2022-11-23 10:40:00

OIL PRICE: BRENT BELOW $89, WTI NEAR $81

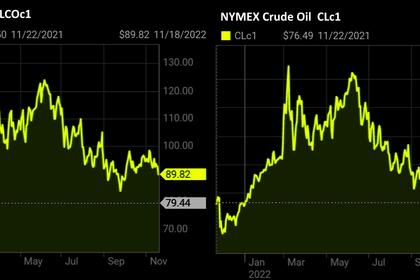

REUTERS - Nov 23 - Oil prices were steady on Wednesday as concerns about lower fuel demand from China amid tightening COVID-19 curbs offset data showing a larger-than-expected U.S. crude draw last week.

Brent crude futures dropped 15 cents, or 0.2%, to $88.21 a barrel at 0508 GMT, while U.S. West Texas Intermediate (WTI) crude futures lost 9 cents, or 0.1%, to $80.86 a barrel.

Both benchmark contracts rose about 1% on Tuesday as the United Arab Emirates, Kuwait, Iraq and Algeria reinforced comments from Saudi Arabia's energy minister that the Organization of the Petroleum Exporting Countries (OPEC) and allies, together called OPEC+, were not considering boosting oil output. OPEC+ next meets to review output on Dec. 4.

Meanwhile, top crude oil importer China has been grappling with a surge in COVID-19 cases that has deepened worries about its economy.

Late on Tuesday, financial hub Shanghai tightened rules for people entering the city while Beijing shut parks and museums.

"Oil is having a tug-of-war with China COVID demand concerns getting countered with what appears to be a motivated Saudi Arabia to keep the oil market tight," said Edward Moya, senior market analyst with OANDA, in a note.

Traders are also being cautious ahead of the release of the U.S. Federal Reserve's minutes from its November policy meeting due at 1900 GMT, CMC Markets analyst Tina Teng said.

"The Fed is expected to signal a slowdown in rate hikes but any surprising hawkish reiteration will weigh on sentiment, lifting the U.S. dollar and pressuring commodity prices," Teng added.

Underpinning oil prices on Wednesday, U.S. crude inventories fell by about 4.8 million barrels for the week ended Nov. 18, data from the American Petroleum Institute showed, according to market sources.

Analysts polled by Reuters on average had expected a 1.1 million barrel drawdown in crude inventories.

Distillate stocks, which include heating oil and jet fuel, rose by about 1.1 million barrels compared with analysts' expectations for a drop of 600,000 barrels.

Uncertainty over how Russia will respond to plans by the Group of Seven (G7) nations to cap Russian oil prices also provided some support to the market.

The price cap is due to be announced soon, a senior U.S. Treasury official said on Tuesday, adding that it will probably be adjusted a few times a year.

"Traders closely monitor Russia's exports and will look for how much they might trim the nation's foreign sales in retaliation, which could be a bullish fillip for oil prices," SPI Asset Management managing partner Stephen Innes said in a note.

-----

Earlier:

2022, November, 21, 11:25:00

OIL PRICE: BRENT NEAR $87, WTI NEAR $80

Brent had slipped 74 cents, or 0.8%, to $86.88 a barrel, WTI were at $79.40 a barrel, down 68 cents or 0.9%.

2022, November, 21, 11:20:00

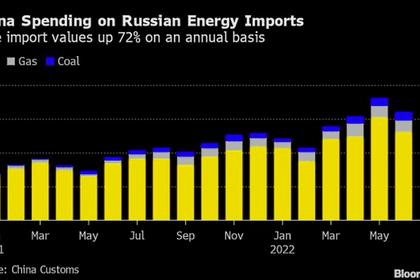

RUSSIAN ENERGY FOR CHINA $60 BLN

Oil imports from Russia rose 16% to 7.72 million tons last month, a volume topped only by Saudi Arabia, according to Chinese customs data.

2022, November, 18, 11:25:00

OIL PRICE: BRENT NEAR $89, WTI NEAR $82

Brent had edged lower by 13 cents or 0.1% to $89.65 a barrel, WTI rose 13 cents, or 0.2%, to $81.77 a barrel.

2022, November, 16, 11:05:00

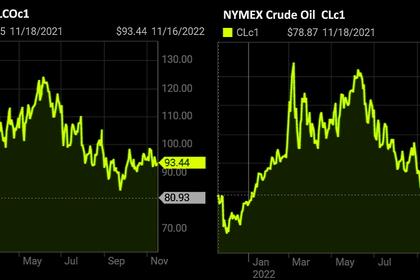

OIL PRICE: BRENT ABOVE $93, WTI ABOVE $86

Brent dropped by 60 cents, or 0.6%, to $93.26 a barrel, WTI fell 69 cents, or 0.8%, to $86.23 a barrel.

2022, November, 16, 10:55:00

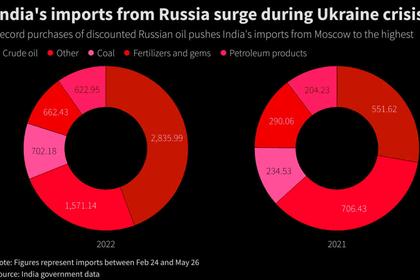

RUSSIAN OIL FOR INDIA UP

From a market share of less than 1% in India's import basket before the start of the Russia-Ukraine conflict, Russia's share of India's imports rose to 4.24 million mt, or nearly 1 million b/d, in October, taking a 21% share comparable to that of Iraq and higher than Saudi Arabia's share of around 15% in the country's import basket in the same month,

2022, November, 16, 10:50:00

RUSSIAN OIL, GAS FOR JAPAN

Japan sees an equity stake in the Sakhalin 1 oil, gas project important as it relies around 95% on Middle Eastern oil imports.

2022, November, 14, 13:10:00

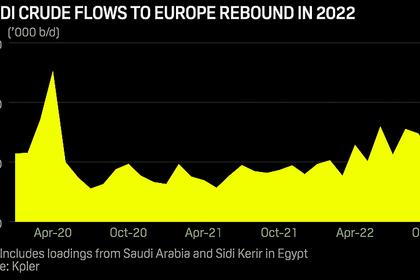

SAUDI'S OIL FOR EUROPE

The Netherlands, Poland, Spain, France and Italy have been the top five destinations for Saudi oil in the region this year, all of which have also been regular buyers of Russian crude.