2020-06-18 11:20:00

WORLD OIL DEMAND WILL FALL BY 9 MBD

OPEC - 17 JUNE 2020 - OPEC MONTHLY OIL MARKET REPORT

Oil Market Highlights

Crude Oil Price Movements

Spot crude oil prices rebounded in May from low levels registered a month earlier, as physical market fundamentals improved significantly. The OPEC Reference Basket (ORB) value rose by $7.51, or 42.5%, m-o-m, to stand at $25.17/b. Crude oil futures prices also bounced back in May, amid renewed optimism onthe outlook of global oil market fundamentals and expectations for a further recovery of oil demand andtightening global supply. ICE Brent increased by $5.78, or 21.7%, m-o-m to average $32.41/b, andNYMEX WTI soared by $11.83, or 70.8%, m-o-m to average $28.53/b. The contango structure of oil futuresprices flattened considerably over the month in all three markets, suggesting that the supply-demandfundamentals are gradually improving. Hedge funds and other money managers turned more positive aboutthe outlook for crude oil prices and continued to raise their combined futures and options net long positions inboth ICE Brent and NYMEX WTI contracts.

World Economy

The world economic growth forecast remains unchanged, declining by 3.4% y-o-y in 2020, following global economic growth of 2.9% in 2019. The major economies’ forecasts remain unchanged this month, except for India. The US is forecast to contract by 5.2% in 2020, following growth of 2.3% in 2019. An even larger decline of 8.0% is expected in the Euro-zone in 2020, compared to growth of 1.2% in 2019. Japan is forecast to contract by 5.1% in 2020, comparing to growth of 0.7% in 2019. China’s 2020 GDP is forecast to grow by 1.3%, following growth of 6.1% in 2019. India’s forecast was revised down to decline by 0.8%, a sharp slowdown from downwardly revised growth of 4.9% in 2019. Brazil’s economy is forecast to contract by 6.0% in 2020, following growth of 1.1% in 2019. Russia’s economy is forecast to contract by 4.5% in 2020, after growth of 1.3% in 2019, not only due to COVID-19, but also because of the considerable decline in oil prices.

World Oil Demand

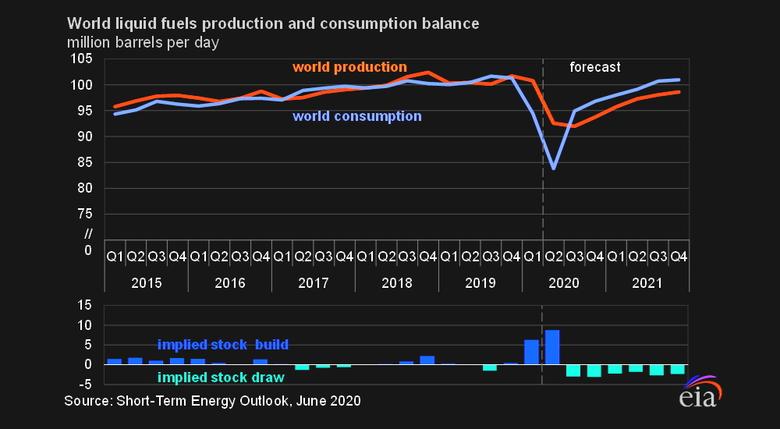

World oil demand is projected to decrease by 9.1 mb/d in 2020, unchanged from the previous month’s assessment. The COVID-19 pandemic has negatively affected global economic activities, eliminating global oil demand growth potential and leading to a y-o-y decline of 6.4 mb/d in 1Q20 and by 17.3 mb/d y-o-y in 2Q20. Transportation fuels are projected to be under pressure during 2020 as lockdowns in various countries particularly the US, Europe, India and the Middle East reduce demand for gasoline and jet fuel, as air travel and distances travelled anticipated to significantly decline compared with a year earlier. Furthermore, decreased manufacturing activities, compared with the previous year, will limit industrial fuel requirements. Petrochemical feedstock is expected to be driven by slower end-user requirements for plastics and plastic products, compared to previous years. Considering the large uncertainties going forward, new data and developments may warrant further revisions in the near term. For 2019, world oil demand growth is kept unchanged at 0.83 mb/d as OECD oil demand declined by 0.10 mb/d while non-OECD oil demand increased by 0.93 mb/d.

World Oil Supply

Non-OPEC liquids production growth in 2020 (including processing gains) is revised up by 0.3 mb/d from the previous month’s assessment and is now forecast to decline by 3.2 mb/d y-o-y. The revision is based on oil production estimations for April and May in non-OPEC countries participating in Declaration of Cooperation (DoC). Strong conformity with the voluntary production adjustments by the 10 non-OPEC participating countries in the DoC led to a drop in crude oil output of more than 2.59 mb/d in May, while OPEC-10 cut 6.25 mb/d m-o-m. At the same time, preliminary oil production outside the DoC showed a decrease by 2.0 mb/d in April and furthermore by 0.8 mb/d in May, mainly in the US and Canada. Oil supply in 2020 is forecast to show growth only in Norway, Brazil, Guyana and Australia. Non-OPEC liquids production growth in 2019 was revised up by 0.01 mb/d owing to a minor upward revision in Latin America’s production in 4Q19 and is now estimated to have grown by 2.03 mb/d to average 65.03 mb/d for the year. OPEC NGLs are estimated to have declined by 0.08 mb/d y-o-y in 2019 to average 5.26 mb/d, while the preliminary 2020 forecast indicates a decline of 0.03 mb/d to average 5.23 mb/d. OPEC crude oil production in May decreased by 6.30 tb/d m-o-m to average 24.19 mb/d, according to secondary sources.

Product Markets and Refining Operations

Refinery margins globally came under heavy pressure and plummeted to record lows on the back of oil product gluts amid stronger feedstock prices. The middle section of the barrel suffered the most as the manufacturing, freight and distribution systems still operate at reduced rates. Although gasoline markets showed some upside, owing to a gradual recovery in mobility as the pandemic restrictions continue to be eased, this was insufficient to prevent the hard downfall in refining economics.

Tanker Market

Dirty tanker rates in May fell from the high levels seen since mid-March. Production adjustments by OPEC and participating non-OPEC countries, as well as other major producers have eased the pressure seen on demand for VLCCs. A decline in product exports amid COVID-19 lockdowns have also kept clean tanker rates subdued, with both reduced refinery runs and weak product demand limiting cargoes. Floating storage has provided some support to both dirty and clean rates, however, levels are seen to be unwinding faster-than-expected.

Crude and Refined Products Trade

Preliminary data for May shows US crude imports recovering slightly to 6.0 mb/d following the arrival of long-haul volumes from the Middle East. US crude exports remained broadly steady at 3.2 mb/d, although a considerable share was headed to floating storage and oversea inventories. Product exports fell sharply in May, accelerating the decline that started in March, as COVID-19 disruptions constricted product demand in Latin America. After bottoming out at 9.7 mb/d in March, China’s crude imports picked up in April, averaging 9.9 mb/d. Preliminary customs data indicates crude imports hit a new record high of 11.3 mb/d in May. Product exports from China reached a new record high of 2.08 mb/d in April, although tanker tracking data points to a sharp fall in exports in the coming months. India’s crude imports dipped in April to average 4.2 mb/d, impacted by the government-ordered lockdown over the month. India’s product imports experienced a continued decline, weighed down by similar factors, averaging below 1.0 mb/d for the first time this year. India’s product exports edged slightly higher in April, as refiners looked to international markets to drain excessively high inventories.

Commercial Stock Movements

Preliminary April data showed that total OECD commercial oil stocks rose by 107.7 mb m-o-m to stand at 3,069 mb. This is 184 mb higher than the same time one year ago and 140.6 mb above the latest five-year average. Within the components, crude and products stocks rose by 58.1 mb and 49.6 mb m-o-m, respectively. OECD crude stocks stood at 57.9 mb above the latest five-year average, while product stocks exhibited a surplus of 82.6 mb compared to the latest five-year average. In terms of days of forward cover, OECD commercial stocks fell by 4.2 days m-o-m in April to stand at 80.7 days. This is 19.9 days above April 2019, and 18.6 days above the latest five-year average.

Balance of Supply and Demand

Demand for OPEC crude in 2019 is revised down by 0.5 mb/d from the previous assessment, standing at 29.4 mb/d, which is 1.1 mb/d lower than the 2018 level. Demand for OPEC crude in 2020 is also revised down by 0.7 mb/d from the previous month, standing at 23.6 mb/d, which is around 5.8 mb/d lower than in the previous year.

-----

Earlier:

2020, June, 17, 12:50:00

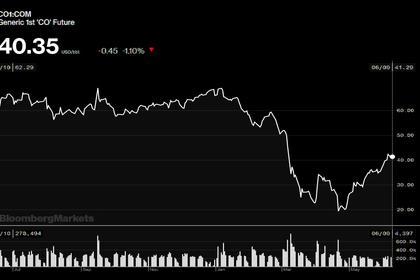

OIL PRICE: NOT ABOVE $41 ANEW

Brent was up 29 cents, or 0.7%, at $41.25 a barrel, WTI rose 17 cents, or 0.4%, to $38.55 a barrel.

2020, June, 17, 12:45:00

SAUDI ARABIA: THE TOP

Saudi Arabia exported nearly 11 million barrels of oil per day, a record, and the US about 8.6 million barrels.

2020, June, 16, 14:05:00

GLOBAL UPSRTEAM INVESTMENTS DOWN

Spending is also expected to be largely flat in 2021, landing only marginally higher than 2020 at $386 billion. Before the Covid-19 pandemic, expected total upstream investment would maintain last year’s levels, both in 2020 and 2021.

2020, June, 16, 13:55:00

U.S. PRODUCTION: OIL (-93) TBD, GAS (-693) MCFD

Crude oil production from the major US onshore regions is forecast to decrease 93,000 b/d month-over-month in June from 7,725 to 7,632 thousand barrels/day, gas production to decrease 693 million cubic feet/day from 81,254 to 80,561 million cubic feet/day .

2020, June, 11, 10:15:00

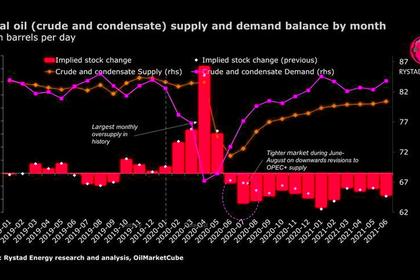

OIL MARKET DEFICIT 4 MBD

The imbalance is forecast to reach 4.6 million bpd in July, 4.2 million bpd in August

2020, June, 9, 17:45:00

ОПЕК+: УСПЕХ СДЕЛКИ

«Необходимо соответствовать обязательствам по соглашению - от этого зависит успех сделки. Все страны подтвердили необходимость выполнения этого соглашения. Те, кто его недовыполнил, должны в течение нескольких месяцев убрать с рынка дополнительные баррели, чтобы обеспечить полное соответствие», - сказал Александр Новак.