2022-11-02 11:50:00

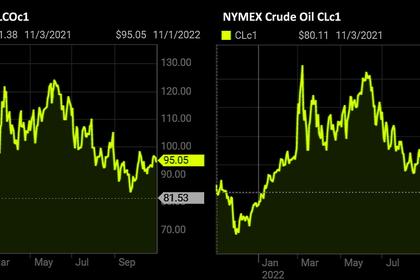

OIL PRICE: BRENT NEAR $95, WTI NEAR $89 ANEW

REUTERS - Nov 2 - Oil prices rose on Wednesday after industry data showed a surprise drop in U.S. crude stocks, suggesting demand is holding up despite steep interest rate hikes dampening global growth.

Brent crude rose 54 cents, or 0.6%, to $95.19 a barrel by 0723 GMT, while U.S. West Texas Intermediate (WTI) crude rose 72 cents, or 0.8%, to $89.09 a barrel.

The benchmarks rose about 2% in the previous session on a weaker U.S. dollar and after an unverified note trending on social media said the Chinese government was going to consider ways to relax COVID-19 rules from March 2023, potentially boosting demand in the world's No.2 oil user.

In a further positive sign for demand, U.S. crude oil stocks fell by about 6.5 million barrels for the week ended Oct. 28, according to market sources citing American Petroleum Institute figures.

Eight analysts polled by Reuters had on average expected crude inventories to rise by 400,000 barrels.

At the same time, gasoline inventories fell more than expected, with stockpiles down by 2.6 million barrels compared with analysts' forecasts for a drawdown of 1.4 million barrels.

"Apart from the larger-than-expected draw in the U.S. inventory data, the optimism from unconfirmed news of China's zero-COVID exit also supported oil's upside momentum," CMC Markets analyst Tina Teng said.

China's zero-COVID policy has been a key factor in keeping a lid on oil prices as repeated lockdowns have slowed growth and pared oil demand in the world's second-largest economy.

Teng added that a softer U.S. dollar was also underpinning oil prices. A weaker dollar makes commodities priced in the greenback cheaper for holders of other currencies.

The greenback slipped from a near one-week peak versus major peers, with traders on tenterhooks before the looming Federal Reserve rate decision on Wednesday.

The potential disruption from the European Union embargo on Russian oil that is set to start on Dec. 5 may also be pushing prices higher. The ban, a reaction to Russia's invasion of Ukraine, will be followed by a halt on oil product imports in February.

"Still, with the EU embargo in the market headlights now, implying the oil complex may lose anywhere between 1-3 million barrels per day, oil could power higher when the embargo kicks in and/or any nod from China that an earlier-than-expected China reopening is on the cards," said Stephen Innes, managing partner at SPI Asset Management in a note.

-----

Earlier:

2022, November, 1, 17:15:00

OIL PRICE: BRENT NEAR $95, WTI NEAR $89

Brent rose $1.95, or 2.1%, to $94.76 per barrel, WTI rose $1.93, or 2.23%, to $88.46 a barrel.

2022, November, 1, 17:10:00

GLOBAL ENERGY DEMAND WILL UP BY 23%

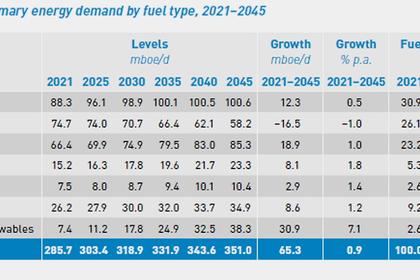

Global primary energy demand is forecast to continue growing in the medium- and long-term, increasing by a significant 23% in the period to 2045. The world needs to annually add on average 2.7 million barrels of oil equivalent a day to 2045.

2022, October, 31, 12:15:00

OIL PRICE: BRENT BELOW $96, WTI BELOW $88

Brent dropped $1.02, or 1.1%, to $95.94 a barrel, WTI were down $1.24, or 1.4%, at $87.84 a barrel.

2022, October, 31, 12:10:00

RUSSIAN OIL UNCERTAINTY

The G7 and EU are finalizing details of a price cap that is intended to be implemented with the EU ban on seaborne Russian crude imports on Dec. 5 and Russian oil products on Feb. 5, 2023.

2022, October, 28, 12:05:00

OIL PRICE: BRENT BELOW $97, WTI ABOVE $88

Brent dropped $1.02, or 1.1%, to $95.94 a barrel, WTI were down $1.24, or 1.4%, at $87.84 a barrel.

2022, October, 27, 15:30:00

OIL PRICE: BRENT BELOW $97, WTI BELOW $89

Brent rose 56 cents, or 0.6%, to $96.25 a barrel, WTI gained 41 cents, or 0.5%, to $88.32.

2022, October, 26, 10:45:00

OIL PRICE: BRENT BELOW $93, WTI BELOW $85

Brent fell $1.03, or 1.1%, to $92.49 a barrel, WTI were down 75 cents, or 0.9%, to $84.57.