2021-02-10 11:55:00

OIL PRICES 2021-22: $52-$56

U.S. EIA - February 9, 2021 - SHORT-TERM ENERGY OUTLOOK

Forecast highlights

Global liquid fuels

• The February Short-Term Energy Outlook (STEO) remains subject to heightened levels of uncertainty because responses to COVID-19 continue to evolve. Reduced economic activity related to the COVID-19 pandemic has caused changes in energy demand and supply over the past year and will continue to affect these patterns in the future. U.S. gross domestic product (GDP) declined by 3.6% in 2020 from 2019 levels. This STEO assumes U.S. GDP will grow by 3.8% in 2021 and by 4.2% in 2022. The U.S. macroeconomic assumptions in this outlook are based on forecasts by IHS Markit.

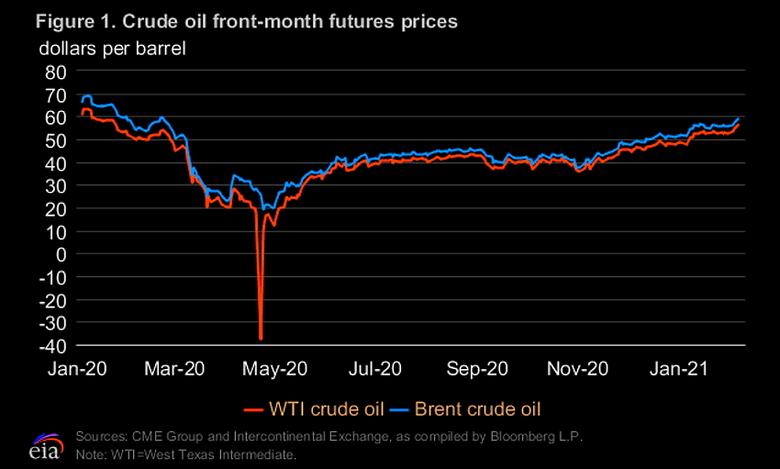

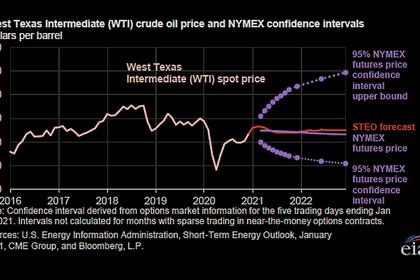

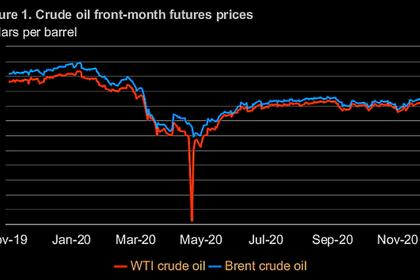

• Brent crude oil spot prices averaged $55 per barrel (b) in January, up $5/b from the December average but $9/b lower than the average in January of last year. Higher Brent prices in January largely reflected the January 5 announcement by Saudi Arabia that it would unilaterally cut 1.0 million barrels per day (b/d) of crude oil production in February and March, in addition to the reduced production levels on which the Organization of the Petroleum Exporting Countries (OPEC) and partner countries (OPEC+) previously agreed. The U.S. Energy Information Administration (EIA) expects Brent crude oil prices will average $56/b in the first quarter of 2021 and $52/b over the remainder of the year. EIA expects lower oil prices later in 2021 as a result of rising oil supply that will slow the pace of global oil inventory withdrawals. EIA also expects that high global oil inventory levels and spare production capacity will limit upward price pressures. EIA expects Brent prices will average $55/b in 2022.

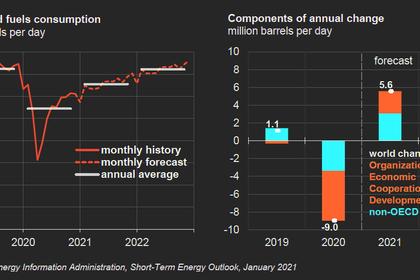

• EIA estimates that the world consumed 93.9 million b/d of petroleum and liquid fuels in January, which is down 2.8 million b/d from January 2020. EIA forecasts that global consumption of petroleum and liquid fuels will average 97.7 million b/d for all of 2021, which is up by 5.4 million b/d from 2020. EIA forecasts that consumption of petroleum and liquid fuel will increase by 3.5 million b/d in 2022 to average 101.2 million b/d.

• EIA estimates that U.S. crude oil production averaged 11.0 million b/d in January, which is down slightly from 11.1 million b/d in November (the most recent month for which historical data are available). EIA expects production will continue to decline slightly in the coming months, reaching 10.9 million b/d in June. Although oil-directed drilling has increased in the United States in recent months, the number of active drilling rigs remains lower than year-ago levels. EIA expects production from newly drilled wells will be more than offset by declining production rates at existing wells in the first half of 2021. However, based on EIA’s forecast that West Texas Intermediate crude oil prices will remain near or higher than $50/b during the forecast period, EIA expects drilling will continue to increase. As a result, production from new wells will exceed the declines from legacy wells, and overall crude oil production will increase in the second half of 2021 and in 2022. EIA estimates that U.S. crude oil production will average 11.0 million b/d in 2021—down from 11.3 million b/d in 2020 and 12.2 million b/d in 2019—and will rise to 11.5 million b/d in 2022.

• U.S. regular gasoline retail prices averaged $2.33 per gallon (gal) in January, compared with an average of $2.20/gal in December and $2.55/gal in January 2020. EIA forecasts gasoline prices to average $2.44/gal in 2021 and $2.46/gal in 2022. U.S. diesel fuel prices averaged $2.68/gal in January compared with $2.58/gal in December and $3.05/gal in January 2020, and EIA forecasts it will average $2.70/gal in 2021 and $2.77/gal in 2022.

• On a volume basis, U.S. consumption of gasoline declined by more than other petroleum products in 2020. EIA forecasts that U.S. gasoline consumption will rise in the forecast but remain lower than 2019 levels. U.S. gasoline consumption is forecast to average 8.6 million b/d in 2021 and 8.9 million b/d in 2022, up from 8.0 million b/d in 2020 but lower than the 9.3 million b/d consumed in 2019.

Natural Gas

• EIA expects that total U.S. consumption of natural gas will average 81.7 billion cubic feet per day (Bcf/d) in 2021, down 1.9% from 2020. The decline in total U.S. consumption reflects less natural gas consumed for electric power as a result of higher natural gas prices compared with last year. In 2021, EIA expects residential natural gas demand to average 12.9 Bcf/d (up 0.2 Bcf/d from 2020) and commercial demand to average 9.1 Bcf/d (up 0.6 Bcf/d from 2020). EIA forecasts industrial consumption will average 23.0 Bcf/d in 2021 (up 0.4 Bcf/d from 2020) as a result of increased manufacturing activity amid a recovering economy. Industrial consumption of 23.0 Bcf/d would be 0.1 Bcf/d below the 2019 level. EIA expects total U.S. natural gas consumption will average 81.0 Bcf/d in 2022.

• In January, the Henry Hub natural gas spot price averaged $2.71 per million British thermal units (MMBtu), up from the December average of $2.59/MMBtu. EIA expects Henry Hub spot prices to reach a monthly average of $2.98/MMBtu in February 2021. Higher expected prices in February reflect expectations of continued strong liquefied natural gas (LNG) exports and a shrinking surplus of natural gas in storage compared with the five-year (2016– 20) average. EIA uses weather forecasts from the National Oceanic and Atmospheric Administration (NOAA) as an input into the STEO, and the NOAA forecast in this STEO is from late January. More recent forecasts for mid-February weather show cold temperatures could extend across much of the United States, which creates an upside risk to near-term prices in this outlook. EIA expects that Henry Hub spot prices will average $2.95/MMBtu in 2021, which is up from the 2020 average of $2.03/MMBtu. EIA expects that continued growth in LNG exports and in domestic natural gas consumption outside of the electric power sector, as production remains relatively flat, will contribute to Henry Hub spot prices rising to an average of $3.27/MMBtu in 2022.

• U.S. working natural gas in storage ended October at more than 3.9 trillion cubic feet (Tcf), 5% more than the 2015–19 average and the fourth-highest end-of-October level on record. EIA estimates that inventory withdrawals were 703 billion cubic feet (Bcf) in January, compared with a five-year (2016–20) average January withdrawal of 716 Bcf. The January withdrawals occurred at a lower rate than EIA forecast in last month’s STEO. The lowerthan- expected withdrawal is the result of warmer-than-average January temperatures that reduced natural gas use for space heating. However, EIA forecasts that declines in U.S. natural gas production this winter compared with last winter will more than offset the declines in natural gas consumption, which will contribute to natural gas storage returning to levels near the five-year average by the end of winter. Forecast natural gas inventories end March 2021 at 1.8 Tcf, which is about the same as the five-year average.

• EIA forecasts that U.S. production of dry natural gas will average 90.5 Bcf/d in 2021 and 91.0 Bcf/d in 2022, which are down from an average of 91.3 Bcf/d in 2020 and 93.1 Bcf/d in 2019. In the forecast, dry natural gas production remains relatively flat, averaging between 89.8 Bcf/d and 91.0 Bcf/d in every month from February 2021 through July 2022. Flat natural gas production is the result of falling production in several of the smaller natural gas producing regions being offset by growth in other regions, most notably in the Appalachia and Haynesville regions. EIA estimates that the United States exported 9.8 Bcf/d of LNG in January amid high spot natural gas prices in Asia. However, foggy conditions and high winds affected export operations at Sabine Pass LNG, Corpus Christi LNG, and Cameron LNG, leading to several weather-related closures and sporadic suspension of piloting services on several days in January. EIA forecasts that U.S. LNG exports will average 8.5 Bcf/d in 2021. In 2022, EIA forecasts LNG exports will average 9.2 Bcf/d, surpassing the amount of natural gas exported via pipeline for the first time.

Electricity, coal, renewables, and emissions

• EIA forecasts that consumption of electricity in the United States will increase by 1.6% in 2021 after falling 3.8% in 2020. EIA forecasts residential sector retail sales will grow by 2.2% in 2021. The increase is primarily a result of colder forecast temperatures in the first quarter of 2021 compared with the same period in 2020, which EIA expects will raise demand for space heating, along with EIA’s assumption that more people will be working from home than in the first quarter of 2020. EIA expects retail sales of electricity in the commercial and industrial sectors will increase by 1.2% and 2.3%, respectively. For 2022, EIA forecasts total electricity consumption will grow by another 1.7%. EIA expects the share of U.S. electric power generated with natural gas to fall from 39% in 2020 to 37% in 2021 and to 35% in 2022. The forecast natural gas share declines in response to a forecast increase in the price of natural gas delivered to electricity generators from an average of $2.38/MMBtu in 2020 to $3.27/MMBtu in 2021 (a 37% increase). Coal’s forecast share of electricity generation rises from 20% in 2020 to 21% in 2021 and to 22% in 2022. Electricity generation from renewable energy sources rises from 20% in 2020 to 21% in 2021 and to 23% in 2022. The nuclear share of U.S. generation declines from 21% in 2020 to 20% in 2021 and to 19% in 2022.

• EIA forecasts that planned additions to U.S. wind and solar generating capacity in 2021 and 2022 will contribute to increasing electricity generation from those sources. EIA estimates that the U.S. electric power sector added 17.5 gigawatts (GW) of new wind capacity in 2020. EIA expects 15.3 GW of wind capacity will be added in 2021 and 3.6 GW in 2022. Utility-scale solar capacity rose by an estimated 11.1 GW in 2020. The forecast for added utility-scale solar capacity is 16.2 GW for 2021 and 12.3 GW for 2022.

• EIA expects U.S. coal production to total 589 MMst in 2021, 50 MMst (9%) more than in 2020. In 2022, EIA expects coal production to rise by a further 5 MMst (1%). These increases reflect higher forecast demand for coal in the electric power sector because of rising natural gas prices, which increases coal’s competitiveness relative to natural gas for power generation dispatch. Although EIA expects coal production to rise in 2022, expected production increases will be limited by strong inventory draws. EIA expects significant coal supply to the power sector will come from a reduction in inventory levels in 2022, as the power sector brings inventory levels back in line with historical averages. Coal production in the forecast will also be limited by declining production capacity, as high mine reclamation costs have contributed to mine divestments and closings that may counter the effects of higher coal demand.

• EIA expects rising global economic activity will contribute to rising steel production and power demand, which will lead to increased U.S. exports of both metallurgical and steam coal. EIA forecasts coal exports will total 85 MMst in 2021, up by 24% from 2020, which was the lowest level since 2016. EIA forecasts exports will rise by 6 MMst in 2022 to 91 MMst.

• EIA estimates that U.S. energy-related carbon dioxide (CO2) emissions decreased by 11% in 2020. This decline in emissions is the result of less energy consumption related to economic contraction in response to the COVID-19 pandemic. In 2021, EIA forecasts that energyrelated CO2 emissions will increase by about 4% from the 2020 level as economic activity increases leading to rising energy use. Energy-related CO2 emissions are also expected to rise by 3% in 2022 as economic growth continues.

-----

Earlier:

2021, February, 9, 15:45:00

OPEC+ OIL PRODUCTION UP 440 TBD

OPEC's 13 members pumped 25.70 million b/d in the month, up 270,000 b/d from December, while their nine non-OPEC partners, led by Russia, produced 12.91 million b/d, a rise of 170,000 b/d,

2021, February, 8, 12:55:00

OIL PRICE: NEAR $60

Brent touched an intraday high of $60.06 a barrel. WTI advanced 60 cents, or 1.1%, to $57.45 a barrel.

2021, February, 5, 12:40:00

OIL REMAINS THE FUEL

Petroleum remains the most-consumed fuel in the United States, as energy-related carbon dioxide emissions dip through 2035 before climbing in later years.

2021, February, 4, 16:35:00

OIL MARKET WILL BE GOOD: 2021

The global economy is forecast to grow by 4.4 per cent in 2021, a substantial shift from -4.1 per cent last year. “With the crude oil market currently switching into backwardation, we are hopeful that 2021 will be a good year for overall demand,” Barkindo said.

2021, January, 22, 11:35:00

OIL PRICES 2021-22: $50-$55

The price of Brent crude oil to increase from its December 2020 average of $50 per barrel (b) to an average of $56/b in the first quarter of 2021. The Brent price is then expected to average between $51/b and $54/b on a quarterly basis through 2022.

2021, January, 13, 13:50:00

OIL PRICES 2021-22: $53

Brent crude oil spot prices to average $53 per barrel (b) in both 2021 and 2022 compared with an average of $42/b in 2020.

2020, December, 9, 11:45:00

OIL PRICES 2021: $47 - $50

Brent prices will average $49/b in 2021, up from an expected average of $43/b in the fourth quarter of 2020. Brent prices will average $47/b in the first quarter of 2021 and rise to an average of $50/b by the fourth quarter.