2021-03-29 13:05:00

INDIA'S ENERGY CHANGES

By A. K. Shyam, PhD Assessor National Accreditation Board for Education & Training (NABET

ENERGYCENTRAL - Mar 23, 2021 - Background:

Energy has been considered backbone of sound economic development of any country for many reasons known to everyone. Every country passes through different phases of development and even today, no country can match the other as the preferences and options have been different for different countries, depending upon the resources. Developed countries seem to have an edge in this regard due to their affordability to latest technologies compared to developing and underdeveloped nations. However, climate change which is not specific to any country has brought them together in sharing and shouldering responsibilities to fight impact together. The annual global meet on climate change sets the trend for future and responsibility to each of the countries party to the negotiations. Unfortunately, pandemic of 2019 seems to have shaken every country and the agenda on climate change understandably needs re-consideration of the decisions made during the Paris meet.

It is in the light of the current scenario that every country needs to reorient itself to address appropriate strategies to combat the post pandemic demands on Energy.

Indian Scenario

India, world’s largest producer and third largest consumer of electricity has grown significantly since independence both in installed capacity and Transmission & Distribution (T & D). National grid in India has an installed capacity of 375.32 GW as on Dec. 2020 with renewable contribution (including large hydroelectric) constituting 36.17% of the installed capacity.

Effective policy implementation in India facilitated around 750 million people to gain access to electricity between 2000 and 2019. This has indirectly impacted in the reduction of biomass in cooking and consequent indoor air pollution especially affecting women and children.

The institutional framework in India attracts investments for its growing energy needs - private sector investments are allowed in coal mining, open up oil and gas retail markets. Functioning energy markets seem to ensure economic efficiency in coal, gas and power sectors helping to achieve energy security and supporting economic growth.

It is also necessary to ensure financial health of power sector dealing with surplus capacity, low utilisation of coal and natural gas and increasing shares of variable renewable energy. Creation of competitive wholesale power market is vital in improving the utilisation of generation capacity. Single National power system and major investments in thermal and renewable capacity has improved markedly.

It has also been realized through international experience, that a diverse mix of flexibility, investments provide successful system integration of wind and solar PV.

- Energy Security a priority:

Coal continues to be the largest source of energy with increased coal supply since early 2000. Combined with stringent air pollution regulations, coal power plants are aiming at greater efficiency along with relatively lower emissions. This is necessitated for steel, cement and fertiliser development.

India happens to be world’s third largest consumer of oil but, fourth largest oil refiner and exporter of refined products. India could become an attractive market for refinery investment since its oil consumption in mid-2020’s is likely to surpass China. In view of this, ambitious long-term road map to expand refining capacity in tune with projected demand through 2040. India’s import (above 80% in 2018) is projected to increase significantly in the coming decades.

India has been meticulously prioritising a reduction on imports by increasing firstly, on domestic upstream activities, secondly, diversifying sources of supply and increasing investments in overseas oil fields of Middle East and Africa. Promoting domestic production, the Hydrocarbon Exploration and Licencing Policy (HELP) and is building up dedicated emergency oil stocks. Strategically, the reserve capacity of 40 million barrels can cover just about 10 days of current net imports – the same lasts just four days of net imports in 2040.

Similarly, the share of natural gas in the energy mix is being increased to 15% by 2030 from a mere 6% today. The country is aiming to increase domestic gas production – currently; there are five operating terminals which may result in 11 additional terminals with the projects under construction.

- Progress in Sustainable Development:

India has a keen eye on Goal 7 (delivering energy access) of United Nations Sustainable Development goals and has made important progress. India’s per capita emission of 1.6 tonnes of Carbon dioxide is well below global average of 4.4 tonnes. Nationally Determined Contribution under the Paris Agreement facilitates emission reduction and increase share of non-fossil fuels in the power generation capacity. Increased forest/tree cover further supplement acting as carbon sink. Energy efficiency has helped avoid 15% of additional annual energy demand and 300 million tonnes of carbon dioxide emissions over a period of 18 years (2000 to 2018).

Electricity demand seems to be tripling due to increased appliance ownership and cooling needs and without significant energy efficiency improvements, India may have to add massive power generation capacity. But, raising energy efficiency would save about 190$ US billion per year by 2040 and avoid 875 terawatt hours per year – almost half of India’s current annual power generation.

India’s investment in solar PV was greater than all fossil fuel sources of electricity generation in 2018 due to large scale auctions to swift renewable energy due to rapid decrease in price. India had 84 GW Grid connected renewable capacity compared to 366 GW in 2019. India is now aiming at 175 GW of renewable by 2022 – eventually mounting to 450 GW as announced by Prime Minister. This would warrant unlocking the flexibility for effective system integration. The design of renewable auctions with clear criteria , location and system value along with grid expansion and demand side response would go a long way in achieving this goal.

The environment related aspects of air, water and land are being addressed since the 1980s. Reducing health impacts due to air pollution being a key priority, rules have been strengthened through adoption of National Clean Air Programme (NCAP) responsible for monitoring and enforcement of stringent standards for air.

Climate change presents growing water stress, storms, floods and other extreme weather events and adoption to such extremes would warrant political priority. The water requirement towards growing energy needs is pretty crucial for the anticipated growth.

- Technology and Innovation:

National priorities like, ‘Make in India’ promotes manufacturing innovations – even attracts global companies to produce solar PV, Lithum batteries, solar charging infrastructure and related advanced technologies especially in energy including cooling, electric mobility, smart grids and biofuels.

Climate policy agenda drives mission based approach in policy areas – solar, water and energy. Clean energy seems to be attracting research and development funding spread widely across government and public sector companies.

Energy data and policy governance:

It is the integration of several ministries that promotes an appropriate national energy policy – develop framework for long term energy agenda. While these are essential, energy data, monitoring, reviewing progress and enforcing implementation of energy policies are more crucial in not only appropriate action but even improve dissemination.

Establish, permanent energy policy co-ordination in the central government, with an Overarching national energy policy framework to support the development of a secure, Sustainable and affordable energy system.

- Continue to encourage investment in India’s energy sector :

- Prioritise actions to foster greater energy security by:

- strengthening the resilience of India’s energy infrastructure, based on a robust analysis of the Water–energy nexus and cooling demand, notably when planning future investment.

- Adopt a co-ordinated cross-government strategy for energy R&D, which enables impact-oriented Measurement and dissemination of results.

- Ensure India’s international energy collaboration to be strong and mutually beneficial, Highlighting the country’s energy successes and supporting continued opportunities to learn from International best practices.

India, being the second most populous country, has strong economic performance in recent decades in reducing poverty level, greater energy access and penetration of cleaner energy. The sustained economic growth places enormous demand on its energy sources/systems and infrastructure. About 45% of land area being agriculture, 24% forest barring exceptions of deserts in the west and Himalayan Mountains in north, population density is indeed high throughout the country.

Challenges in post pandemic period:

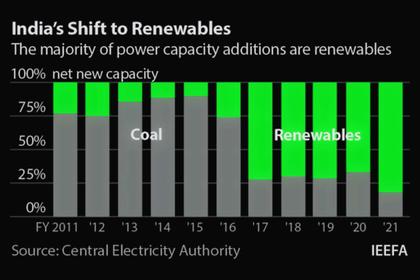

Coal fired electricity generation in India fell 5% in 2020 due to significantly reduced electricity demand due to Covid-19 lockdown. This is the second consecutive year since reaching peak in 2018. However, coal still dominated as source of power generation accounting for 71% of power in the last year. But, India needs to make some serious strategic changes in the post covid decade to make or break from coal to clean electricity transition.

Coal fell by 51 terawatt hours (TWh-2020) caused by 36 TWh (3%) fall in electricity demand and 12 TWh (3%) rise in solar generation. Consequently, plant load factor (PLF) fell to a recor low of 53% in 2020. However, growth of 4-5% electricity annual demand growth until 2030, it is estimated that there would be small (52 TWh) increase in coal fired power generation. It is projected that the coal power could fall even in India pursues higher economic growth rate. Despite aiming at climate-friendly pathway, it depends on 2022 target for both wind and solar generation – combined generation of which stood at 118 TWh in 2020 which is short of the aimed target of 274 TWh in 2021-2022 and 793 TWh for 2029-2030.

- Largest power demand increase of any country over next 20 years

India is likely to experience largest increase in power demand over the next 20 years and thus calls for policies and investment to accelerate towards clean energy transition. Similar to other countries, ensuring affordable clean and reliable energy being vital for future development, avoiding carbon intensive path followed earlier would warn strong policies, technological leap and surge in clean energy systems.

It is therefore a tremendous opportunity to discontinue high carbon pathway as quickly as possible in ensuring the desired ambition of fulfilling clean energy. An energy policy success so far is a positive indication in its ability to meet this challenge successfully.

Prime Minister’s announcement of 450 GW targets of renewables by 2030 is indeed a encouraging example of how clean energy could power growing economy. India’s down payment on clean energy transition promotes its pace to become global market leader in solar and storage by 2040.

It is already cheaper to build solar in India than anywhere else which is very good showing the urgency which is very important in confronting the crisis we all face today.

The blazes of Australia and California which are fresh in memories warn us on the need for quick solutions on the greatest crisis, the climate change. Many are concerned on the challenge to ‘Get to Zero’ as soon as possible. There has been a suggestion on “Green Premiums” in view of the storage batteries price dropping and becoming clear that solar and wind need be promoted. There is also a possibility that almost every country may reach 80% renewable by 2030.

As brought out earlier, Covid-19 has taught us many lessons and the most important one being on climate change. People fear that we may be talking ‘Climate Change’ in a decade hence similar to Covid-19 today. It is perhaps human to pay attention to meeting most immediate needs like, Covid-19 now. But, one needs to be serious about the dramatic high temperatures and its impact in the future. International Energy Agency (IEA) estimated a reduction of around 8% which meant that 47 billion tons of carbon equivalents will be released instead of 51 billion and if we can maintain this every year, we may perhaps be in a better shape.

In terms of cost – using a technology of $1 million to avert 10,000 tons of carbon emission would mean $100 per ton which is felt expensive. Taking mortality into consideration during Covid-19, more than 600,000 deaths worldwide, this will be 14 per 100,000. Comparing this with climate change – increase in global temperature within the next 40 years would account for the same. In case the emissions continue to stay, 73 extra deaths per 100,000 may be accounted while the figure may drop by 10% due to lower emissions.

It is thus evident that the lessons learnt globally due to Covid-19 need urgent actions on our part and some of them could be :

- Allow Science and Innovation to lead: Though ‘Zero emissions’ would be welcome, we know it is not possible through low rate either in flying or driving. Teleconferencing perhaps would help to a little extent which means, we will be using more energy and not less. We therefore need to 1. Find new tools to fight climate change 2. Produce electricity with less emission 3. Keep buildings cool and warm and finally, 4. Seeds of innovation. There is no single solution and we need to pool all that is possible carefully, in order to achieve the primary goal of lowering emissions, We’ll need biology, chemistry, physics, political science, economics, engineering, and other sciences in order to deal with this problem though climate science tells us why we need to deal with this problem.

- Make sure solutions work for poor countries:

Countries, responsible for the rise so far need to shoulder greater responsibility in curtailing emissions and in offering clean energy sources at a lower cost to poor countries. Governments, inventors and entrepreneurs around the world need to focus on green technologies affordable for poor countries.

- Start NOW:

A few countries have already started committing to funding and policies that help towards ‘Zero Emissions’. But, we not only need more to join but even speed up our actions.

Everyone realizes the urgency with which the world needs to gear up towards ‘Zero emission’ goal. It is also alarming that rising global temperatures would impact not only human life but even the natural ecosystems on which living has been possible so far. Therefore, COP 26 scheduled in Nov. 2021 in Glasgow, Scotland will be very crucial for proper direction towards the responsibility that global leaders need to shoulder on climate change. While COP 21 in Paris desired an initiative to double investment in research and development for clean energy, Covid-19 has now forced much more serious situation and quick action towards this objective, IF we wish to halt rising global temperatures.

Developed countries like USA & UK have greater responsibility to facilitate and make it easy for other countries in this noble task. Manufacturing sectors especially, cement and steel accounting for 31% need an urgency to decarbonize.

Manufacturing sector: (OPTIONAL)

Small and Medium sized Enterprises (SMEs) seem to have been neglected in the Green Manufacturing while their collective footprint amounts to major contribution. Energy saving and emission reduction are crucial even for SMEs. Environmental regulations coupled with public pressure and technological options have influenced industry worldwide to aim at environmentally conscious performance. Motivation is indeed a great character to switch to practices and rationale for a better environment. What is more important is to realize the several benefits of adopting green practices – financial benefit, company’s image, competitive advantage, customer/employee satisfaction are a few of them. Several companies in India have opted for Green Manufacturing – Suzlon Energy, ITC Limited, Tamilnadu Newsprint and Papers Limited, Wipro Technologies, HCL Technologies and Oil and Natural Gas company.

Car manufacturers as for example, SKODA have been aiming to become Green with their novel approaches in reducing carbon dioxide emissions. ‘Green Future’ strategy by SKODA seems to have been an integral part of its growth strategy 2018 and environmental strategy of Volkswagen Group. Octavia GreenLine with 86.0 mpg and Carbon dioxide emission of just 87 g/km will be the most fuel efficient. Recently launched Citigo CNG powered by natural gas enjoys carbon dioxide emission of just 79 g/kmIt offers 48 models with emissions of less than 120 g/km; 10 models with less than 100 g.km.

The facility has a new press line at the plant in Mlada Boleslav and claims that it requires 15% less energy than old facilities and is able to store energy not needed as well. Secondly, supply with heat and energy – brown coal used for heat and energy generation at this unit will be substituted with biomass in the form of wood pellets with an effective of about 45,000 tons of carbon reduction. GreenRetail led to removal of 95 tons of unusable or discarded materials from the storage areas of service partners – almost 90% of this could be reprocessed.

-----

This thought leadership article was originally shared with Energy Central's Clean Power Community Group. The communities are a place where professionals in the power industry can share, learn and connect in a collaborative environment. Join the Clean Power Community today and learn from others who work in the industry.

-----

Earlier:

2021, March, 18, 12:25:00

INDIA'S RENEWABLES 93 GW

India aims to achieve 175 GW of renewable capacity (excluding large hydropower) by 2022.

2021, February, 16, 11:55:00

INDIA'S HYDROPOWER UP

Hydropower accounts for 13% of India's total capacity, with 50 GW (2019). Over 93 GW of new hydropower projects are in various phases of development.

2021, February, 15, 13:50:00

INDIA'S ENERGY MARKET TRANSFORMATION

One of the key mitigation measures is development of adequate energy storage capacity in India.

2021, February, 15, 13:45:00

INDIA'S ENERGY TRANSITION RISK $9 BLN

This dramatic growth in renewable energy capacity reinforces the fact that India is witnessing an unprecedented energy transition to low-carbon development,

2021, February, 15, 13:40:00

INDIA'S ENERGY TRANSITION BUDGET 2021-22

Budget 2021-22 is a mixed bag in terms of support for India’s transition to a sustainable, low carbon economy.

2021, February, 9, 15:50:00

INDIA: GLOBAL ENERGY DRIVER

An expanding economy, population, urbanisation and industrialisation mean that India sees the largest increase in energy demand of any country, across all of our scenarios to 2040.

2021, February, 5, 12:35:00

INDIA OIL DEMAND WILL UP

"India's peak oil demand will be much later than what many analysts predict. So we will be seeing handsome demand numbers going into 2030s and 2040s, if not 2050s,"