2020-05-19 11:55:00

OIL&GAS INDUSTRY: THE NEXT TRANSFORMATION

McKinsey - May 15, 2020 - The oil and gas industry is experiencing its third price collapse in 12 years. After the first two shocks, the industry rebounded, and business as usual continued. This time is different. The current context combines a supply shock with an unprecedented demand drop and a global humanitarian crisis. Additionally, the sector’s financial and structural health is worse than in previous crises. The advent of shale, excessive supply, and generous financial markets that overlooked the limited capital discipline have all contributed to poor returns. Today, with prices touching 30-year lows, and accelerating societal pressure, executives sense that change is inevitable. The COVID-19 crisis accelerates what was already shaping up to be one of the industry’s most transformative moments.

While the depth and duration of this crisis are uncertain, our research suggests that without fundamental change, it will be difficult to return to the attractive industry performance that has historically prevailed. On its current course and speed, the industry could now be entering an era defined by intense competition, technology-led rapid supply response, flat to declining demand, investor scepticism, and increasing public and government pressure regarding impact on climate and the environment. However, under most scenarios, oil and gas will remain a multi-trillion-dollar market for decades. Given its role in supplying affordable energy, it is too important to fail. The question of how to create value in the next normal is therefore fundamental.

To change the current paradigm, the industry will need to dig deep and tap its proud history of bold structural moves, innovation, and safe and profitable operations in the toughest conditions. The winners will be those that use this crisis to boldly reposition their portfolios and transform their operating models. Companies that don’t will restructure or inevitably atrophy.

A troubled industry enters the crisis

The industry operates through long megacycles of shifting supply and demand, accompanied by shocks along the way. These megacycles have seen wide swings in value creation.

After the restructurings of the early 1980s, the industry created exceptional shareholder value. From 1990 to 2005, total returns to shareholders (TRS) in all segments of the industry, except refining and marketing companies, exceeded the TRS of the S&P 500 index. Oil and gas demand grew, and OPEC helped to maintain stable prices. Companies kept costs low, as memories from the 1980s of oil at $10 per barrel (bbl) were still acute. A new class of supermajor emerged from megamergers; these companies created value for decades. Similarly, the “big three” oil-field service equipment (OFSE) companies emerged. Political openings and new technologies created opportunity for all.

From 2005 to January 2020, even as macro tailwinds such as strong demand growth and effective supply access continued, the global industry failed to keep pace with the broader market. In this period, the average of the oil and gas industry generated annual TRS growth about seven percentage points lower than the S&P 500 (Exhibit 1). Every subsegment similarly underperformed the market, and independent upstream and OFSE companies delivered zero or negative TRS. The analysis excludes companies that were not listed through this period (including some structurally advantaged national oil companies, and private companies).

In the early years of this period, the industry’s profit structure was favorable. Demand expanded at more than 1 percent annually for oil and 3 to 5 percent for liquefied natural gas (LNG). The industry’s “cost curves”—its production assets, ranked from lowest to highest cost—were steep. With considerable high-cost production necessary to meet demand, the market-clearing price rose. The same was true for both gas and LNG, whose prices were often tightly linked to oil. Even in downstream, a steep cost curve of the world’s refining capacity supported high margins.

Encouraged by this highly favorable industry structure and supported by an easy supply of capital seeking returns as interest rates fell, companies invested heavily. The race to bring more barrels onstream from more complex resources, more quickly, drove dramatic cost inflation, particularly in engineering and construction. These investments brought on massive proved-up reserves, moving world supplies from slightly short to long.

Significant investment went into shale oil and gas, with several profound implications. To begin with, shale reshaped the upstream industry’s structure. As shale oil and gas came onstream, it flattened the production-cost curve (that is, moderate-cost shale oil displaced much higher-cost production such as oil sands and coal gas), effectively lowering both the marginal cost of supply and the market-clearing price (Exhibit 2).

In another wrinkle, the rise of shale made it more challenging for OPEC to maintain market share and price discipline. While OPEC cut oil and natural gas liquids production by 5.2 million barrels per day (bpd) since 2016, shale added 7.7 million bpd over this timeframe, taking share and limiting price increases. When the industry no longer needs a decade to find and develop new resources, but can turn on ample supply in a matter of months, it will be hard to repeat the run-up in prices of 2000–14.

Historically, price wars wipe out poor performers and lead to consolidation. But the capital markets were generous with the oil industry in 2009–10 and again in 2014–16. Many investors focused on volume growth funded by debt, rather than operating cash flows and capital discipline, in the belief that prices would continue to rise and an implied “OPEC put” set a floor.

It hasn’t worked out that way.

Challenges today and tomorrow

The combination of the COVID-19 pandemic demand disruption, and a supply glut has generated an unprecedented crisis for the industry.

Short-term scenarios for supply, demand, and prices

Under most best-case scenarios, oil prices could recover in 2021 or 2022 to precrisis levels of $50/bbl to $60/bbl. Crude price differentials in this period are also likely to present both challenges and opportunities. The industry might even benefit from a modest temporary price spike, as today’s massive decline in investment results in tomorrow’s spot shortages. In two other scenarios we modeled, those price levels might not be reached until 2024. In a downside case, oil prices might not return to levels of the past. In any case, oil is in for some challenging times in the next few years.

Regional gas prices could fall much lower than in the previous megacycle. Shale gas has unlocked abundant gas resources at breakeven costs less than $2.5/MMBtu to $3.0/MMBtu.1 The pandemic has had an immediate impact, lowering gas demand by 5 to 10 percent versus precrisis growth projections. With North America becoming one of the largest LNG exporters by the early 2020s, and a sharply oversupplied LNG market, regional gas prices in Europe and Asia will be driven by prices at Henry Hub, plus cash costs for transportation and liquefaction (a premium of about $1/MMBtu to $2/MMBtu).

Demand for refined products is down at least 20 percent, and has plunged refining into crisis. We think it will be two years at least before demand recovers, with the outlook for jet fuel particularly bleak.

The immediate effects are already staggering: companies must figure out how to operate safely as infection spreads and how to deal with full storage, prices falling below cash costs for some operators, and capital markets closing for all but the largest players.

Long-term challenges

Looking out beyond today’s crisis toward the late 2030s, the macro-environment is set to become even more challenging. Start with supply and demand. We expect growth in demand for hydrocarbons, particularly oil, to peak in the 2030s, and then begin a slow decline.

Excess capacity in refining will be exposed, putting downward pressure on profits—driven by marginal pricing and, in some cases outside the growing non-OECD2 demand markets, by the economics of some refiners that seek to avoid the high cost of closing assets.

The upstream cost curve will likely stay flat. While geopolitical risks will continue to be a major factor affecting supply, new sources of low-cost, short-cycle supply will reduce the amplitude and duration of price fly-ups. The battered shale oil and gas subsector will nonetheless continue to provide supply that can be rapidly brought onstream. Its resilience might even improve as larger, stronger players consolidate the sector. Declining demand, driven by the energy transition, and global oversupply will make the task of OPEC and OPEC++ harder rather than easier.

Global gas and LNG will have a favorable role in the energy transition, ensuring a place in the future energy mix, supported by the continual demand growth in the coming decade. However, in LNG, the expected and potential cyclical capacity expansion over the decade will add pressure and volatility to global LNG contract pricing, and hence to regional gas prices. In the long term (post-2035), gas will face the same pressures as oil with peak demand and incremental economics driving decision making.

The challenge of the energy transition will continue. Today, governments are intently focused on managing the COVID-19 pandemic and mitigating the effects on economies, which is deflecting attention away from the energy transition. That said, the climate and environment debate is unlikely to go away. The innovation that has lowered costs for wind, solar, and batteries will continue and the decarbonization will remain an imperative for the industry. Negative public sentiment and investor/lender pressure that the industry has endured in the past may turn out to be mild compared with the future. The energy transition and decarbonization may even be accelerated by the current crisis.

A growing number of investors are questioning whether today’s oil and gas companies will ever generate acceptable returns. And their role in the energy transition is also uncertain. Oil and gas companies will have to prove that they can master this space. Discipline in finance, capital allocation, risk management, and governance will be critical.

The crisis as catalyst

The pandemic is first and foremost a humanitarian challenge, as well as an unprecedented economic one. The industry has responded with a Herculean effort to successfully and safely operate essential assets in this challenging time. The current crisis will have a profound impact on the industry, both short and long term. How radically the oil and gas ecosystem will reconfigure, and when, will depend on potential supply–demand outcomes and the actions of other stakeholders, such as governments, regulators, and investors. In any scenario, however, we argue that the unprecedented crisis will be a catalytic moment and accelerate permanent shifts in the industry’s ecosystem, with new future opportunities.

Implications for the industry

All companies are rightly acting to protect employees’ health and safety, and to preserve cash, in particular by cutting or deferring discretionary capital and operating expenditures and, in many cases, distributions to shareholders. These actions will not be enough for financially stretched players. We are likely to see an opportunity for a profound reset in many segments of the industry.

Upstream. A broad restructuring of several upstream basins will likely occur, underpinned by the opportunity created by balance-sheet weaknesses, particularly in US onshore and other high-cost mature basins. We could see the US onshore industry, which currently has more than 100 sizable companies, consolidate very significantly, with only large at-scale companies and smaller, truly nimble, and innovative players surviving. Broad-based consolidation could be led by “basin masters” to drive down unit costs by exploiting synergies. In the shale patch alone, we estimate that economies of skill and scale, coupled with new ways of working, could further reduce costs by up to $10/bbl, lowering shale’s breakeven point and improving supply resilience.

Downstream. Closing refineries and other assets with high costs or poor proximity to growing non-OECD markets was going to be necessary anyway, when oil demand begins a secular decline. However, as we saw in the 1980s and 1990s, governments may intervene to prop up inefficient assets, which will place additional pressure on advantaged assets elsewhere in the global refining ecosystem. Consolidation, another wave of efficiency efforts, and the hard work needed to wring out every last cent of value from optimizing refineries and their supply chains is the likely industry response. In the medium term, the value of retail networks (and access to end customers) could increase.

Midstream. Well-located midstream assets supported by contracts with creditworthy counterparties have proven a successful business model. Midstream may well continue to be a value-creating component of the oil and gas value chain, however, as demand peaks in the 2030s—there is likely to be downward pressure on rates driven by pipe-on-pipe competition.

Petrochemicals. Petrochemicals has been and could continue to be a bright spot in the portfolio for leading players. Disciplined investment in advantaged assets (such as at-scale integrated refining/petrochemical installations) that feature distinctive technologies and privileged markets should enable value creation.

Global gas and LNG. Gas is the fastest growing fossil fuel, with robust demand driven by the energy transition (for example, the shifts away from coal, and from dispatchable backup to renewables). However, the total extent of greenhouse-gas emissions is still being calculated for some LNG value chains. We estimate that global gas demand will peak in the late 2030s as electrification of heating and development of renewables may erode long-term demand. This, combined with midterm volatility, could lead to further consolidation and to an industry operating on incremental economics.

Oil-field services and equipment (OFSE) and supply chain. Much of the oil and gas supply industry was in a dire position coming into the crisis; significant over-capacity had emerged, and profitability collapsed after 2014. Despite a wave of bankruptcies and restructurings, the industry has not experienced the radical consolidation, capacity reductions, and capability upgrades needed. This restructuring may well happen now, with asset liquidation that resembles the 1980s oil bust more than the soft 2015–20 financial restructuring, and a new wave of business and supply-chain reconfiguration, technological acceleration, and partnership with customers.

National Oil Companies. National Oil Companies (NOCs) will be under additional pressure due to their important role as contributors to national budgets and governments’ societal needs. The difficult choices between industry supply discipline and market-share protection will accentuate. For NOCs not blessed with the lowest-cost resources, the pressure for fundamental change (for example, through privatization or a rethinking of collaboration with IOCs and OFSE companies) will be intense.

New businesses related to the energy transition and renewables will continue to emerge, particularly during the crises. The returns for some of these opportunities remain unclear, and the oil and gas industry will have to prove whether it can be a natural and leading participant in these businesses. Hydrogen, ammonia, methanol, new plastics, and carbon capture, utilization, and storage (CCUS) could all be interesting areas for the oil and gas industry.

The current crisis will have a profound impact on the industry, both short and long term.

How to win in the new environment

Some companies whose business models or asset bases are already distinctive can thrive in the next normal. But for most companies, a change in strategy, and potentially business model, is an imperative.

Learning from others

It is instructive to seek inspiration from other industries that experienced sector-wide change, and how the leaders within these industries emerged as value creators. The common thread in these examples is a large reallocation of capital informed by a deep understanding of market trends and future value pools, the value of focused scale, and a willingness to fundamentally challenge and transform existing operating models and basis for competition.

Steel experienced both declining demand and stranded assets due to global shifts in demand, that structurally destroyed value. However, a few players used different strategies to protect value. Mittal Steel built a model around acquiring assets with structural advantage (such as those in insulated markets, and some that allowed backward integration into advantaged raw-material supply) and then cutting costs and improving operations. Additionally, it initiated significant industry consolidation. Nucor combined industry-leading operational capabilities with a first-mover status in electric-arc furnace technology. Others focused on scale and technology in profitable niches like seamless pipe.

In automobile manufacturing, faced with rising Asian competition, US and European companies had to change. Fiat Chrysler Automobiles aggressively restructured its business model and culture by pursuing transformative mergers (Chrysler first, PSA Group lately) to gain scale in, or access to, preferred market segments, and to add global brands to its portfolio. It subsequently drove platform sharing across models and integrated supply-chain partners into its ecosystem.

In materials, 3M found a way to innovate on commodity materials that enabled it to identify high-value end markets. A telecom-equipment manufacturing company came close to demise when the telecom business collapsed at the end of the dotcom boom. It boldly reallocated resources and conducted programmatic M&A to become a leading producer of LCD glass for the booming mobile-device market.

In banking, JPMorgan Chase used its “fortress-like” balance sheet during the financial crisis to make attractive acquisitions and relentlessly pursue market leadership in segments it believed in. It was not always the first mover, but mobilized significant resources (people and capital) against several big bets. ING, the Dutch banking group, undertook a radical digital and agile transformation to fundamentally change its operating platform, which it thinks is now properly geared for the future.

Some traditional and existing models will still apply

Traditionally the super-major approach has been one model for value creation. Companies with scale, strong balance sheets, best-in-class integrated portfolios, advantaged assets, and superior operational abilities should create value even in a challenged future. Basin leadership has also long been a source of distinctiveness and value creation in oil and gas. Similarly, low-cost commodity suppliers with first-quartile assets have also thrived.

Finally, the industry features some focused business models that create value through scale, capability and operational efficiency in specific segments—such as Vitol in trading, Enterprise Products Partners in midstream, Ørsted in offshore wind, and Quantum Energy Partners in private equity. Undoubtably there will be similar opportunities to build commercially disciplined niche companies in the future.

Questions for leaders and emerging insights—the return of strategy

While the current crisis is justifiably consuming leadership time and attention, many are thinking through how to lead their companies after the crisis and are posing existential questions about their reasons for being and basis for distinctiveness. Different strategic choices are available (such as basin master, midstream and trading leader, technology specialist, first-quartile low-cost producer, value-chain integrator, energy transition specialist, and advantaged integrated refining/petrochemical player, among others). It will be unacceptable not to make clear choices. The value of the traditional multi-business model is often not sufficient enough to overcome bad operational management, poor capital allocation, or structurally disadvantaged assets. Will some large companies survive in their current form? What is the role of independents and mid-size players? How will NOCs thrive and continue to play their important societal roles in the future?

Will different forms of partnership with the supply chain be an important part of future business models? How should companies structure relationships with digital and advanced analytics companies to transform operations and to support new business models? Can technology and innovation unlock new growth for the industry: What would it take to deliver new LNG projects in a fundamentally different way at $300/ton and displace coal completely? Can the costs of CO2 mitigation be fundamentally lowered? In an era of abundance, will value flow to those that own the customer relationship and integrated value chains? Should companies make a radical shift toward renewables and away from oil and gas?

In answering these questions, companies should base their responses on three givens. The opportunity to lead has never been better—separation between market leaders and laggards will be increasingly sharp. Shaping regulation will matter, and enforcing operating standards will benefit industry and market leaders. Similarly, resilience and balance-sheet strength are non-negotiable. A new, strategic view on what the capital structure should look like, and the resultant dividend policy, is needed.

Taking bold action during the crisis to secure resilience and accelerated repositioning

Hard questions, indeed. In the meantime, winners will accept the crisis for what it is: a chance to form their own views of the future and to lead to capture new opportunities. Leaders will adopt tailored strategies that fit within their specific environment and markets in which they choose to compete, and the capabilities they bring (such as low-cost production, regional-gas or downstream-oil market leadership, value-chain integration, and specialized strengths in for example retail, trading, and distribution). In our view, all companies should act boldly on five themes, consistent with their chosen strategy:

- Reshape the portfolio, and radically reallocate capital to the highest-return opportunities. Our studies across multiple industries show that the degree of dynamic capital reallocation strongly correlates to long-term value creation (Exhibit 3). Companies should make tough and fundamental choices across the asset base and permanently reallocate capital away from lower-return businesses toward those best aligned with future value creation and sources of distinctiveness. Some companies may choose this moment to accelerate their pivot toward the energy technologies of the future. All this needs to happen in an environment in which companies must also rebuild trust with the capital markets by delivering attractive returns on capital.

- Take bold M&A moves. Could this be another age of mergers—potentially with carve-outs and spin-outs? Is now the time to drive massive consolidation and rationalization, and basin mastery, in US onshore basins such as the Permian, and across basins globally? Winners will emerge with advantaged portfolios that will be resilient to longer-term trends. They should settle for nothing less than the absolutely best positioned assets in upstream, refining, marketing, and petrochemicals.

- Unlock a step-change in performance and cost competitiveness through re-imagining the operating model. Overhead levels at some companies are more than double what they were in 2005. In most cases, these bureaucracies do not improve safety or reliability—and they certainly slow decision making. We believe that G&A and operating costs can be reduced by another 30 to 50 percent. Throughput from existing assets can also be improved significantly—in upstream, average performers have more than 20 percent opportunity, and even top-quartile performers can improve production by 3 to 5 percent. Leading companies will redouble their efforts in this moment, protecting or even scaling up technology, digital, and artificial-intelligence investments; and taking inspiration from some of the new approaches emerging from remote working, so that they do not return to business as usual once the crisis ends. The COVID-19 crisis, which has forced companies to operate in new ways, may be a catalyst to rethink the size and role of the functional teams, field crews, and management processes needed to run an efficient oil and gas company.

- Ensure supply-chain resilience through redefining strategic partnership approaches. Leading operators will act now to ensure resilience, in large part by promoting new commercial and collaborative models with an ecosystem of suppliers to radically simplify standards, processes, and interfaces; lower costs; and increase the speed and quality of the entire system. Deep strategic integration into the supply chain will be critical. “Three bids and a buy” from a deeply distressed supply chain is not a winning model. The OFSE supply chain needs to gain further scale and be able to invest in technology to reduce system costs. Within capital projects, we expect multi-project strategic cooperation and integrated project delivery (IPD) to become much more prevalent; IPD contracting aligns all participants, including sub-contractors, to one over-arching project goal.

- Create the Organization of the Future, in both talent and structure. The oil and gas industry is no longer the premier employer of choice in many markets and is struggling to attract not only the best engineers but also the best new talent in areas such as digital, technology, and commercial. All are needed to drive business-model transformation. The root causes are partly perceptual, as many young people think the sector is placed on the wrong side of the transition. But another cause is the misalignment between the career-progression timeframes and work–life choices the industry offers and the expectations of newer generations of talent. The industry can learn from this crisis. It can radically flatten hierarchies, reduce bureaucracy, and push decision making to the edge—in short, embed more agile ways of working. A new blend of talent can re-animate some of the innovative and pioneering mindsets from past periods.

Industry fundamentals have changed and the rules of the next normal will be tough. But strong performers—with resilient portfolios, innovation, and superior operating models, potentially very different from today—can outperform. The time for visionary thinking and bold action is now.

-----

Earlier:

2020, May, 18, 09:10:00

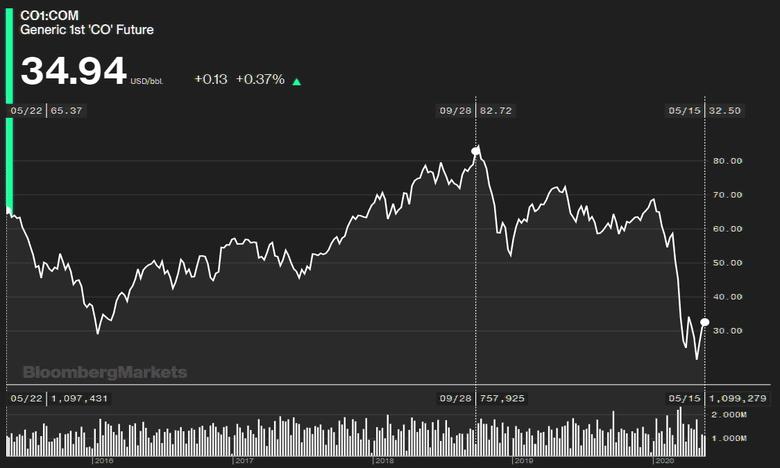

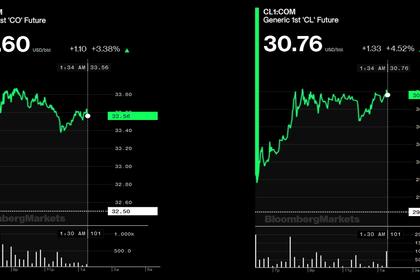

OIL PRICE: ABOVE $33

Brent was up $1.06, or 3.3%, at $33.56 a barrel, WTI was up $1.29, or 4.4%, at $30.72 a barrel

2020, May, 13, 12:45:00

OIL PRICES 2020-21: $34-$48

Brent crude oil prices will average $34/b in 2020, Brent prices will rise to an average of $48/b in 2021