2022-03-28 12:05:00

OIL PRICE: BRENT BELOW $117, WTI BELOW $109

REUTERS - March 28 - Oil prices tumbled more than $5 on Monday as fears over weaker fuel demand in China grew after financial hub Shanghai launched a two-stage lockdown to contain a surge in COVID-19 infections.

The market kicked off another week of uncertainty, buffeted on one side by the war between Ukraine and Russia, the world's second-largest crude exporter, and expansion of COVID-related lockdowns in China, the largest crude importer globally.

Brent crude futures slid as low as $115.32 a barrel and were trading down $5.15, or 4.3%, at $115.50 at 0731 GMT.

U.S. West Texas Intermediate (WTI) crude futures hit a low of $108.28 a barrel, and were down $5.30, or 4.7%, at $108.60.

Both benchmark contracts rose 1.4% on Friday, notching their first weekly gains in three weeks, with Brent surging 11.8% and WTI climbing 8.8%.

"Shanghai's lockdown prompted a fresh sell-off from disappointed investors as they expected such a lockdown would be avoided," said Kazuhiko Saito, chief analyst at Fujitomi Securities.

Shanghai launched a two-stage lockdown of the city of 26 million people on Monday, closing bridges and tunnels, and restricting highway traffic to contain surging local COVID-19 cases.

Saito also said the bullish reaction to a missile attack by Yemen's Houthis on a Saudi oil distribution facility had ran its course on Friday.

But he expected the oil market to turn bullish when the Organization of the Petroleum Exporting Countries (OPEC) and allies, known as OPEC+, meet on Thursday, as the group was "less likely to raise oil output at a faster pace than in recent months".

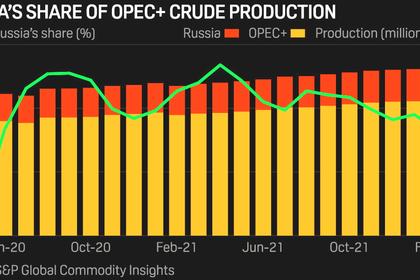

Analysts have varying estimates of how hard Russian oil exports could be hit by economic sanctions imposed on Moscow by the United States and its allies following Russia's invasion of Ukraine. Some reckon that 1 million to 3 million barrels per day (bpd) of Russian oil might not make it to the market.

Russia, which calls its actions in Ukraine a "special operation", exported 4.7 million bpd of crude in 2021, making it the world's second-largest exporter behind Saudi Arabia.

OPEC+ has so far resisted calls from major consuming nations to step up an output boost. The group has been raising output by 400,000 bpd each month since August to unwind cuts made when the COVID-19 pandemic hit demand.

"Oil prices will likely stay above $100 a barrel for a while as global supply will only get tighter as supply from Russia declines while the United States is headed to driving season," said Tetsu Emori, chief executive of Emori Fund Management.

OECD stockpiles are at their lowest since 2014.

To help ease tight supply, the United States is considering another release of oil from the Strategic Petroleum Reserve (SPR) that could be bigger than the sale of 30 million barrels earlier this month, a source said.

"But given the already low inventories, there will be limited release of SPR, which is seen as another supporting factor to the market," Emori said.

U.S. drillers added oil rigs for a 19th consecutive month but at the slowest pace since 2020 even though the government urged producers to boost output.

-----

Earlier:

2022, March, 25, 11:30:00

OIL PRICE: BRENT BELOW $118, WTI BELOW $111

Brent fell 46 cents, or 0.4%, to $118.57 a barrel, WTI ell 47 cents, or 0.4%, to $111.87 a barrel.

2022, March, 25, 11:25:00

OPEC WARNS EUROPE

OPEC has told the EU that global energy markets would be destabilized if European countries follow through with a threat to ban imports of Russian oil,

2022, March, 25, 11:20:00

OPEC+ IS IMPORTANT

In a circular carried by state-run Saudi Press Agency, the cabinet stressed "the importance of the essential role of the OPEC+ agreement in the balance and stability of oil markets."

2022, March, 24, 13:55:00

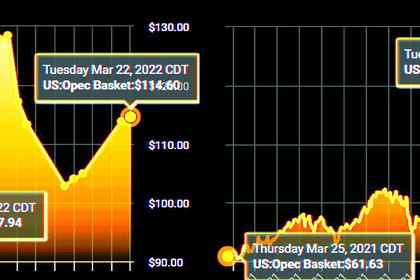

OIL PRICE: BRENT NOT ABOVE $122, WTI NOT ABOVE $115

Brent were down 15 cents, or 0.12%, at $121.45 a barrel, WTI fell 75 cents, or 0.65%, to $114.18 a barrel.

2022, March, 24, 13:50:00

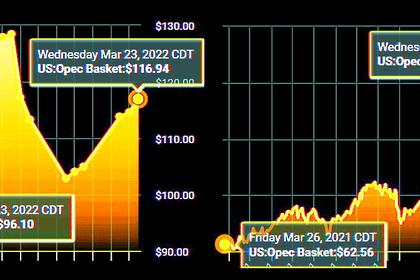

OPEC OIL PRICE: $116.94

The price of OPEC basket of thirteen crudes stood at $116.94 a barrel on Wednesday,

2022, March, 24, 13:40:00

РОССИЯ - ОТВЕТСТВЕННЫЙ ПОСТАВЩИК НЕФТИ, ГАЗА

Россия остаётся ответственным поставщиком нефти и газа, однако мы учитываем и наши интересы на рынке, важность сохранения бесперебойности функционирования сектора.

2022, March, 22, 12:45:00

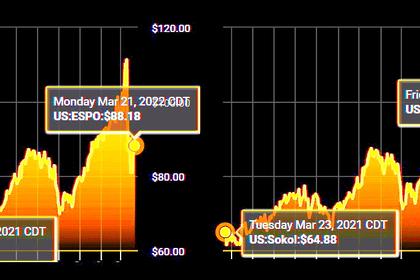

RUSSIA BYPASSES SANCTIONS

"If oil is sold at a discount, then [consumers] will be happy to buy it. We will earn less, but we will be able to place oil," Novak said.