower expected global demand for natural gas.

Electricity, coal, renewables, and emissions

The economic slowdown and stay-at-home orders are likely to affect U.S. electricity consumption over the next few months. EIA expects the largest impact will occur in the commercial sector where forecast retail sales of electricity fall by 4.7% in 2020 due to the closure of many businesses. Similarly, EIA expects retail sales of electricity to the industrial sector will fall by 4.2% in 2020 as many factories cut back production. Forecast U.S. sales of electricity to the residential sector fall by 0.8% in 2020, as reduced power usage resulting from milder winter and summer weather is offset by increased household electricity consumption as much of the population stays at home.

EIA forecasts that total U.S. electric power sector generation will decline by 3% in 2020. Renewable energy sources account for the largest proportion of new generating capacity in 2020, driving EIA's forecast that renewable generation by the electric power sector will grow by 11% this year. Renewable energy is typically dispatched whenever it is available because of its low operating cost. The forecast for lower overall electricity demand leads to an expected decline in fossil-fuel generation, especially at coal-fired power plants. EIA expects that coal generation will fall by 20% in 2020. Forecast natural gas generation rises by 1% this year, reflecting favorable fuel costs and the addition of new generating capacity.

Although EIA expects renewable energy to be the fastest growing source of electricity generation in 2020, the effects of COVID-19 and the resulting economic slowdown are likely to have an impact on new generating capacity builds over the next few months. EIA expects that the electric power sector will add 19.4 gigawatts of new wind capacity and 12.6 gigawatts of utility-scale solar capacity in 2020. These annual wind and solar capacity additions are 5% and 10% lower, respectively, than expected in the previous STEO.

EIA forecasts that U.S. coal production will total 537 million short tons (MMst) in 2020, down 153 MMst (22%) from 2019. Lower production reflects declining demand for coal in the electric power sector, lower demand for U.S. exports, and a number of coal mines that have been idled for extended periods as a result of COVID-19. EIA forecasts that total coal consumption will decrease by 19% in 2020, driven primarily by electric power sector demand, which will fall by 107 MMst (20%) in 2020. Total coal exports also decline, as European demand is affected by economic slowdown.

After decreasing by 2.7% in 2019, EIA forecasts that energy-related carbon dioxide (CO2) emissions will decrease by 7.5% in 2020 as the result of the slowing economy and restrictions on business and travel activity related to COVID-19. In 2021, EIA forecasts that energy-related CO2 emissions will increase by 3.6%. Energy-related CO2 emissions are sensitive to changes in weather, economic growth, energy prices, and fuel mix.

-----

Earlier:

2020, April, 7, 12:15:00

OIL PRICE: ABOVE $33

Brent was up by 80 cents, or 2.4%, at $33.85 a barrel, WTI was up by 83 cents, or 3.2%, at $26.91 a barrel

2020, April, 6, 15:00:00

OIL PRICE: NEAR $33

Brent was down $1.23, or 3.6%, at $32.88 a barrel, WTI was $1.01, or 3.6%, lower at $27.33 a barrel

2020, April, 6, 14:55:00

ВЗАИМОДЕЙСТВИЕ ОПЕК+ РОССИЯ

«Россия считает необходимым объединить эти усилия. Мы готовы к договоренностям с партнерами и в рамках механизма ОПЕК+, и к взаимодействию с США по этому вопросу. В результате необходимо сократить добычу, предварительно, на 10 млн баррелей в сутки. Это должно происходить по-партнерски. Все понимают, что речь может идти о сокращении от уровня добычи 1 квартала текущего года», - подчеркнул Президент.

2020, April, 6, 14:50:00

СПРОС НА НЕФТЬ ВЫРАСТЕТ

«На нефтяном рынке спрос также падает, на 10-15%. Мы надеемся, что в течение нескольких месяцев с постепенным увеличением экономической активности спрос все же будет нарастать», - сказал Александр Новак.

2020, April, 6, 14:45:00

ВОЗМОЖНОСТЬ ОПЕК+ РОССИЯ

Мы при необходимости не исключаем и такой вариант развития событий. Если такое желание будет у стран, входящих в ОПЕК+ и стран, которые не входят, которые тоже сегодня проявляют активность, потому что попали в трудную ситуацию, — я этот вариант не исключаю.

2020, April, 6, 14:40:00

SAUDI ARABIA, RUSSIA OIL DEAL

Saudi Arabia raised its crude output to 12.3 million bpd on April 1 and said it planned to export to more than 10 million bpd starting from April.

2020, April, 6, 14:35:00

#OilPriceWar: OPEC+ DELAY TO APRIL 9

"Russia was not a supporter of ending the OPEC+ deal. President Putin and the Russian side are overall inclined towards a constructive negotiation process, there is no alternative for stabilizing the international energy market,"