2021-07-08 12:45:00

OIL PRICES 2021-22: $72-$67

U.S. EIA - July 7, 2021 - Short-Term Energy Outlook

Forecast highlights

Global liquid fuels

The July Short-Term Energy Outlook (STEO) remains subject to heightened levels of uncertainty related to the ongoing economic recovery from the COVID-19 pandemic. U.S. economic activity continues to rise after reaching multiyear lows in the second quarter of 2020 (2Q20). The increase in economic activity and easing of the COVID-19 pandemic have contributed to rising energy use. U.S. gross domestic product (GDP) declined by 3.5% in 2020 from 2019 levels. This STEO assumes U.S. GDP will grow by 7.4% in 2021 and by 5.0% in 2022. We based the U.S. macroeconomic assumptions in this outlook on forecasts by IHS Markit.

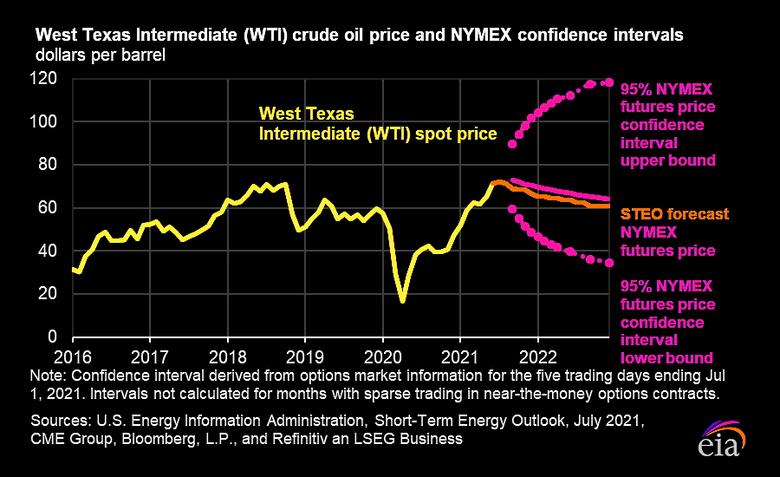

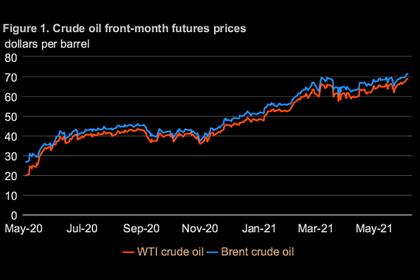

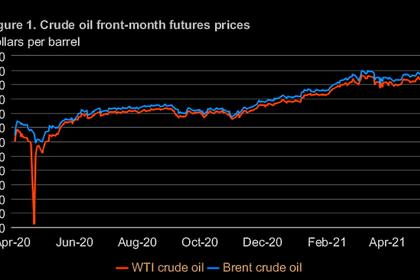

Brent crude oil spot prices averaged $73 per barrel (b) in June, up $5/b from May and $33/b higher than in June of last year. In the coming months, we expect that global oil production, largely from OPEC+ members (OPEC and partner nonmember countries), will increase by more than global oil consumption. We expect rising production will reduce the persistent global oil inventory draws that have occurred for much of the past year and keep prices similar to current levels, averaging $72/b during the second half of 2021 (2H21). However, in 2022, we expect that continuing growth in production from OPEC+ and accelerating growth in U.S. tight oil production, along with other supply growth, will outpace growth in global oil consumption and contribute to declining oil prices. Based on these factors, we expect Brent to average $67/b in 2022.

We estimate that global consumption of petroleum and liquid fuels averaged 92.3 million barrels per day (b/d) for all of 2020, down by 8.6 million b/d from 2019. We expect that global liquid fuels consumption will grow by 5.3 million b/d in 2021. In our forecast, global consumption of liquid fuels rises by an additional 3.7 million b/d in 2022 to 101.4 million b/d, which would surpass 2019 levels.

Based on our estimates, global liquid fuels inventories rose by 6.3 million b/d in 1H20 before declining at an average rate of 2.1 million b/d in 2H20 and 1H21. We forecast global inventories will continue to fall in the near term but at a slower rate, with global inventories falling by 0.2 million b/d in 2H21. We then expect inventories to rise by almost 0.5 million b/d in 2022.

U.S. regular gasoline retail prices averaged $2.78 per gallon (gal) in 1H21, compared with an average of $2.20/gal in 1H20. In June, monthly retail gasoline prices averaged $3.06/gal, the first time the monthly average was more than $3.00/gal since October 2014 (in nominal terms). We forecast regular-grade gasoline prices to average $2.92/gal in 2H21 and $2.74/gal for all of 2022.

U.S. liquid fuels consumption in 2020 averaged 18.1 million b/d, down 2.4 million b/d (12%) from 2019 consumption. We forecast U.S. liquid fuels consumption will rise to 19.6 million b/d in 2021 and then to 20.7 million b/d in 2022, which would surpass the 2019 level.

Natural Gas

Henry Hub natural gas spot prices averaged $2.03 per million British thermal units (MMBtu) in 2020. We expect Henry Hub prices will rise to an annual average of $3.22/MMBtu in 2021, and we forecast prices will then fall to an average of $3.00/MMBtu in 2022.

We expect U.S. dry natural gas production to average 92.6 billion cubic feet per day (Bcf/d) in 2021, up by 1.3% from 2020, and then rise to 94.7 Bcf/d in 2022.

U.S. natural gas consumption averaged 83.3 Bcf/d in 2020, down 2.2% from 2019. We expect that natural gas consumption will decline by 1.1% in 2021 and then grow by 0.7% in 2022. Most of the forecast decline in natural gas consumption this year is the result of less natural gas use in the electric power sector, which we expect to continue to decline because of rising natural gas prices.

U.S. working natural gas in storage ended the winter withdrawal season in March 2021 at 1.8 trillion cubic feet (Tcf), slightly less than the five-year (2016–20) average. We forecast that flat U.S. natural gas production this summer combined with record U.S. natural gas exports will contribute to slightly lower-than-average inventory builds during the remainder of the summer build season, which ends in October. Forecast natural gas inventories end October 2021 at 3.6 Tcf, which is 3% lower than the five-year average.

Electricity, coal, renewables, and emissions

We forecast that U.S. retail sales of electricity will increase by 2.8% in 2021 after falling by 3.9% in 2020. The largest forecast increase in electricity consumption occurs in the industrial sector, driven by rising levels of economic output. We forecast U.S. retail sales of electricity to the industrial sector will grow by 5.1% this year. Retail sales of electricity to the commercial sector also grow in the forecast, but they grow at the slightly slower pace of 2.1% in 2021 as some workers continue working from home instead of in office buildings. We forecast U.S. residential electricity sales will grow by 1.9% in 2021, as a result of colder temperatures in 1Q21 compared with 1Q20 and a hot start to the summer.

We expect the share of electric power generation produced by natural gas in the United States will average 36% in both 2021 and 2022, down from 39% in 2020. Our forecast for the natural gas share as a generation fuel declines because we expect a higher delivered natural gas price for electricity generators. Because we expect higher natural gas prices, we forecast coal’s generation share to rise from 20% in 2020 to 24% this year but to fall to 22% next year. New additions of solar and wind generating capacity support our expectation that the share of U.S. generation from these two energy sources will rise from 11% in 2020 to 15% by 2022. Extreme drought conditions in the West drive our expectation that the share of U.S. generation from hydropower will fall from 8% in 2020 to 6% in 2021 and 7% in 2022. The nuclear share of U.S. electricity generation declines from 21% in 2020 to 20% in 2021 and to 19% in 2022 as a result of retiring capacity at some nuclear power plants.

The U.S. retail electricity price for the residential sector in our forecast averages 13.6 cents per kilowatthour in 2021, which is 2.8% higher than the average retail price in 2020. Forecast residential prices increase by an additional 1.8% in 2022.

During the next 18 months, we expect electricity generation capacity from renewable energy sources to continue growing. Our forecast includes both wind and solar capacity growth, and solar capacity grows at a faster rate. Based on our survey data, large-scale solar capacity growth in gigawatts (GW) will exceed wind growth for the first time in 2022.

We expect U.S. coal production to total 617 million short tons (MMst) in 2021, which is 78 MMst (15%) more than in 2020. Rising electricity demand for coal amid higher natural gas prices is driving this production increase. In 2022, we expect coal production to fall by 7 MMst (1%).

We forecast that total energy-related carbon dioxide (CO2) emissions will increase by 7.1% in 2021 and by 1.5% in 2022 after declining by 11.1% in 2020. Even with growth over the next two years, forecast emissions in 2022 remain 3.3% lower than in 2019.

-----

Earlier:

2021, July, 7, 11:30:00

OIL PRICE: NEAR $75

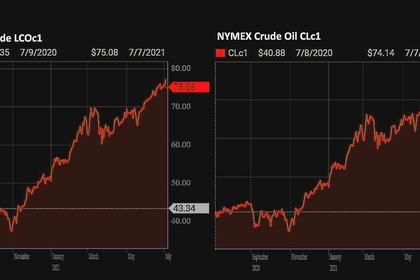

Brent was up 74cents, or 1%, at $75.27 a barrel , WTI was up 88 cents, or 1.2%, at $74.25 a barrel,

2021, June, 9, 12:50:00

OIL PRICES 2021-22: $68-60

EIA forecasts that Brent prices will remain near current levels in 3Q21, averaging $68/b., and $60/b in 2022.

2021, June, 8, 14:15:00

OIL PRICE: NEAR $71

Brent was down 35 cents, or 0.5%, at $71.14 a barrel, WTI was off by 32 cents, or 0.5%, at $68.91 a barrel,

2021, May, 12, 13:00:00

OIL PRICES 2021-22: $65-61

EIA forecasts that Brent prices will average $65/b in the second quarter of 2021, $61/b during the second half of 2021, and $61/b in 2022.

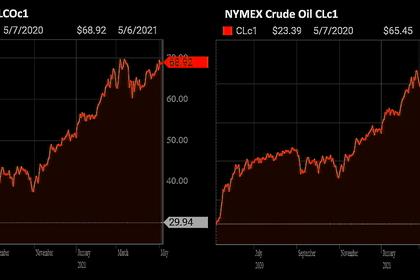

2021, May, 6, 13:40:00

OIL PRICE: NEAR $70 ANEW

Brent fell by 28 cents, or 0.4%, to $68.68 a barrel. WTI lost 31 cents, or 0.5%, to $65.32 a barrel.

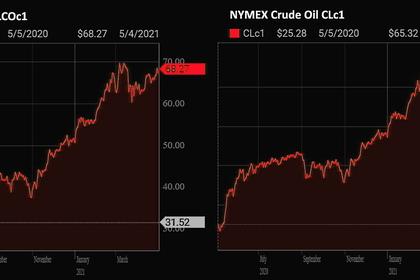

2021, May, 4, 12:40:46

OIL PRICE: ABOVE $68

Brent were 65 cents, or 0.96%, higher at $68.21 a barrel. WTI ticked up 62 cents, or 0.1%, to $65.11 a barrel.

2021, April, 20, 13:55:00

OIL PRICE: ABOVE $67 YET

Brent was up 64 cents, or 1%, at $67.69 a barrel. WTI gained 60 cents, or 1%, to $63.98.