2021-10-22 11:20:00

GLOBAL CARBON EMISSIONS WILL UP

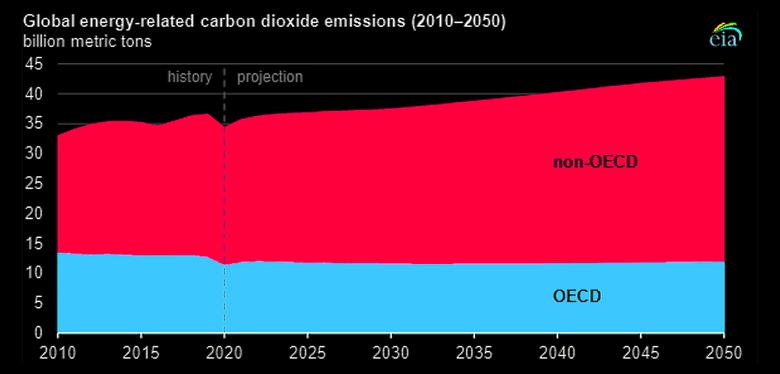

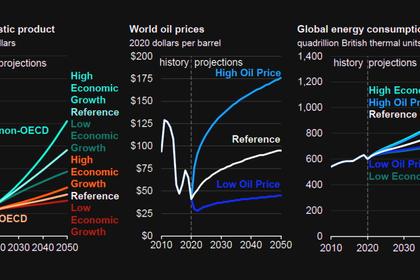

U.S. EIA - OCTOBER 21, 2021 - In our International Energy Outlook 2021, we project that global energy-related carbon dioxide (CO2) emissions will increase for countries both inside and outside of the Organization for Economic Cooperation and Development (OECD) over the next 30 years under current laws and regulations. Between 2020 and 2050, we project that total energy-related CO2 emissions will increase by 5% (600 million metric tons) in OECD countries (which generally have slowly growing economies) and by 35% (8 billion metric tons) in non-OECD countries (which generally have rapidly growing economies).

We project that carbon intensity, measured as emissions per unit of primary energy consumption, will decrease in both OECD and non-OECD countries through 2050. A region’s fuel mix largely determines its carbon intensity, and our projection of carbon intensity decreases around the world as use of renewable energy grows and use of coal is reduced in many countries. We project average aggregate carbon intensity in non-OECD countries to be higher than in the OECD over the next 30 years because non-OECD countries will likely continue to use primarily fossil fuel-fired generation to support their more rapid economic growth over this time.

We also project that energy intensity, the energy consumed per dollar of GDP, will decline globally through 2050. Driven by technology and shifts away from energy-intensive industries in many economies, increased energy efficiency results in lower energy intensity. In the non-OECD region, economic growth results in a faster decline of energy intensity than in the OECD region. By 2050, the energy intensity of OECD and non-OECD countries becomes more similar as some non-OECD countries increase their share of less energy-intensive industries and their technology use becomes more similar to OECD countries.

Emissions-related policies also influence projections in energy-related CO2 emissions. Required efficiency, fuel, and technology goals are generally more prevalent in OECD countries, contributing to the relatively slower growth in emissions for the OECD relative to the non-OECD countries.

For more information on our projections of international energy-related CO2 emissions, refer to our International Energy Outlook 2021.

-----

Earlier:

2021, October, 19, 12:35:00

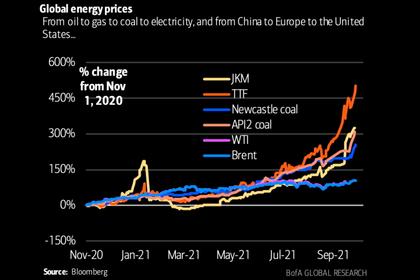

GLOBAL ENERGY PRICES UP

Several factors are fuelling this price surge in energy commodities – primary among them is energy demand having rebounded as economies get back to business and consumers return to pre-pandemic levels of economic activity.

2021, October, 18, 12:40:00

ВОССТАНОВЛЕНИЕ НЕФТЯНОГО РЫНКА

«Нефтяной рынок восстанавливается последовательно. Мы видим, что в 2021 году общий рост спроса составит 6 млн баррелей, а к концу года мы надеемся на полное восстановление спроса»,

2021, October, 15, 09:35:00

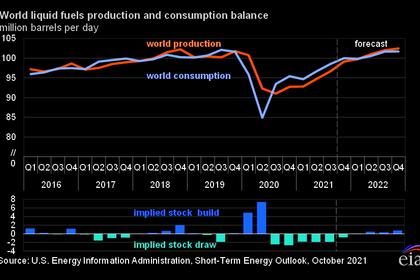

GLOBAL OIL DEMAND WILL UP BY 5.8 MBD

World oil demand is estimated to increase by 5.8 mb/d in 2021, revised down from 5.96 mb/d in the previous month’s assessment.

2021, October, 13, 12:15:00

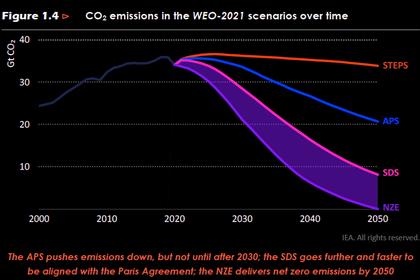

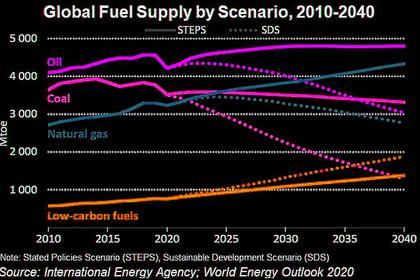

GLOBAL ELECTRICITY DEMAND NEARLY DOUBLES TO 2050

This scenario also sees an accelerating pace of change in the power sector, sufficient to realise a gradual decline in the sector’s emissions even as global electricity demand nearly doubles to 2050.

2021, October, 13, 12:10:00

GLOBAL ECONOMY GROWTH 2021-22: 5.9% - 4.9%

The global economy is projected to grow 5.9 percent in 2021 and 4.9 percent in 2022

2021, October, 11, 11:50:00

GLOBAL ENERGY CONSUMPTION WILL UP BY 50%

Global energy consumption will increase nearly 50% over the next 30 years.

2021, July, 5, 13:25:00

GLOBAL GAS DEMAND UP

“Natural gas demand is set to rebound strongly in 2021 and will keep rising further if governments do not implement strong policies to move the world onto a path towards net-zero emissions by mid-century,” the IEA said in its latest gas outlook.