2021-01-15 12:00:00

GLOBAL OIL DEMAND WILL UP BY 5.9 MBD

OPEC - 14 JANUARY 2021 - OPEC MONTHLY OIL MARKET REPORT

Oil Market Highlights

Crude Oil Price Movements

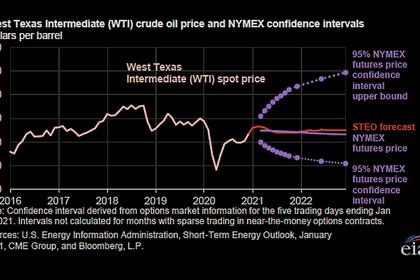

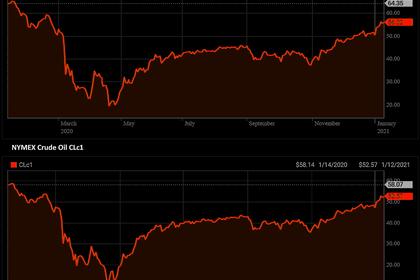

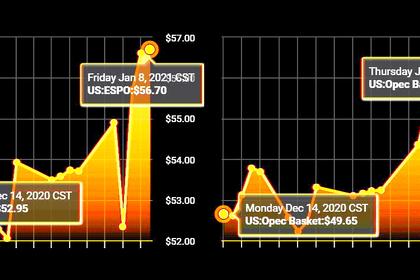

Spot crude prices settled sharply higher in December, extending the previous month’s gains, buoyed by a further improvement in physical market fundamentals and strong crude buying from the Asia Pacific region. The OPEC Reference Basket increased by $6.56, or 15%, month-on-month (m-o-m), to stand at $49.17/b in December. However, in annual terms, the ORB dropped $22.57, or 25%, to average $41.47/b in 2020, which represents the lowest yearly average since 2016. Crude oil futures prices extended their previous month’s surge in December, rising sharply on both sides of the Atlantic. The ICE Brent front month rose by $6.24, or 14.2%, m-o-m in December to average $50.22/b, while NYMEX WTI gained $5.72, or 13.8%, m-o-m to average $47.07/b. As a result, the Brent-WTI spread widened 52¢ to average $3.15/b in December. The price structure of the forward curve strengthened further in December. The ICE Brent stood in shallow backwardation for most of the month, while DME Oman and Dubai remained in strong backwardation. However, the WTI structure remained in contango. Hedge funds and other money managers continued to boost bullish positions, providing additional momentum to the steady ongoing gains in crude oil prices.

World Economy

Global economic growth was revised up slightly for 2020, after a better-than-expected performance in 3Q20. As a result, the global economy is now expected to contract by 4.1% in 2020, compared to the previous month’s forecast of -4.2%. While the 2021 forecast remains at 4.4%, recent news of fiscal stimulus in the US and the likelihood of a stronger-than-anticipated recovery in Asian economies provide potential upsides for this year’s growth prospects. US economic growth in 2020 was revised slightly higher by 0.1 percentage point (pp) to show a contraction of 3.5%, while the 2021 forecast remains at 3.4%. The Euro-zone forecast was also adjusted slightly higher by 0.1 pp to -7.2%, while the 2021 growth forecast remains at 3.7%. Japan’s figures remain unchanged, contracting by 5.2% in 2020 followed by growth of 2.8% in 2021. China’s economic growth remains at 2.0% in 2020 and at 6.9% in 2021. India is now expected to have seen a shallower contraction of 9.0% in 2020, compared to a previously forecast -9.2%. Expected growth in 2021 remains at 6.8%. Brazil’s economy is now estimated to have contracted by 5.2%, revised up from the previous expectation of -5.8%, while forecast growth in 2021 remains at 2.4%. Russia’s economy is seen contracting by 4.1% in 2020, compared to the previous forecast of -4.5%, while forecast growth in 2021 remains unchanged at 2.9%.

World Oil Demand

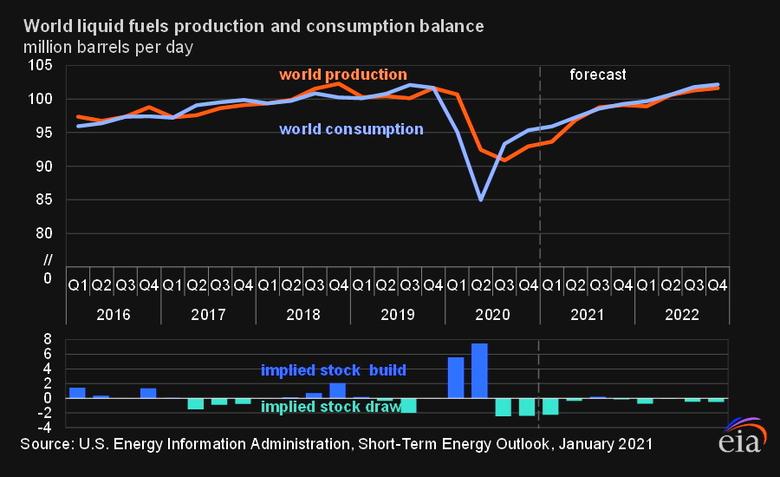

World oil demand growth in 2020 was revised marginally higher from last month’s report and is now estimated to have declined by 9.8 mb/d year-on-year (y-o-y) to average 90.0 mb/d in 2020. OECD America, led by the US, was revised lower particularly in 2H20 amid a sluggish recovery in transportation fuels. In the non-OECD region, oil demand growth was revised higher in 2020, mainly reflecting better-than-expected demand in China and India. Strong petrochemical feedstock demand along with a healthy uptick in gasoline requirements supported the upward revision in both countries. For 2021, global oil demand is forecast to increase by 5.9 mb/d y-o-y to average 95.9 mb/d. The growth forecast was kept unchanged compared to last month’s assessment. In the OECD region, oil consumption is estimated to increase by 2.6 mb/d y-o-y but will still lag pre-pandemic levels. OECD Americas is estimated to increase the most amid a rebound in transportation fuels. In the non-OECD region, oil demand is estimated to increase by 3.3 mb/d y-o-y, driven by China followed by India and Other Asia, and supported by a rebound in economic activities.

World Oil Supply

Non-OPEC liquids production in 2020 is estimated to average 62.7 mb/d, representing a contraction of 2.5 mb/d, y-o-y. This is broadly unchanged from the previous report, despite several upward and downward revisions in the production of various countries in 4Q20. The oil supply forecast for the US and Brazil was revised down, while the figures for Canada and Russia were adjusted higher due to better-than-expected output in 4Q20. The contraction in 2020 is driven mainly by Russia, the US, Canada and the UK, while production in Norway, Brazil, China, and Guyana is expected to increase. The forecast for non-OPEC supply in 2021 also remains unchanged, with growth expected at 0.8 mb/d. The upward revision in US supply offset the downward revision in the supply forecast for Russia. Market conditions have improved for US shale as oil prices have moved into a range where output is likely to recover at a higher-than-expected rate in 2H21. As a result, the US liquids supply forecast was revised up by around 0.1 mb/d to average just under 18.0 mb/d, representing y-o-y growth of 0.4 mb/d although uncertainties remain. The main contributors to supply growth are expected to be the US, Canada, Brazil and Norway. OPEC NGLs are forecast to grow by about 0.1 mb/d y-o-y in 2021 to average 5.2 mb/d, following an estimated contraction of 0.1 mb/d in 2020. OPEC crude oil production in December increased by 0.28 mb/d, m-o-m, to average 25.36 mb/d, according to secondary sources.

Product Markets and Refining Operations

Refining margins showed mixed results across the globe in December. The only positive performing region was the US, where margins were supported by strength across the barrel with the exception of fuel oil. Product markets improved on increased transportation activities during the year-end holidays, amid still-suppressed refinery intakes relative to the previous year. In Europe, margins weakened weighed down by stronger crude prices at a time of seasonal weakness with notable losses seen at the top and bottom of the barrel. The hard lockdowns implemented during the month amid pandemic-related concerns exacerbated the pressure on product markets. In Asia, refining margins experienced losses, dragged down by the fuel oil segment as utility sector demand declined. In addition, the surge in crude prices weighed further on Asian refining economics. For the most part, refineries have returned from the peak autumn refinery maintenance season, resulting in a slight rise in available spare capacity globally, awaiting the right incentives to be utilized.

Tanker Market

Dirty tanker rates experienced a slight improvement in December, while still remaining near historically low levels, amid a persistent imbalance in tanker demand and availability. VLCC and Suezmax rates saw some improvement on eastward rates from the Middle East and West Africa, as well as from West Africa to the US Gulf Coast. Meanwhile, Aframax rates declined, weighed down by a sluggish intra-Med performance. Clean tanker rates continued to pick up in December from multi-year lows seen in at the start of the fourth quarter, with gains both East and West of Suez.

Crude and Refined Products Trade

Preliminary data shows US crude imports averaged 5.6 mb/d in December, resulting in an annual average of 5.9 mb/d in 2020, the lowest since 1991. US crude exports ended the year averaging just below 3 mb/d in December, down from a record high of 3.7 mb/d in February 2020. In annual terms, US crude exports averaged 3.1 mb/d in 2020 for a y-o-y increase of 0.2 mb/d. The latest data shows Japan’s crude imports recovered for the second month in a row to average 2.3 mb/d in November, reflecting winter demand, but were still sharply lower y-o-y, declining 22%. China’s crude imports averaged 11.1 mb/d in November, recovering from a decline the month before as a backlog of inflows continued to clear customs. Preliminary data shows crude imports declining m-o-m in December. China’s product imports recovered in November from the weak performance in the previous month, averaging 1.3 mb/d, while product exports fell back from the relatively high level seen in the previous month to average almost 1.3 mb/d. India’s crude imports jumped 24% to an eight-month high, averaging 4.5 mb/d in November, as an easing of lockdown measures led refineries to boost runs. Both product imports and exports increased in November to average around 1.0 mb/d, respectively.

Commercial Stock Movements

Preliminary data shows total OECD commercial oil stocks down by 24.5 mb, m-o-m, in November. At 3,104 mb, inventories were 205.1 mb higher than the same period a year ago and 163.1 mb above the latest five-year average. Within the components, crude and products stocks declined, m-o-m, by 11.2 mb and 13.3 mb, respectively. At 1,546 mb, OECD crude oil stocks are 98.4 mb higher than the same time a year ago, and 72.6 mb above the latest five-year average. Total product inventories stood at 1,558 mb, some 106.7 mb above the same period a year ago, and 90.5 mb higher than the latest five-year average. In terms of days of forward cover, OECD commercial stocks fell, m-o-m, by 1.6 days to stand at 70.5 days in November. This is 8.8 days above the November 2019 level and 8.5 days above the latest five-year average.

Balance of Supply and Demand

Demand for OPEC crude in 2020 remained unchanged from the previous report to stand at 22.2 mb/d, around 7.1 mb/d lower than in 2019. Demand for OPEC crude in 2021 remained unchanged from the previous report to stand at 27.2 mb/d, around 5.0 mb/d higher than in 2020.

-----

Earlier:

2021, January, 13, 13:55:00

OIL PRICE: ABOVE $56

Brent was up 36 cents, or 0.6%, at $56.94 a barrel. WTI was up 34 cents, or 0.6%, at $53.55 a barrel.

2021, January, 13, 13:50:00

OIL PRICES 2021-22: $53

Brent crude oil spot prices to average $53 per barrel (b) in both 2021 and 2022 compared with an average of $42/b in 2020.

2021, January, 12, 11:40:00

OIL PRICE: NEAR $56

Brent climbed 22 cents, or 0.4%, to $55.88 a barrel. WTI gained 25 cents, or 0.5%, to $52.50 a barrel.

2021, January, 12, 11:35:00

ABU DHABI OIL PRICE UP

Government-owned Abu Dhabi National Oil Co. set Murban crude at a premium of 75 cents a barrel to the regional benchmark,

2021, January, 11, 13:00:00

ЦЕНА URALS: $41,73

Средняя цена на нефть марки Urals в январе-декабре 2020 года сложилась в размере $41,73 за баррель, в январе-декабре 2019 года - $63,59 за баррель.

2021, January, 11, 12:55:00

РОССИЯ ВЫПОЛНЯЕТ УСЛОВИЯ СДЕЛКИ

«В феврале, а также в марте Россия будет увеличивать добычу по 65 тыс. баррелей в сутки, суммарно это 130 тыс. баррелей к январскому уровню. Россия ответственно относится к сделке, мы выполняем её условия близко к 100% и полностью соответствуем тому, что заложено в соглашении, с учетом постепенного увеличения спроса», – отметил вице-премьер.

2020, December, 25, 10:40:00

OPEC+ RISSIA OIL PRICE: $45 - $55

In comments, cleared for publication on Friday, Novak also said that Moscow views an oil price between $45 and $55 per barrel as the optimum level to allow for recovery of its oil production,