2022-02-02 12:20:00

EUROPEAN GAS PRICES DOWN

PLATTS - 01 Feb 2022 - European gas prices were markedly lower in intraday trading Feb. 1 amid news of a substantial supply boost via Ukraine to Slovakia and the apparent return of the Nord Stream 1 pipeline to full capacity.

"With more flows at the moment and the weather forecast still mild, risk premium is taken off the market," a German-based gas trader, adding that the strengthened gas flows could be expected to continue.

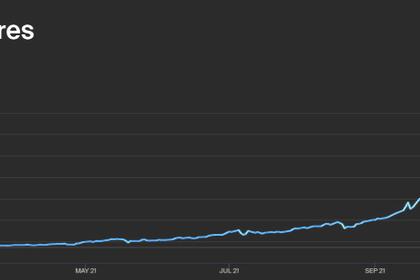

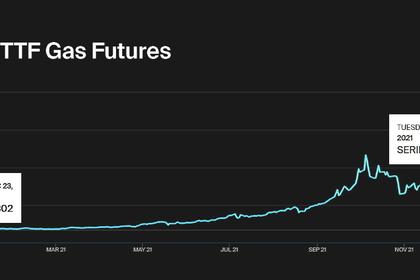

March Dutch TTF futures, which hit a low of Eur74.5/MWh (483.3/MWh) early on, were trading at Eur76/MWh at 1317 GMT, having fallen 7.4% on Jan. 31 to Eur84.025/MWh, as assessed by S&P Global Platts.

Entry gas flow nominations at the Slovakian-Ukrainian interconnection point Velke Kapusany jumped day on day, with Slovakian TSO Eustream's data showing 848 GWh/d (80 million cu m/d) of flows for the Feb. 1 gas day, up from 514 GWh/d on Jan. 31.

Velke Kapusany nominations in January averaged close to 315 GWh/d until Jan. 24, when flows strengthened to average 490 GWh/d for the rest of the month.

At the same time, Nord Stream 1 appeared to be returning to full capacity, according to the operator's data, with hourly gas flow nominations reaching 73 GWh since the start of Feb. 1 gas day, compared with 69 GWh/h for Jan. 31.

Nord stream 1 flows remained below capacity for the whole of January, trending at 1.64 TWh/d compared with the normal 1.75 TWh/d level.

Meanwhile, March UK NBP gas futures, which touched a low of 178.06 pence/therm early on, were trading at 182 p/th by 1315 GMT, having fallen 7.7% on Jan. 31 to 201.5 p/th.

Daily gas flow nominations at the Mallnow compression station in Germany continued to suggest reverse flows on the Yamal pipeline, according to operator Gascade, with no entry flows nominated for Feb. 1 but with exit nominations appearing to decline to 36 GWh/d, compared to 142 GWh for Jan. 31.

-----

Earlier:

2022, January, 12, 10:16:00

GAZPROM'S RECORDS 2021

In 2021, we produced 514.8 billion cubic meters of gas. This is the best result in the last 13 years.

2021, December, 24, 12:05:00

EUROPEAN GAS PRICES DOWN

The front-month wholesale Dutch gas price , which is the European benchmark, eased to 140 euros per megawatt hour on Thursday, down by 15%.

2021, December, 22, 12:15:00

EUROPEAN GAS PRICES UP

Gas prices continued to soar Dec. 21 across the board with assessing TTF front-month at a record Eur180.30/MWh, up 23% on the days and also doubling since Dec. 6.

2021, December, 15, 12:55:00

EUROPEAN GAS PRICES GROWTH

Derivatives linked to TTF, Europe’s wholesale gas price, soared as high as €131 per megawatt hour

2021, December, 9, 12:15:00

EUROPE'S GAS STOCKS DOWN ANEW

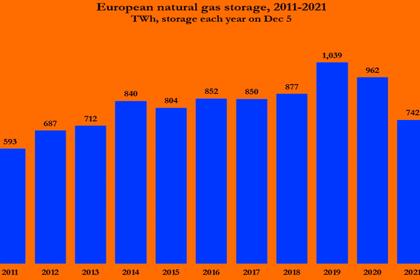

Storage facilities are now only 66% full, a level of depletion they would not normally reach until the middle of January in an average winter.

2021, November, 24, 12:00:00

RUSSIAN GAS TO EUROPE

European and British wholesale gas prices rose on Tuesday as colder weather increased demand and the market remained nervous about winter supplies from Russia.

2021, November, 10, 12:15:00

RUSSIAN GAS FOR EUROPE

European gas prices have remained high through October and November, in part due to lower-than-expected imports from Russia and low levels of EU storage, especially in Gazprom-owned sites such as Rehden in Germany and Haidach in Austria.