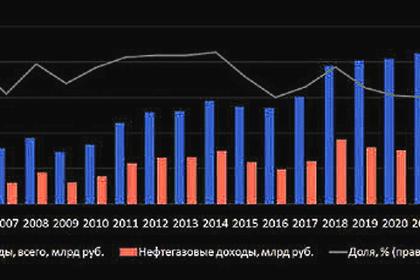

ДОХОДЫ РОССИИ +709,6 МЛРД.РУБ.

МИНФИН РОССИИ - 03.02.2022 - Ожидаемый объем дополнительных нефтегазовых доходов федерального бюджета, связанный с превышением фактически сложившейся цены на нефть над базовым уровнем, прогнозируется в феврале 2022 года в размере +709,6 млрд руб.

Суммарное отклонение фактически полученных нефтегазовых доходов от ожидаемого месячного объема нефтегазовых доходов и оценки базового месячного объема нефтегазовых доходов от базового месячного объема нефтегазовых доходов по итогам января 2022 года составило -74,8 млрд руб.

Таким образом, совокупный объем средств, направляемых на покупку иностранной валюты и золота, составляет +634,7 млрд руб. Операции будут проводиться в период с 7 февраля 2022 года по 4 марта 2022 года, соответственно, ежедневный объем покупки иностранной валюты и золота составит в эквиваленте 33,4 млрд руб.

Трансляции покупок иностранной валюты на внутренний валютный рынок временно приостановлена Банком России с 24 января 2022 года. Решение о возобновлении покупки иностранной валюты на внутреннем валютном рынке будет принято Банком России с учетом фактической обстановки на финансовых рынках.

----

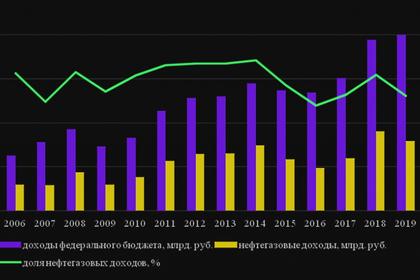

ДОХОДЫ РОССИИ +709,6 МЛРД.РУБ.

ROSNEFT - Financial results for 12M 2018 and 4Q 2018

EBITDA growth by 1.5 times YoY up to RUB 2 trln with margins improvement up to 25%

Net Income jumped by 2.5 times YoY up to RUB 549 bln in 12M 2018

Fee cash flow in 12M 2018 up to USD 17.9 bln

Drop over USD 14 bln of total trading prepayments and net debt

Consolidated IFRS financial results for 12M 2018 and 4Q 2018:

| |

12M 2018 |

12M 20171 |

Change, % |

4Q 2018 |

3Q 2018 |

Change, % |

| Financial results |

RUB bln (except %) |

| Revenues and equity share in profits of associates and joint ventures |

8,238 |

6,011 |

37.0% |

2,165 |

2,286 |

(5.3)% |

| EBITDA |

2,081 |

1,400 |

48.6% |

488 |

643 |

(24.1)% |

| EBITDA margin |

24.8% |

22.6% |

2.2 p. |

22.2% |

27.4% |

(5.2) p. |

| Net income attributable to Rosneft shareholders |

549 |

222 |

>100% |

109 |

142 |

(23.2)% |

| Net income margin |

6.7% |

3.7% |

3.0 p. |

5.0% |

6.2% |

(1.2) p. |

| Capital expenditures |

936 |

922 |

1.5% |

257 |

227 |

13.2% |

| Free cash flow (RUB equivalent)2 |

1,133 |

245 |

>100% |

261 |

509 |

(48.7)% |

| Upstream operating expenses RUB/boe |

194 |

185 |

4.9% |

205 |

193 |

6.2% |

| |

USD bln3 (except %) |

| Revenues and equity share in profits of associates and joint ventures |

133.7 |

106.4 |

25.7% |

33.1 |

35.8 |

(7.5)% |

| EBITDA |

33.1 |

24.0 |

37.9% |

7.4 |

9.8 |

(24.5)% |

| Net income attributable to Rosneft shareholders |

8.9 |

3.8 |

>100% |

1.6 |

2.3 |

(30.4)% |

| Capital expenditures |

15.0 |

15.8 |

(5.1)% |

3.9 |

3.5 |

11.4% |

| Free cash flow |

17.9 |

4.1 |

>100% |

4.0 |

7.8 |

(48.7)% |

| Upstream operating expenses USD/boe |

3.1 |

3.2 |

(3.1)% |

3.1 |

2.9 |

6.9% |

| For reference |

|

|

|

|

|

|

| Average Urals price. USD per bbl |

69.8 |

53.1 |

31.4% |

67.3 |

74.2 |

(9.3)% |

| Average Urals price. th. RUB per bbl |

4.38 |

3.10 |

41.2% |

4.48 |

4.86 |

(8.0)% |

1In 12M 2017 revenues and EBITDA are adjusted due to recognition of the final purchase price allocation of assets acquired in 2017.

2The calculation includes interest expense on the prepayments on the long-term oil and petroleum products supply agreements.

3Calculated using average monthly Central Bank of Russia exchange rates for the reporting period.

Commenting the results for 2018, Rosneft Chairman of the Management Board and Chief Executive Officer Igor Sechin said:

“In 2018 on the background of high volatility of oil prices, changes in tax legislation, regulation of prices for oil products in the domestic market and impact from restriction under OPEC+ Agreement, the Company demonstrated successful production and financial results.

Rosneft continued implementation of investment projects and integration of previously acquired assets.

Its effectiveness is confirmed by the organic growth strategy approved a year ago, aimed at increasing the profitability of the business and maximizing the return on existing assets. At the year-end, the Company generated high cash flow, which led to drop over USD 14 bln of total debt burden.

Approved dividend policy allowed us to increase significantly payments to shareholders that had a positive impact on the Company’s value – since the approval of the Company's strategy in December 2017, the market capitalization growth of the Company amounted to 40% with an average dynamics of about 32% for Russian oil and gas companies.

I would like to note the importance of the upcoming 2019 for the Company. Capital investments are expected at RUB 1.2-1.3 trillion that is driven by the active implementation phase of strategic upstream oil and gas projects and also by projects of construction of modern facilities at the Company’s refineries. At the same time, the Company will continue to improve the efficiency of its financial and operational activities, technological transformation of the business and other tasks that ensure the Company's leadership in the long-term perspective.”

Financial performance

Revenues and equity share in profits of associates and joint ventures

12М 2018 revenue boosted by more than 1.4 times YoY up to RUB 8,238 bln (USD 133.7 bln) mainly due to favorable world price dynamics (+41.2% in RUB terms and 31.4% in USD terms) and growth of equity share in profits of the Russian and international projects (+44% YoY).

4Q 2018 revenue amounted to RUB 2,165 bln (USD 33.1 bln) reduced by 5.3% QoQ in RUB terms due to significant Urals price drop (-8.0% in RUB terms and -9.3% in USD terms) which was partially compensated by higher volumes of crude oil production and sales.

EBITDA

12M 2018 EBITDA grew up to RUB 2,081 bln (USD 33.1 bln) that is in 1.5 times higher compared to 12M 2017. Growth was driven by improvement of the Company’s efficiency, by favorable external market environment and by easing of restriction under OPEC+ Agreement.

12M 2018 YoY increase of 4.9% in lifting costs (from 185 to 194 RUB/boe) was much lower of industrial inflation in Russia (11.9%). The growth was mainly caused by higher repairs and maintenance costs of the growing well stock, oilfield works and higher tariffs of natural monopolies.

EBITDA margin was up to 25% in 12M 2018 on the back of the above factors and the Company’s efforts.

4Q 2018 EBITDA was RUB 488 bln (USD 7.4 bln). EBITDA reduction is mainly caused by the negative impact of export duty lag effect on the back of substantial drop of crude oil price and higher seasonal costs.

4Q 2018 lifting costs were at 205 RUB/boe (3.1 USD/boe) if compared to 193 RUB/boe (2.9 USD/boe) in 3Q 2018. Higher lifting costs in RUB term were mainly caused by higher tariffs of natural monopolies, increased costs in technological transport and production growth after removing of restriction under OPEC+ Agreement.

Net income attributable to Rosneft shareholders

In 12M 2018 net income attributable to Rosneft shareholders increased by 2.5 times YoY and amounted to RUB 549 bln (USD 8.9 bln) despite the recognition of impairment. On the back of higher operating income net income growth was driven by positive FX impact and one-off gain from the share acquisition in upstream JV with a foreign partner and fair value recognition of previously held interest in JV.

4Q 2018 net income attributable to Rosneft shareholders amounted to RUB 109 bln (USD 1.6 bln) compared to RUB 142 bln (USD 2.3 bln) in 3Q 2018. The decrease is mainly due to negative dynamics of operating income (-31.5% to 3Q 2018) and lower positive effect of forex and other income.

Capital expenditures

Capital expenditures amounted to RUB 257 bln (USD 3.9 bln) in 4Q 2018 and RUB 936 bln (USD 15.0 bln) in 12M 2018. Capital expenditures grew by 1.5% YoY in RUB terms. Capital investments are aimed at the implementation of high-efficiency exploration and production oil and gas projects, the continuation of projects for the construction of modern facilities at the refineries, development of in-house services and maintenance of current assets within the approved plan and the Company’s Strategy.

Free cash flow

Thanks to high operating results, implementation of measures to reduce working capital level and favorable price environment the Company has boosted its free cash flow up to RUB 1,133 bln (USD 17.9 bln) in 2018, which is 4 times higher YoY.

Reduction of free cash flow in 4Q 2018 to RUB 261 bln (USD 4.0 bln) was due to decrease in EBITDA.

Financial stability

In 12M 2018 the Company considerably reduced its debt burden: more than 2 times drop in the level of short-term liabilities and net debt/EBITDA of 1.2x in USD terns (cut by 40%) by year end.

RUB 225 bln was paid to the shareholders of the Company in terms of dividend in 2018 including RUB 155 bln in 1H 2018 that is 50% of net income under IFRS and complies with the level approved by the dividend policy. Strong yearly results will also ensure a high level of final dividends, with the higher returns for shareholders.

-----

Earlier:

2018, November, 7, 11:15:00

ROSNEFT - 3Q 2018 EBITDA growth by 13.8% QoQ up to RUB 643 bln, 9M 2018 EBITDA growth by 1.6 times YoY up to RUB 1,593 bln with margins improvement 9M 2018 Net Income jumped by 3.4 times YoY up to RUB 451 bln Free Cash Flow improvement in 3Q 2018 by more than 2 times QoQ up to RUB 509 bln and over 4 times YoY up to RUB 872 bln

|

| |

2018, November, 7, 11:10:00

ROSNEFT - Q3 2018 AVERAGE DAILY HYDROCARBON PRODUCTION REACHED 5.83 MMBOE, DEMONSTRATING A 2.1% GROWTH VS. Q2 2018 LEVEL

|

| |

2018, October, 24, 11:10:00

REUTERS - Russia’s Rosneft (ROSN.MM) and U.S. ExxonMobil (XOM.N) plan to build a liquefied natural gas (LNG) plant in a consortium with Indian and Japanese partners, spreading the estimated $15 billion cost, two sources familiar with the talks said.

|

| |

2018, October, 10, 07:40:00

REUTERS - The Mozambican government said on Monday it had signed oil exploration agreements with U.S. energy firm Exxon Mobil and Russia’s Rosneft.

|

| |

2018, September, 14, 12:20:00

ROSNEFT - Rosneft and the Chinese National Oil and Gas Corporation (CNPC) signed the Agreement on Cooperation in Exploration and Production in the Russian Federation in the framework of the IV Eastern Economic Forum.

|

| |

2018, September, 14, 12:15:00

ROSNEFT - Under the Agreement the parties plan to build over 160 CNG stations in Russia and the possibility of using LNG as natural gas motor fuel is being discussed.

|

| |

2018, September, 7, 12:21:00

ROSNEFT - following the approval of the Rosneft open market share buyback program (the «Program») by the Board of Directors, Rosneft appointed UBS as an independent agent to conduct the open market share buyback on behalf of the Company.

|