2020-08-28 14:50:00

SERBIA'S GDP WILL DOWN 3%

IMF - August 26, 2020 - IMF Executive Board Completes Fourth Review Under the Policy Coordination Instrument for the Republic of Serbia

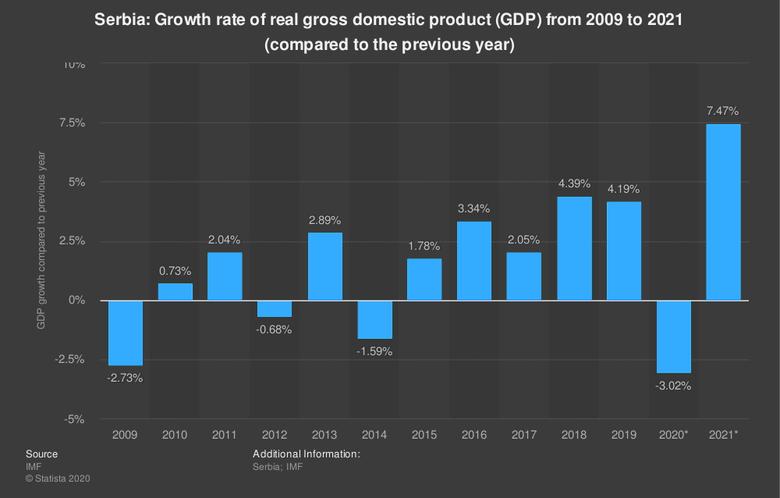

- Due to the COVID-19 pandemic, Serbia’s real GDP is projected to contract by 3 percent in 2020 and is expected recover next year with growth at 6 percent.

- To address the crisis, the authorities adopted stringent containment measures at an early stage and implemented a large policy package.

- Containing fiscal risks and preparing contingency measures is critical given the highly uncertain economic outlook.

The Executive Board of the International Monetary Fund (IMF) concluded the Fourth Review Under the Policy Coordination Instrument (PCI) for the Republic of Serbia.

The PCI was approved on July 18, 2018 (see Press Release No. 18/299) and aims at maintaining macroeconomic and financial stability, while advancing an ambitious reform agenda to foster rapid growth, job creation, and improved living standards.

The COVID-19 pandemic is negatively impacting Serbia’s economic activity. Growth is projected at -3 percent this year, compared to 4.2 percent in 2019, with lower external demand, weaker foreign direct investment and remittances, disruptions in regional and global supply chains, and domestic supply constraints. With the lockdown measures relaxed, the economy has begun to recover, and growth in 2021 is expected to be at 6 percent. Risks to the outlook are substantial given the uncertainty about the evolution of the epidemic. The recent rise in infection rates in Serbia, though from low levels, underscores these risks.

The authorities responded to the pandemic promptly by implementing stringent containment measures and a large package of fiscal, monetary, and financial sector measures. The policy measures were generally well-designed, and appropriately aimed at providing lifelines to households, preserving jobs, boosting healthcare spending, and providing sufficient liquidity to the banking system and relief to borrowers.

While the immediate policy priorities have shifted to supporting the economy through the crisis, the objectives of the PCI, which expires in January 2021, remain ambitious and appropriate. The authorities and staff agreed that going forward it will be critical to contain fiscal risks including from troubled state-owned enterprises. Absent large economic surprises, the fiscal deficit in 2021 should be contained to about 2 percent of GDP, with limited increases in public sector wages and pensions while making room for higher public investment.

At the conclusion of the Board discussion on the fourth review of the PCI for Serbia, Mr. Tao Zhang, Deputy Managing Director and Acting Chair made the following statement:

“The COVID-19 pandemic is having a significant adverse impact on Serbia’s economic activity. The authorities have launched timely and strong policy actions. The near-term outlook remains subdued and is subject to uncertainty. In this context, the authorities’ immediate policy priorities have shifted to supporting the economy through the crisis.

“The fiscal package introduced in response to the crisis is among the largest in the region, providing needed support to households and businesses, as well as higher health spending. Strong reporting and procurement practices are key for ensuring the effectiveness and proper oversight of this spending.

“Going forward, and provided that the economy sees a gradual recovery as currently projected, budget planning should balance support to the economy with a gradual return to a sustainable fiscal stance. Fiscal space should be directed to public investment, which will be critical for supporting growth, while limiting increases in public sector wages and pensions. Identifying fiscal risks stemming from the crisis will be important for underpinning the execution of the budget and projecting funding needs. Continued modernization of the tax administration will be needed to protect the main revenue streams during the crisis and the subsequent recovery.

“Monetary policy has rightly been accommodative, and temporary extraordinary measures have been adopted to help keep the banking sector liquid and support borrowing. Inflation remains low and the exchange rate stable. Continued monitoring of economic developments will be key to preserve macrofinancial stability and limit balance sheet risks.

“Financial sector reforms should continue to support the recovery and long-term growth. Priorities include completing the privatization of the largest state-owned bank, advancing capital market development, and supporting access to development finance.”

|

Table 1. Serbia: Selected Economic and Social Indicators |

||||||||||

|

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

||||

|

CR 19/369 |

Est. |

CR 19/369 |

Proj. |

CR 19/369 |

Proj. |

Proj. |

||||

|

(Percent change, unless otherwise indicated) |

||||||||||

|

Real sector 1/ |

||||||||||

|

Real GDP |

3.3 |

2.0 |

4.4 |

3.5 |

4.2 |

4.0 |

-3.0 |

4.0 |

6.0 |

6.0 |

|

Real domestic demand (absorption) |

1.4 |

3.9 |

6.5 |

4.6 |

5.2 |

4.0 |

-1.8 |

3.6 |

8.0 |

5.9 |

|

Consumer prices (average) |

1.1 |

3.1 |

2.0 |

1.9 |

1.9 |

2.0 |

1.5 |

2.2 |

1.9 |

2.3 |

|

GDP deflator |

1.5 |

3.0 |

2.1 |

3.3 |

2.5 |

3.4 |

3.8 |

3.4 |

2.3 |

2.4 |

|

Unemployment rate (in percent) 2/ |

15.9 |

14.1 |

13.3 |

… |

10.9 |

… |

… |

… |

… |

… |

|

Nominal GDP (in billions of dinars) |

4,521 |

4,754 |

5,069 |

5,417 |

5,411 |

5,827 |

5,448 |

6,264 |

5,907 |

6,414 |

|

(Percent of GDP) |

||||||||||

|

General government finances |

||||||||||

|

Revenue 3/ |

40.8 |

41.5 |

41.5 |

41.4 |

42.1 |

40.2 |

38.2 |

39.8 |

41.1 |

41.4 |

|

Expenditure 3/ |

41.9 |

40.4 |

40.9 |

42.0 |

42.3 |

40.7 |

46.8 |

40.3 |

43.2 |

42.0 |

|

Current 3/ |

37.9 |

36.7 |

36.4 |

37.2 |

37.0 |

35.9 |

42.3 |

35.6 |

37.5 |

36.3 |

|

Capital and net lending |

3.2 |

3.1 |

4.1 |

4.5 |

5.1 |

4.7 |

4.3 |

4.5 |

5.3 |

5.3 |

|

Amortization of called guarantees |

0.9 |

0.6 |

0.4 |

0.2 |

0.2 |

0.1 |

0.2 |

0.2 |

0.4 |

0.4 |

|

Fiscal balance 4/ |

-1.2 |

1.1 |

0.6 |

-0.5 |

-0.2 |

-0.5 |

-8.6 |

-0.5 |

-2.0 |

-0.5 |

|

Primary fiscal balance (cash basis) |

1.7 |

3.6 |

2.8 |

1.5 |

1.8 |

1.5 |

-6.6 |

1.5 |

-0.1 |

1.3 |

|

Structural primary fiscal balance 5/ |

1.7 |

3.7 |

2.8 |

1.8 |

1.6 |

1.6 |

1.1 |

1.6 |

1.1 |

1.1 |

|

Gross debt |

68.9 |

58.7 |

54.5 |

52.7 |

52.8 |

51.4 |

59.8 |

47.8 |

57.0 |

53.2 |

|

(End of period 12-month change, percent) |

||||||||||

|

Monetary sector |

||||||||||

|

Money (M1) |

20.3 |

9.7 |

20.1 |

10.7 |

16.3 |

9.7 |

6.0 |

8.6 |

12.2 |

11.1 |

|

Broad money (M2) |

9.8 |

3.3 |

15.0 |

8.5 |

8.8 |

7.4 |

5.5 |

6.2 |

9.0 |

8.2 |

|

Domestic credit to non-government 6/ |

1.8 |

4.4 |

10.1 |

7.2 |

9.5 |

7.3 |

6.6 |

6.9 |

8.4 |

9.0 |

|

(Period average, percent) |

||||||||||

|

Interest rates (dinar) |

||||||||||

|

NBS key policy rate |

3.3 |

3.9 |

3.1 |

… |

2.3 |

… |

… |

… |

… |

… |

|

Interest rate on new FX and FX-indexed loans |

3.1 |

3.1 |

2.8 |

… |

3.1 |

… |

… |

… |

… |

… |

|

(Percent of GDP, unless otherwise indicated) |

||||||||||

|

Balance of payments |

||||||||||

|

Current account balance |

-2.9 |

-5.2 |

-4.8 |

-5.9 |

-6.9 |

-5.3 |

-6.4 |

-5.2 |

-6.5 |

-6.3 |

|

Exports of goods |

34.9 |

35.9 |

35.2 |

36.2 |

35.8 |

36.7 |

33.2 |

37.7 |

33.5 |

35.1 |

|

Imports of goods |

-43.4 |

-46.1 |

-47.1 |

-49.2 |

-48.0 |

-49.3 |

-44.1 |

-49.7 |

-46.0 |

-47.8 |

|

Trade of goods balance |

-8.5 |

-10.2 |

-11.9 |

-13.0 |

-12.2 |

-12.6 |

-10.9 |

-12.0 |

-12.6 |

-12.7 |

|

Capital and financial account balance |

0.6 |

4.8 |

6.7 |

8.7 |

10.5 |

6.7 |

6.1 |

5.7 |

7.3 |

7.0 |

|

External debt (percent of GDP) 7/ |

76.5 |

68.9 |

66.1 |

58.4 |

66.2 |

54.7 |

68.6 |

51.1 |

65.3 |

61.5 |

|

of which: Private external debt |

29.4 |

29.7 |

30.9 |

27.5 |

31.7 |

25.7 |

30.3 |

24.3 |

29.0 |

27.4 |

|

Gross official reserves (in billions of euro) |

10.2 |

10.0 |

11.3 |

12.5 |

13.4 |

13.2 |

13.2 |

13.5 |

13.6 |

14.0 |

|

(in months of prospective imports) |

5.5 |

4.7 |

4.8 |

4.9 |

6.3 |

4.8 |

5.6 |

4.5 |

5.1 |

4.8 |

|

(percent of short-term debt) |

345.2 |

200.3 |

193.9 |

191.5 |

250.8 |

201.7 |

247.9 |

205.7 |

255.8 |

262.5 |

|

(percent of broad money, M2) |

58.7 |

53.2 |

52.2 |

54.2 |

57.8 |

53.1 |

57.2 |

50.4 |

54.8 |

52.0 |

|

(percent of risk-weighted metric) |

… |

… |

113.1 |

117.7 |

123.1 |

117.7 |

121.3 |

116.4 |

120.8 |

118.0 |

|

Exchange rate (dinar/euro, period average) |

123.1 |

121.4 |

118.3 |

… |

117.9 |

… |

… |

… |

… |

… |

|

REER (annual average change, in percent; |

||||||||||

|

+ indicates appreciation) |

-1.0 |

2.9 |

2.8 |

… |

1.0 |

… |

… |

… |

… |

… |

|

Social indicators |

||||||||||

|

Per capita GDP (in US$) |

5,756 |

6,284 |

7,246 |

7,445 |

7,382 |

8,086 |

7,458 |

8,787 |

8,442 |

9,210 |

|

Real GDP per capita (percent change) |

3.9 |

2.6 |

5.0 |

3.9 |

4.5 |

4.4 |

-2.6 |

4.4 |

6.4 |

6.4 |

|

Population (in million) |

7.1 |

7.0 |

7.0 |

7.0 |

7.0 |

6.9 |

6.9 |

6.9 |

6.9 |

6.9 |

|

Sources: Serbian authorities; and IMF staff estimates and projections. |

||||||||||

|

1/ SORS released revised national accounts in November 2018. |

||||||||||

|

2/ Unemployment rate for working age population (15-64). |

||||||||||

|

3/ Includes employer contributions. |

||||||||||

|

4/ Includes amortization of called guarantees. |

||||||||||

|

5/ Primary fiscal balance adjusted for the automatic effects of the output gap both on revenue and spending as well as one-offs. |

||||||||||

|

6/ At constant exchange rates. |

||||||||||

|

7/ After CR19/369, domestic securities held by non-residents are included in external debt. Historical data were updated since 2015. |

||||||||||

-----

Earlier:

2020, July, 16, 16:05:00

NORD STREAM 2: THE NEW SANCTIONS

The changes to the CAATSA guidance is the latest move by the US to put pressure on companies involved in building both Nord Stream 2 and the TurkStream extension in Bulgaria and Serbia into Hungary.

|

2020, February, 7, 10:30:00

EUROPE'S CLEAN ENERGY INVESTMENT $5.4 BLN

"New targeted credit lines will support climate action by companies in Bulgaria, Italy, Romania and Spain, improve access to finance by energy, tourism and education companies in Serbia, help agriculture firms in Romania to expand and encourage circular economy investment in Spain," the EIB said in a statement.

|

2019, December, 20, 09:55:00

SERBIA'S GDP UP 3.5-4.0%

Serbia's economic growth is projected at 3.5 percent in 2019 and 4 percent in 2020, with negative contributions from the external environment offset by strong domestic demand.

|