2021-10-15 09:35:00

GLOBAL OIL DEMAND WILL UP BY 5.8 MBD

OPEC - 13 October 2021 - OPEC Monthly Oil Market Report

Oil Market Highlights

Crude Oil Price Movements

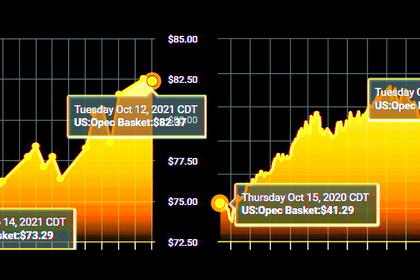

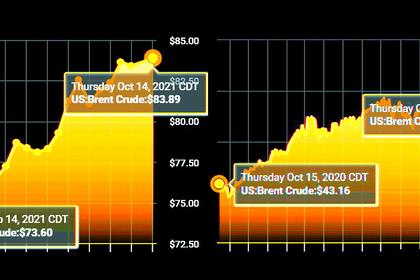

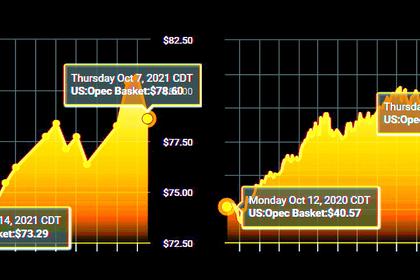

Crude oil prices rebounded m-o-m in September, gaining about 5%, supported by robust oil market fundamentals amid a slow restart of US oil production, further recovery of oil demand and a drop in inventories, along with easing COVID-19-related mobility restrictions in several Asian countries. Moreover, worries about natural gas and coal shortages in Europe and Asia boosted sentiment for higher oil demand. The OPEC Reference Basket (ORB) value rose by $3.55 or 5.0% m-o-m in September to settle at $73.88/b. Year-to-date (y-t-d), the ORB was up by $26.21, or 64.5%, to average $66.83/b compared with the same period last year. The ICE Brent front-month rose $4.37, or 6.2%, m-o-m in September to average $74.88/b, while NYMEX WTI increased by $3.83, or 5.7%, m-o-m to average $71.54/b. Consequently, the Brent/WTI spread widened further in September to $3.34/b, its highest point since last April. The market structure of all three major oil benchmarks – Brent, WTI and Dubai – remained in backwardation. However, the Brent forward curve strengthened, while WTI and Dubai backwardation flattened slightly. Hedge funds and other money managers boosted bullish wagers in September as oil prices rose to multi-year highs, as the risk of a natural gas and coal shortage urged speculators to bet on higher oil prices.

World Economy

Global economic growth forecasts for both 2021 and 2022 remain unchanged from the last month’s assessment at 5.6% and 4.2%, respectively. Given somewhat slowing 3Q21 momentum, the US economy forecast for 2021 is revised down slightly to 5.8% from 6.1%, while the forecast for 2022 remains unchanged at 4.1%. Euro-zone economic growth is revised up to 5% from 4.7% for 2021 and to 3.9% from 3.8% for 2022, after a strong rebound in 2Q21. The forecast for Japan is revised down to 2.6% from 2.8% for 2021, due to ongoing COVID-19-related social-distancing measures in 3Q21, while the forecast for 2022 remains at 2%. After a strong recovery in the first half of the year, China’s economy is seen to slow somewhat, leaving the growth forecast at 8.3% in 2021 and 5.8% in 2022, representing a 0.2 percentage point downward revision for both years. Meanwhile, India’s 2021 growth forecast is unchanged at 9% for 2021 and 6.8% for 2022, although downside risks prevail. Russia’s forecasts are revised up from 3.5% to 4% for 2021 and from 2.5% to 2.7% for 2022, benefitting from the more stable oil market. Brazil’s growth forecast remains unchanged for both 2021 and 2022 at 4.7% and 2.5%, respectively. The ongoing robust growth in the world economy continues to be challenged by uncertainties, such as the spread of COVID-19 variants and the pace of vaccine rollouts worldwide, as well as ongoing global supply-chain disruptions. Additionally, sovereign debt levels in many regions, together with rising inflationary pressures and potential central bank responses, remain key factors requiring close monitoring.

World Oil Demand

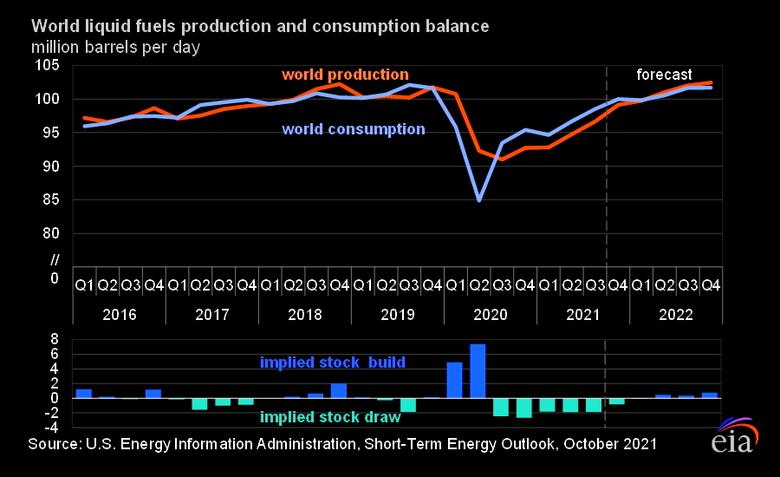

World oil demand is estimated to increase by 5.8 mb/d in 2021, revised down from 5.96 mb/d in the previous month’s assessment. The downward revision is mainly driven by lower-than-expected actual data for the first three quarters of this year, despite healthy oil demand assumptions going into the final quarter of the year, which will be supported by seasonal uptick in petrochemical and heating fuel demand and the potential switch from natural gas to petroleum products due to high gas prices. Both OECD and non-OECD figures are adjusted lower, with the downward revision in OECD regions focused in 1H21, while the non-OECD revision is concentrated in 3Q21.The world is expected to consume 96.6 mb/d of petroleum products this year. For 2022, world oil demand growth is unchanged at 4.2 mb/d. As a result, global demand next year is seen averaging 100.8 mb/d. Demand is anticipated to be supported by healthy economic momentum in the main consuming countries and better management of the COVID-19 pandemic.

World Oil Supply

Non-OPEC liquids supply growth in 2021 is revised down by 0.3 mb/d from the previous month’s assessment to now stand at 0.7 mb/d. The revisions were driven mainly by a downward adjustment in 3Q21 due to factors such as production outages in the US Gulf of Mexico caused by Hurricane Ida; maintenance in the Tengiz field in Kazakhstan; and a force majeure in Canada at the Suncor oil sands site. The impact of the Hurricane led to a downward revision in US liquids supply in 2021 from growth of 0.1 mb/d to a contraction of 0.1 mb/d. The main growth drivers for 2021 supply growth continue to be Canada, Russia, China, Norway and Brazil. Similarly, the non-OPEC supply growth forecast for 2022 is revised up by 0.1 mb/d due to the base change to now stand at 3.0 mb/d. Russia and the US are expected to be the main drivers, followed by Brazil, Norway, Canada, Kazakhstan, Guyana, and other countries in the DoC. OPEC NGLs are forecast to grow by 0.1 mb/d in both 2021 and 2022 to average 5.2 mb/d and 5.3 mb/d, respectively. OPEC crude oil production in September increased by 0.49 mb/d m-o-m, to average 27.33 mb/d, according to available secondary sources.

Product Markets and Refining Operations

Refinery margins further extended their upward trend in September globally, with solid support coming from the middle of the barrel. The tightness in product balance caused by supply side constraints in previous months was exacerbated by the start of peak refinery maintenance season amid lower product exports from China. Middle distillates were the main margin driver in all regions, while in Asia this upside was outpaced by robust fuel oil performance. Meanwhile, gasoline markets weakened as their crack spreads stepped down from post-pandemic highs registered the previous month, due to a less optimistic demand outlook as peak driving season approached its end.

Tanker Market

Dirty tanker rates remained soft in September amid a continued imbalance between tonnage supply and demand, keeping rates at low or even loss-making levels. Meanwhile, some positive signs are emerging for the final quarter of the year, as loading schedules should see a 20% increase in waterborne Russian exports and 10% increase in North Sea flows, amid ongoing planned upward adjustments in OPEC production. However, a sustained recovery in the tanker market could take as long as 12 months to materialize to allow for a return in demand from emerging and developing markets and sufficient scrapping to reduce the overhang in tonnage availability.

Crude and Refined Products Trade

Preliminary data shows US crude imports in September recovering from a slight dip the month before to average a healthy 6.4 mb/d, while US crude exports averaged 2.6 mb/d in September, continuing an alternating pattern of rises and dips, this time on the lower side. After four months of relatively muted levels, China’s crude imports jumped to 10.5 mb/d in August, pushed higher by the arrival of storm-delayed cargoes, although policy-led uncertainties continued to impact China’s trade flows. India’s crude imports finally saw a recovery, after following a general downward trend since December 2020, to average 4.1 mb/d in August. Tanker tracking data show India’s crude imports remaining steady in September. Japan’s crude imports continued to recover from low levels, reaching their highest point since April 2020 at 2.7 mb/d in August. The country’s crude and product imports are expected to see a boost from demand in the power sector for fuel oil as well as crude for direct burning, amid reports of a restart of oil-fired power units.

Commercial Stock Movements

Preliminary August 2021 data showed that total OECD commercial oil stocks fell by 19.5 mb m-o-m to stand at 2,855 mb. This was 363 mb lower than the same time one year ago, 183 less than the latest five-year average and 131 mb below the 2015-2019 average. Within components, OECD commercial crude stocks fell by 23.0 mb m-o-m in August, ending the month at 1,362 mb. This was down by 102 mb compared with the latest five-year average, and 87 mb below the 2015-2019 average. By contrast, OECD total product inventories rose by 3.2 mb m-o-m in August to stand at 1,493 mb. This was 81 mb lower than the latest five-year average and 43 mb below the 2015-2019 average. In terms of days of forward cover, OECD commercial stocks fell by 0.1 days m-o-m in August to stand at 62.5 days. This was 12.3 days lower than the same period in 2020, 2.5 days below the latest five-year average and 0.3 days below the 2015-2019 average.

Balance of Supply and Demand

Demand for OPEC crude in 2021 is revised up by 0.1 mb/d from the previous month’s assessment to stand at 27.8 mb/d, around 5.0 mb/d higher than in 2020. Demand for OPEC crude in 2022 was also revised up by 0.1 mb/d from the previous month’s assessment to stand at 28.8 mb/d, around 1.0 mb/d higher than in 2021.

-----

Earlier:

2021, October, 14, 13:35:00

OIL PRICE: NEAR $84 AGAIN

Brent gained 67 cents, or 0.8%, to $83.85 a barrel. WTI climbed 62 cents, or 0.8%, to $81.06 a barrel.

2021, October, 14, 13:30:00

СБАЛАНСИРОВАННЫЕ РЕШЕНИЯ РОССИИ

Что касается наших усилий по стабилизации мирового энергетического рынка, то да, у нас всё это происходит в довольно жёстком режиме: мы спорим друг с другом, отстаиваем свои позиции, но находим, до сих пор находили сбалансированные, приемлемые для всех сторон решения.

2021, October, 14, 13:25:00

ГЛОБАЛЬНАЯ ЭНЕРГЕТИКА РОССИИ

Заместитель Председателя Правительства Российской Федерации Александр Новак принял участие в первом дне международного форума «Российская энергетическая неделя»

2021, October, 14, 13:00:00

OPEC + RUSSIA 400 TBD

The OPEC+ alliance has agreed to increase production by 400,000 b/d through the end of 2022, aiming to eliminate the historic cuts it implemented through the pandemic by late in the year

2021, October, 14, 12:55:00

OIL PRICES 2021-22: $81-$72

We expect Brent prices will remain near current levels for the remainder of 2021, averaging $81/b during the fourth quarter of 2021. In 2022, we expect that growth in production from OPEC+, U.S. tight oil, and other non-OPEC countries will outpace slowing growth in global oil consumption and contribute to Brent prices declining from current levels to an annual average of $72/b.

2021, October, 11, 12:00:00

ОПЕК+ РОССИЯ: 119%

В августе исполнение соглашения ОПЕК+ вышло на рекордный за всё время кооперации стран ОПЕК и не-ОПЕК уровень в 119%.

2021, October, 11, 11:50:00

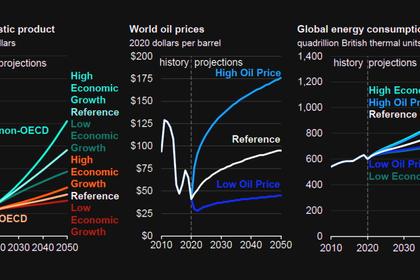

GLOBAL ENERGY CONSUMPTION WILL UP BY 50%

Global energy consumption will increase nearly 50% over the next 30 years.