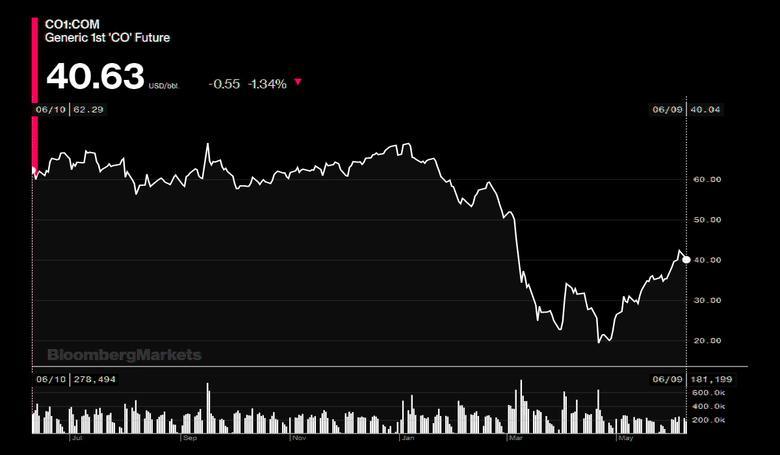

2020-06-10 12:55:00

OIL PRICES 2020-21: $37-$48

U.S. EIA - June 9, 2020 - SHORT-TERM ENERGY OUTLOOK

Forecast Highlights

Global liquid fuels

- Although revisions to EIA’s forecasts in the June STEO are generally smaller than they have been in recent months, this forecast remains subject to heightened levels of uncertainty because mitigation and reopening efforts related to the 2019 novel coronavirus disease (COVID-19) continue to evolve. Reduced economic activity related to the COVID-19 pandemic has caused changes in energy supply and demand patterns in 2020, particularly for petroleum and other liquid fuels. Uncertainties persist across EIA’s outlook for other energy sources, including natural gas, electricity, coal, and renewables.

- Daily Brent crude oil spot prices averaged $29 per barrel (b) in May, up $11/b from the average in April. Oil prices rose in May as initial data show global oil demand was higher than EIA had forecast and as adherence to announced production cuts by Organization of the Petroleum Exporting Countries (OPEC) and partner countries (OPEC+) was high. EIA expects monthly Brent prices will average $37/b during the second half of 2020 and rise to an average of $48/b in 2021. The forecast of rising crude oil prices reflects expected declines in global oil inventories during the second half of 2020 and through 2021. EIA expects high inventory levels and spare crude oil production capacity will limit upward price pressures in the coming months, but as inventories decline into 2021, those upward price pressures will increase.

- EIA forecasts that demand for global petroleum and liquid fuels will average 83.8 million barrels per day (b/d) in the second quarter of 2020, 16.6 million b/d lower than at the same time last year. Lower demand is the result of COVID-19-related shutdowns throughout much of the world. As stay-at-home orders are eased, EIA expects liquid fuels consumption will rise to an average of 94.9 million b/d in the third quarter (down 6.7 million b/d year over year). EIA forecasts that consumption of petroleum and liquid fuels globally will average 92.5 million b/d for all of 2020, down 8.3 million b/d from 2019, before increasing by 7.2 million b/d in 2021.

- EIA expects the supply of liquid fuels globally will average 92.6 million b/d in the second quarter of 2020, down 7.9 million b/d year over year. The declines reflect voluntary supply cuts by OPEC+ and reductions in drilling activity in the United States because of low oil prices. Supply of oil fell by less than demand in the second quarter, and EIA expects supply to be slower to increase. In the forecast, the global supply of oil declines to 92.0 million b/d in the third quarter before rising to an annual average of 97.4 million b/d in 2021. EIA expects OPEC to drive supply growth in 2021.

- EIA expects that global liquid fuels inventories will grow by an average of 2.2 million b/d in 2020. EIA estimates inventories rose from January through May at an average rate of 9.4 million b/d. The builds, which peaked during April, were the result of a sharp decline in global oil demand because of widespread travel limitations and reduced economic activity. EIA estimates that global oil inventories at the end of May stood 1.4 billion barrels higher than they were at the end of 2019. However, EIA now expects global oil inventories will begin declining in June, a month earlier than previously forecast, with draws continuing through the end of 2021. The sooner-than-expected draws are the result of sharper declines in global oil production during June and higher global oil demand than previously expected. EIA expects global liquid fuels inventories will fall at an average rate of 2.5 million b/d from June 2020 through the end of 2021.

- EIA forecasts U.S. liquid fuels consumption will average 15.7 million b/d in the second quarter of 2020, down 4.6 million b/d (23%) from the same period in 2019. The decline reflects travel restrictions and reduced economic activity related to COVID-19 mitigation efforts. EIA expects the largest declines in U.S. oil consumption have already occurred and demand will generally rise during the next 18 months. EIA forecasts U.S. liquid fuels consumption will average 18.4 million b/d in the third quarter of 2020 (down 2.3 million b/d year-over-year) before rising to an average of 19.5 million b/d in 2021. Although that level would be 1.4 million b/d more than EIA’s forecast 2020 consumption, it would be 1.0 million b/d less than the 2019 average.

- Declines in U.S. liquid fuels consumption vary across products. EIA expects jet fuel consumption to fall by 64% year-over-year in the second quarter of 2020, while gasoline consumption falls by 26% and distillate consumption falls by 17%. EIA forecasts the consumption of all three fuels to rise in the third quarter and into 2021 but to remain lower than 2019 levels.

- EIA estimates U.S. crude oil production fell from a record 12.9 million b/d in November 2019 to 11.4 million b/d in May 2020 as Baker Hughes reported the fewest active drilling wells in the United States in their records which go back to 1987. EIA expects U.S. crude oil production will continue to decline, to 10.6 million b/d in March 2021, then increase slightly through the end of 2021. EIA forecasts that U.S. crude oil production will average 11.6 million b/d in 2020, down 0.7 million b/d from 2019. In 2021, EIA expects U.S. crude oil production will average 10.8 million b/d. This 2020 production decline would mark the first annual decline since 2016. Typically, price changes affect production after about a six-month lag. However, current market conditions have shortened this lag as many producers have already curtailed production and reduced capital spending and drilling in response to lower prices.

Natural gas

- In May, the Henry Hub natural gas spot price averaged $1.75 per million British thermal units (MMBtu). EIA forecasts that relatively low natural gas demand will keep spot prices lower than $2/MMBtu through August. However, EIA expects prices will generally rise through the end of 2021. EIA expects that natural gas price increases will be sharpest this fall and winter when they rise from an average of $2.06/MMBtu in September to $3.08/MMBtu in January. Despite EIA’s forecast of record end-of-October storage levels, EIA expects that rising demand heading into winter, combined with reduced production, will cause upward price pressures. EIA forecasts that Henry Hub natural gas spot prices will average $2.04/MMBtu in 2020 and $3.08/MMBtu in 2021.

- EIA expects that total U.S. consumption of natural gas will average 81.9 billion cubic feet per day (Bcf/d) in 2020, down 3.6% from 2019. The decline primarily reflects less consumption in the industrial-sector, which EIA forecasts will average 21.0 Bcf/d in 2020, down 8.7% from 2019 as a result of reduced manufacturing activity.

- U.S. dry natural gas production set a record in 2019, averaging 92.2 Bcf/d. EIA forecasts dry natural gas production will average 89.7 Bcf/d in 2020, with monthly production falling from 96.2 Bcf/d in November 2019 to 83.6 Bcf/d in March 2021, before increasing slightly. Natural gas production declines the most in the Appalachian and Permian regions. In the Appalachian region, low natural gas prices are discouraging producers from engaging in natural gas-directed drilling, and in the Permian region, low crude oil prices reduce associated natural gas output from oil-directed wells. In 2021, EIA’s forecast production of dry natural gas in the United States averages 85.4 Bcf/d. EIA expects production to begin rising in the second quarter of 2021 in response to higher prices.

- EIA estimates that total U.S. working natural gas in storage ended May at almost 2.8 trillion cubic feet (Tcf), 18% more than the five-year (2015–19) average. In the forecast, inventories rise by 2.1 Tcf during the April-through-October injection season to reach more than 4.1 Tcf on October 31, which would be a record.

- EIA forecasts that U.S. liquefied natural gas exports will average 5.6 Bcf/d in the second quarter of 2020 and 3.7 Bcf/d in the third quarter of 2020. EIA expects that U.S. liquefied natural gas exports will decline through the end of the summer as a result of reduced global demand for natural gas.

Electricity, coal, renewables, and emissions

- EIA forecasts 5.7% less electricity consumption in the United States in 2020, compared with 2019. The largest decline by consumption sector on a percentage basis occurs in the commercial sector, where EIA expects retail sales of electricity to fall by 9.1% this year. Forecast industrial retail electricity sales fall by 6.7%. EIA forecasts residential sector retail sales will decrease by 1.5% in 2020. Milder expected temperatures compared with 2019 reduce EIA’s forecast of electricity consumption for space heating and cooling, but that effect is partly offset by an assumed increase in electricity use by more people who are working from home. In 2021, EIA forecasts total U.S. electricity consumption will rise by 1.0%.

- EIA expects the share of U.S. utility-scale electricity generation from natural gas-fired power plants will increase from 37% in 2019 to 41% this year. In 2021, the forecast natural gas share declines to 36% in response to higher natural gas prices. Coal’s forecast share of electricity generation falls from 24% in 2019 to 17% in 2020 and then increases to 20% in 2021. Electricity generation from renewable energy sources rise from 17% in 2019 to 21% in 2020 and to 23% in 2021. The increase in the share from renewables is the result of expected additions to wind and solar generating capacity. Expected nuclear generation declines slightly in both 2020 and 2021, but its generation share rises from 20% in 2019 to an average of 22% in 2020 and 21% in 2021 because total U.S. generation falls by more than nuclear generation.

- EIA forecasts that renewable energy will be the fastest-growing source of electricity generation in 2020. EIA expects the electric power sector will add 23.2 gigawatts of new wind capacity and 12.6 gigawatts of utility-scale solar capacity in 2020. However, these future capacity additions are subject to a high degree of uncertainty, and EIA continues to monitor reported planned capacity builds.

- EIA expects coal production will decrease by 25% to 530 million short tons (MMst) in 2020. Metallurgical coal mines in Appalachia have slowed production based on reduced demand from global steel production and coking coal, and EIA forecasts production in that region will decline by 35% this year. EIA forecasts Western region production to decline by 25%, partly because of slowing demand for steam coal from key importers such as India and a decline in U.S. coal-fired generation in 2020. In 2021, EIA forecasts coal production will rise to 549 MMst because of forecast rising natural gas prices and rising demand for U.S. exports.

- After decreasing by 2.8% in 2019, EIA forecasts that U.S. energy-related carbon dioxide (CO2) emissions will decrease by 14% (714 million metric tons) in 2020. This record decline is the result of less energy consumption related to restrictions on business and travel activity and slowing economic growth related to COVID-19 mitigation efforts. CO2 emissions decline with reduced consumption of all fossil fuels, particularly coal (33%) and petroleum (13%). In 2021, EIA forecasts that energy-related CO2 emissions will increase by 5%, as the economy recovers and stay-at-home orders are lifted, for a net decrease in energy-related CO2 emissions of 9% for 2020 and 2021 combined. Energy-related CO2 emissions are sensitive to changes in weather, economic growth, energy prices, and fuel mix.

-----

Earlier:

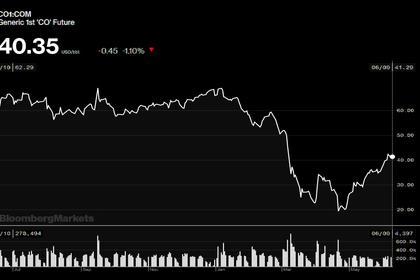

2020, June, 9, 17:50:00

OIL PRICE: ABOVE $40 ANEW

Brent was down 52 cents, or 1.3%, at $40.28 a barrel, WTI fell 27 cents, or 0.7%, to $37.92.

2020, June, 9, 17:45:00

ОПЕК+: УСПЕХ СДЕЛКИ

«Необходимо соответствовать обязательствам по соглашению - от этого зависит успех сделки. Все страны подтвердили необходимость выполнения этого соглашения. Те, кто его недовыполнил, должны в течение нескольких месяцев убрать с рынка дополнительные баррели, чтобы обеспечить полное соответствие», - сказал Александр Новак.

2020, June, 9, 17:25:00

IRAQ IS COMMITTED OPEC+

Iraq will stick to its quota in June and July and will make further reductions later on

2020, June, 8, 13:45:00

OIL PRICE: NEAR $43

Brent was up 50 cents, or 1.2%, at $42.80 per barrel, WTI rose 31 cents, or 0.8%, to $39.86 a barrel.

2020, June, 8, 13:40:00

OPEC+ EXTENDING ADJUSTMENTS

OPEC+ agreed the option of extending the first phase of the production adjustments pertaining in May and June by one further month.

2020, June, 5, 12:45:00

OIL PRICE: ABOVE $40

Brent were up 27 cents, or 0.7%, at $40.26 a barrel, WTI rose 17 cents, or 0.5%, to $37.58 a barrel.