2020-07-14 12:35:00

DECENTRALIZED, DECARBONOZED ENERGY

By Stuart McCafferty President GridIntellect

ENERGYCENTRAL - Utility and transportation decarbonization is rapidly gaining traction as the economic advantages of renewable energy, technology acceleration, and a social mandate for clean energy propel us into a much different world than we have experienced over the previous century. Electric car manufacturer Tesla recently became the most valuable car manufacturer by market capitalization over long-standing companies like Toyota, GM, Ford, and Volkswagen. The electric power industry is also changing. And, the pattern in which decarbonization change is occurring is the same for both transmission and distribution companies. Understanding this pattern can help utilities be very strategic and pragmatic, even allowing them to choose whether to play defense or offense as renewable energy and other Distributed Energy Resources (DER) enter their networks.

As we have worked with various utilities and ISOs over the past several years, it is very apparent that our clients are facing the same issues and philosophical questions on when and how to move forward with DER integration and decarbonization in general. Is this a threat to our business? Or, is this an opportunity? How do we manage all this stuff? How does our organization need to change to be successful? Do we have the right underpinnings such as architecture and technologies to scale? These are the questions being asked by North American and global utilities as the realization sets in that things are changing. And fast! Much faster than most people expected.

We are transitioning from a centralized, fossil-fueled bulk power, system-centric, siloed architecture to a decentralized, decarbonized, event-driven, technology-rich, data-centric, IoT architecture. The pattern is implied in the questions asked above, and in the order they were asked. Understanding that pattern can help organizations analytically plan for their future and invest in “no regrets” internal activities and grid-mod projects.

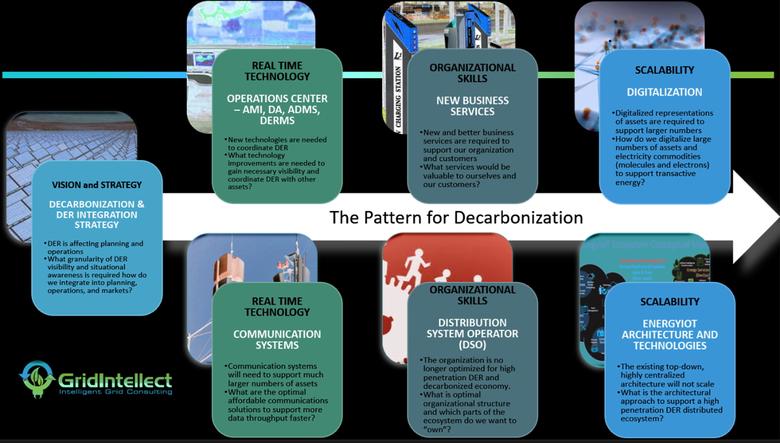

4 Steps in Planning for a Decarbonized Future

Step 1: Vision and Strategy – “Uh oh, we have DER entering our networks and we don’t know what it is, where it is, or how it affects our systems!”

The first critical step for each organization is to ask the critical question of whether to play offense or defense. Playing defense, waiting for things to settle out, and seeing this change as a threat to the current business is certainly a strategy that many utilities have played in the past successfully, but this is certainly a fundamentally different game this time. The first movers are already moving. And, there are threats outside of the normal utility businesses that are salivating at the chance to cash in on a massive industry with predictable growth by introducing new technologies or business services that disrupt the slower movers. Think about Uber and what it did to the taxi and car rental industries.

As utilities become more comfortable with managing DER, they also become more optimistic and see decarbonization as a real opportunity and align their strategy with a more offensive posture. This transition can be seen with some utilities who are encouraging customer DER adoption, increasing distribution hosting capacities, and sometimes even developing customer programs to defray customer DER costs, such as Horizon Power has done in Western Australia. The key to success is first to recognize this is reality, and second to be creative and think through different business services, models, and offerings that keep your utility relevant and profitable in the decarbonized future state.

During this first critical planning step, debates and decisions should involve:

- Is decarbonization and DER adoption a threat or an opportunity? Or both? Should you play offense or defense?

- Who are all the stakeholders? External? Internal? What does success look like for each?

- What DER visibility and situational awareness is required? At what granularity? Do you need visibility for each endpoint, or is aggregated reporting more optimal? If aggregated, at what level within the network do you need an aggregation? Building? Feeder? Substation? Other?

- What’s the strategy to integrate decarbonization and DER adoption into planning, operations, and market systems? How much do you do yourselves, and how much do you rely on from others? Can aggregators provide the proper data for forecasting DER impact on your systems or, do you need higher granularity to ensure that DER does not inadvertently and unpredictably affect your production systems?

Step 2: Real-Time Technology – “Uh oh, our communications and operational systems may not be adequate to support a decarbonized ecosystem with thousands, hundreds of thousands, or more DER!”

Next on the checklist is the recognition that operational and communication systems are insufficient to coordinate with large numbers of DER. Depending on the granularity of DER reporting decided in Step 1, communication systems may need to support much larger numbers of assets than previously. What are the fiscally and operationally most efficient communications mechanisms for connecting with large numbers of physically distributed assets? Operational systems need to be evaluated to consider how to coordinate with many small DER systems properly and to orchestrate them to perform as a highly functional system. This coordination includes all forms of DER – generation, energy storage, and demand-side management assets.

The real-time technology discussions include:

- What are the communication choices to support the needed granularity? Is 5G an opportunity? Can we leverage our existing mesh networks? Do we need to use 4G/LTE or microwave until 5G is ready? Which option(s) is best?

- Is SCADA the long-term technology solution, or will industry information models and IP-based messaging protocols eliminate that as the communications technology of the future? How does the utility prepare for this?

- Can the existing operational systems support coordination and orchestration of thousands, hundreds of thousands, or millions of DER?

- Can the EMS or DMS system support integration of utility-owned, third party, and customer-owned DER? Can the forecasting tools, power flow models, and state estimation tools support a large number of smaller assets? Are there new market opportunities because of DER that should be considered?

- Is there different data that is needed that wasn’t collected previously? Where does the data come from, and how do you get access to it? Are there any obvious gaps in the data that is needed and the data that can be collected?

Step 3: Organizational Skills – “Hmm. Do we have the best mix of services and products for our customers and partners? Is our organization set up to deliver these new capabilities?”

The third step is an organizational evaluation to determine what the future organization looks like and what services and products are needed to maximize value. These organizational changes are the part of the decarbonization process that requires a lot of creative thinking and, frankly, is a place that utilities and utility consultants often get stuck. Just selling more power is probably not a likely business outcome as DER and energy efficiency programs continue to reduce utility-provided electricity sales. So, customer-facing programs, power quality guarantees, customer DER management and maintenance become some of the more common discussions for new services. However, we are just scratching the surface at this point. Many unchartered opportunities have yet to be thought of or have been capitalized on.

Additionally, as decarbonization accelerates, the things that utilities have always done may not be what they want to do in the future. And, new things such as distribution markets may not be something that the utilities want to take on. These decisions have significant implications organizationally, technologically and for the market. In combination, these factors lead to the discussion of Distribution System Operators (DSO) and the idea that there are several functions (distribution grid operator, distribution market operator, distribution grid owner, DER manager, and DER owner) that can be distributed across multiple organizations. Determining which roles the utility wants to own will help the organization identify needed skills and better prepare and plan for the decarbonized grid.

Organizational skills conversations include:

- What are the new business services that support a DER-rich ecosystem? Who should build them? Who benefits, and what are those benefits? What are the needs to build these services? Which ones should be piloted?

- Will there be new distribution markets to allow DER owners to monetize their investments and leverage into a more holistic and resilient network model? How do those markets operate? Who should operate those markets? Can the utility participate in these new markets?

- Who should manage, coordinate, and orchestrate DER on the distribution networks?

- What is the most likely and most optimal DSO organizational model for the utility? What does the utility want to be responsible for and NOT want to be responsible for?

Step 4: Scalability – “Oh $*#@! This will never scale!”

There is a problem with the industry’s existing top-down, centralized, system-centric, siloed architecture that utility stakeholders either sense or know for a fact simply WILL NOT SCALE for 100s of thousands or millions of distributed physical assets. The scalability issue has been an ongoing conversation in standards organizations for many years. The good news is that there are alternative, elastic, event-driven, data-centric, hierarchical, decentralized architectures that will. There are also standards developed specifically to enable these architectures for the electric power industry. These modern architectures and technologies are built to capitalize on virtualization, containerization, and orchestration to push intelligence where it is needed and keep it up-to-date and stable.

Cloud-based platforms and the Internet of Things will enable “distributed intelligence,” allowing centralized control rooms to “coordinate” at system levels while hierarchical control intelligence performs direct control of assets. The resulting ecosystem will be more intelligent, automated, self-sustaining, and resilient. The ability to scale to large numbers of assets and actors will be realized. PNNL’s Grid Architecture program has named this type of hierarchical layered control as “laminar architecture,” and there is a lot of really good thinking behind it. Make no mistake. This approach is a big change for the utility industry, but it is coming, and large cloud technology providers are working on this as we speak.

Key scalability questions include:

- Is disruption right around the corner? Who will they be? Should the utility be working with them?

- What are the components of an EnergyIoT architecture? Who is leading in this area? Who should the utility work with?

- What will digitalization look like? Who is leading in this area? Who should the utility work with?

Going Forward

Decarbonization is a reality. All electric power stakeholders should do their best to embrace the change, collaborate with one another, and plan on how to make the change an opportunity rather than a problem to ignore or deny. The pattern described here is happening everywhere within the utility world. Utilities should take it one step at a time, being thoughtful, including all the appropriate stakeholders in the conversations, and allowing for some “creative thinking.” Hopefully, as you read this article, you can see where you are on the path to decarbonization and can gain some insights from the questions posed. We are happy to assist in any way.

-----

This thought leadership article was originally shared with Energy Central's Clean Power Community Group. The communities are a place where professionals in the power industry can share, learn and connect in a collaborative environment. Join the Clean Power Community today and learn from others who work in the industry.

-----

Earlier:

2020, July, 3, 11:32:00

ENERGY EFFICIENCY FOR AUSTRALIA

Australia has a real opportunity to recover its economy not only by energy efficiency but also by the Noologistical Management.