2020-06-09 17:30:00

GLOBAL LNG MARKET DECELERATION

PLATTS - 09 Jun 2020 - Global LNG market growth is set to decelerate sharply in 2020 on the back of supply cuts and pandemic-driven demand destruction, with most analysts slashing their forecast for the year and some predicting an outright year-on-year contraction in LNG trade.

This is likely to be the sharpest growth deceleration the LNG market has seen in many years and contrary to the expectation that 2020 would have been one of strongest growth years for LNG with the addition of US liquefaction, which is expected be worst hit.

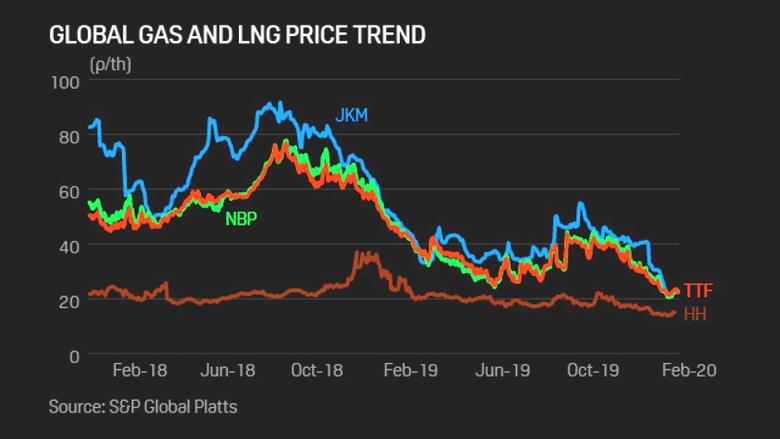

Global LNG trade in 2019 amounted to 354.73 million mt, which was an increase of 13% from 2018 and the sixth year of consecutive growth, according to the International Gas Union, a Barcelona-based gas industry trade group.

"[O]ur view is that there will be a decline in LNG demand year on year," Jason Feer, Global Head of Business Intelligence at brokerage Poten & Partners, said. His baseline for LNG trade in 2019 is just under 360 million mt/year.

Poten expects LNG demand in 2020 to fall below the 2019 levels by 6.7 million mt, and said that even this view may not be bearish enough, with a potential loss of as much as 13.8 million mt due to risks of secondary waves of the pandemic and economic recessions.

Feer said that demand declines are spread across India, Pakistan, Bangladesh, Thailand, Kuwait and Singapore, among others, while China and some European countries will show marginal growth.

Poten expects global LNG imports to average only 29 million mt/month from May through December compared with 32 million mt/month from January through April.

Consulting firm Wood Mackenzie cut its 2020 growth estimates and expects a net LNG market size of 356.8 million mt this year, after adjusting for re-exports.

"We have already reduced our 2020 supply outlook by 15.6 million mt, but are still expecting overall growth of 9.8 million mt of supply," Wood Mackenzie's research director Robert Sims said.

"However this is not evenly spread across the year. In fact, we are expecting a contraction in the summer 2020 months vs summer 2019. The first such 'annual season on season' contraction for 8 years, since winter 2012," Sims said. It expects summer demand to fall 2.7% or 3 million mt year-on-year.

He however, said there was the chance that low LNG spot and oil-indexed contract prices could trigger Indian industrial demand, and accelerate Japanese and Korean coal-to-gas switching demand.

S&P Global Platts Analytics has also pared its 2020 LNG market growth estimate from the previous forecast of 18 million mt/year, but still expects the market to grow.

"We are now expecting the 2020 market to be roughly 364 million mt/year, which is a growth of around 9 million mt/year above 2019 levels," Jeff Moore, Manager, Asian LNG Analytics said.

DEMAND DESTRUCTION TO HIT SUPPLIES

The bulk of the LNG supply cuts in 2020 will come from the US, but Australia, Malaysia and Indonesia in Asia Pacific are not immune.

Platts Analytics said in its monthly report for May published on June 8 that liquefaction utilization in the US is expected to fall below the 50% mark in the months ahead, while utilizations out of Australia and Qatar will remain above the 80% mark.

It said "the reality for the world's top LNG exporters is that they will all be forced to sacrifice volumes on the respective alters of regional demand destruction" and that "some exporters are more equal than others."

"Qatar clearly reigns as the exporter of first resort, while in the US, volumes are falling off a cliff," Platts Analytics said in the monthly report.

The "sacrifices" are dictated by a range of factors, such as the nature of contracts, exposure to spot prices, geographical proximity to customers and trade relationships.

"Supply projects in the Asia Pacific have a harder time adjusting output to price signals as compared to US LNG projects," Edmund Siau, Lead Analyst at energy consultant FGE said.

He said project commercial structures often limit production flexibility, especially if there are different stakeholders in upstream gas, LNG liquefaction, and LNG offtake.

"It takes one player with strong control over the value chain to make such a decision," Siau said. For example, Malaysia's LNG exports have been declining as Petronas is adjusting LNG production, he added.

Others like Australia don't have a single national oil company, and along with Indonesia, are at the mercy of domestic gas demand fundamentals.

Wood Mackenzie's Sims said some Australian East Coast projects had exercised downward quantity tolerances, or DQT, which allow buyers to lower contractual volumes, and the companies were seeking better domestic netbacks where possible.

He cut LNG supply growth forecasts for all three Asian suppliers for 2020, expecting a growth of 0.9 million mt in Australia, a decline of 0.8 million mt in Indonesia and a decline of 0.3 million mt in Malaysia.

-----