2022-05-26 12:15:00

GAS IS CRITICAL FOR THE GLOBAL ENERGY SYSTEM

IGU - May 25, 2022 - Global Gas Report 2022

Executive summary

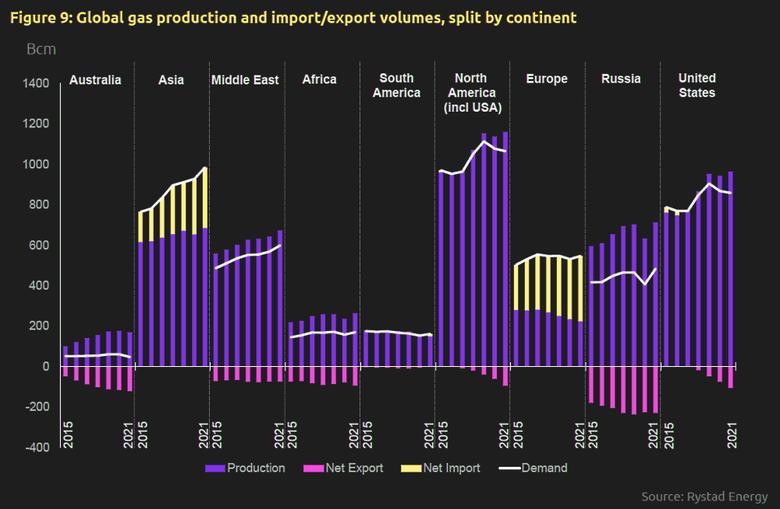

A positive lesson from Covid-19 demand shocks has been the gas value chain’s agility. The natural gas value chain demonstrated notable resiliency through the Covid-19 pandemic. Despite unprecedented shocks to the global energy system and challenging operational environments, gas has continued to reliably fuel society’s critical functions, including power and water supply, hospital equipment, food production, and medical components manufacturing. The industry also nimbly adjusted to geographical and sectorial changes in demand patterns. For example, as the pandemic hit different regions at different times, gas volumes were rerouted to less affected areas where the demand was still strong. The value chain then adjusted back to the demand surge from the post-pandemic recovery, with 2021 natural gas supply surpassing 2019 levels.

The market has seen unprecedented volatility in gas prices over the past two years. TTF gas prices fell to record low levels of $1.20 per MMbtu in May 2020, triggered by nationwide lockdowns and a pandemic-driven low demand environment. US LNG cargos were canceled between April and July, as the market demand remained depressed. Prices recovered quickly in 2021 and rallied upward, as the pace of global economic activity picked up, and gas demand increased, outpacing capacity additions. Both the Asia Spot and TTF gas prices hit record highs, with the Asia Spot price peaking at $54 per MMbtu, as Europe and Asia competed for LNG cargoes. The Russia-Ukraine conflict that started in February 2022 further exacerbated the already tight market, and the TTF Front Month contract was propelled to a new high of $68 per MMBtu in early March. A significant price premium was observed for European cargoes for the first time, as Asian gas was traded at a relatively discounted price.

Upstream oil and gas investments fell by 27% from 2019 to 2020, on top of reduced investments since 2015. This was a consequence of Covid-19 demand destruction and the associated price collapse, as well as uncertainty around future demand and policy direction. Upstream capital investments have been in the range of $400-500 billion between 2016 and 2019, compared to a level of more than $700 billion in 2013 and 2014.

Long-term LNG contracts are gaining in popularity to reduce exposure to spot-priced market volatility, particularly in Europe. The European market, which has been purchasing most of its LNG from the spot and futures markets, was particularly exposed to the price shocks in 2021 and 2022. With lower volumes flowing from Russia, Europe’s reliance on cargoes from the US, Africa and the Middle East increased. China was to some extent shielded from high gas prices, due to its preference for long-term oil-indexed contracts over spot cargoes. A higher share of long-term LNG contracts can be used to minimize exposure to market volatility.

The energy crisis prompted a renewed focus on supply security. For the first time in the history of gas markets, we are seeing a crisis close in scale only to the 1970's oil crisis, when the world faced shortages and price hikes. The crisis has been further exacerbated by supply shortages across all energy commodities, prompting an increased focus on energy security. Future energy systems must be designed with energy security in mind. When it comes to gas, the focus should be on developing a diverse gas supply chain through both upstream production and infrastructure developments. Storage can also play an important role in ensuring energy security by offsetting disruptions to the supply chain. In addition to investing in more storage capacity, governments can impose mandates for minimum storage levels. This has been a common practice with oil, where governments and private practices hold inventories to safeguard the economy and maintain energy security. The European Commission addresses both the questions around a diverse gas supply and storage levels through recently announced policies.

Global CO2 emissions have risen 5% between 2020 and 2021. This is related to the recent gas-to-coal switching. To reverse this rising emission trend, global energy demand-supply will need to be rebalanced, along with appropriate emissions control pricing, carbon and pollution policies.

Extreme weather requires long-term, energysystem- wide, resource adequacy planning. In 2021, the increased frequency of extreme weather events posed significant challenges to the reliable functioning of the global energy systems. Periods of extreme heat and cold, as well as droughts and extended periods with low wind speeds, have highlighted some of the inherent reliability challenges for today’s energy networks. Case studies from the California heatwave, the Texas deepfreeze, the Turkish drought, and periods with low wind speeds in Europe, demonstrated both the key role of gas in ensuring system reliability during long periods of renewable intermittency and the interconnectedness of modern energy systems. These case examples point to the need for deliberate and energy-system-wide planning to assure reliability and avoid cascading failures.

Gas will be critical for an achievable, affordable, sustainable, and secure decarbonization of the global energy system. Initially this can happen through reversing the recent growth in coal use as well as through oil displacement, while supporting the acceleration of renewables deployment through grid balancing and integration in the power sector. Progressively, low-carbon and zero-carbon gases, such as hydrogen, biomethane and natural gas with CCUS, will support deeper decarbonization across sectors alongside renewables and other Paris-compatible fuels. Leveraging existing natural gas infrastructure will be critical in enabling these new decarbonized gas options to commercialize and scale. New gas infrastructure can be designed in a way to enable further scale up of low- and zerocarbon gases and, supporting the achievement of Paris agreement objectives.

Low-carbon and zero-carbon gases are critical to decarbonize heavy industry and manufacturing of vital materials. The industry sector is responsible for around 30% of total energy demand and emissions today, and gas has a crucial role to play in supporting global decarbonization ambitions. Industrial sectors, such as cement, steel, chemicals, and ammonia can be ‘hard-to-abate'. The use of low-carbon and zero-carbon gases in these sectors can provide a viable option to help in deeper sector decarbonization and thereby can resolve the current technical and cost challenges faced by the industry to reduce emissions.

To achieve the desired pace of decarbonization, rapid scale-up of low- and zero-carbon gas technologies will be needed as many are not yet at commercial scale. This will require strong enabling policies, timely investment globally, as well as access to liquidity for capital-intensive projects. To meet the required global capture volume under Rystad Energy’s 1.6-degree scenario, the deployment rate for CCUS needs to scale up by more than 170 times, from around 45 million tonnes per annum of CO2 captured globally today to 8 gigatonnes by 2050. The same could be said for low- and zero-carbon gases. Current production of low- and zero-carbon gases is limited. Blue and green hydrogen contribute less than 1% of pure hydrogen demand, while biomethane represents less than 1% of total natural gas production. While current production levels of green and blue hydrogen and biomethane are low today, there has been stronger policy interest, with more countries committing to development targets and funding over the next decade. In the Asia Pacific region, Japan, South Korea and Australia have introduced roadmaps to set up their hydrogen economies. Japan has committed to increase hydrogen demand to 3 million tonnes per year by 2030, South Korea is set to increase its hydrogen production to 3.9 million tonnes by 2030 and Australia aims to be among the top three hydrogen exporters to Asian markets.

The European Union (EU), under its REPowerEU strategy plans to reduce reliance on natural gas imports and to increase green hydrogen consumption to 20 million tonnes by 2030, of which 10 million tonnes will be imported from non-EU countries. REPowerEU also aims to produce 35 billion cubic meters (Bcm) of biomethane by 2030.

Key insights for the gas industry

Supply Security: The industry should work with policymakers and continue to adjust to changes in demand as the energy transition progresses. It should also continue to work on developing new sources of supply and related infrastructure to ensure supply diversification. This can only be achieved with the right regulatory policy environment on all fronts, including policies that create stability and predictability around future investment decisions. Policymakers and the industry should also work together on defining ways of future-proofing new developments.

Sustainability: The industry should continue to deliver on emission reduction targets. The value of gas in the energy transition will be enhanced further by continuing to deliver on methane emission reduction opportunities. Efforts to scale low- and zero-carbon gas technologies should be strengthened, as these technologies play a key role in the decarbonization of global energy systems. As the gas industry is a key enabler of low- and zero-carbon technologies, future-proofing new assets and infrastructure should be prioritized.

Competitiveness: A rebalanced gas market is expected to improve competitiveness and even the playing field between fuels. Market tightness has led to gas-to-coal switching for power generation, which has resulted in emissions trending upwards. Ensuring that more carbon intensive fuels are not preferred over gas will be key to meeting the emissions targets set by the Paris Agreement.

-----

Earlier:

2022, May, 19, 13:35:00

GLOBAL CLIMATE RESCUE

The global energy system is broken and bringing us ever closer to climate catastrophe.

2022, May, 17, 13:20:00

GLOBAL CHAOTIC ENERGY TRANSITION

The energy transition to net zero emissions will likely take longer than planned, and the cost will be much higher than most realize.

2022, May, 11, 10:55:00

GLOBAL ENERGY, CLIMATE CRISIS

I believe we are in fact in the first global energy crisis, and this is affecting the oil markets, gas markets, electricity markets and coal markets. The world has never seen such an energy crisis.

2022, May, 5, 14:25:00

GLOBAL CLIMATE RISKS 4% GDP

Bangladesh, India, Pakistan and Sri Lanka's exposure to wildfires, floods, major storms and also water shortages mean South Asia has 10%-18% of GDP at risk, roughly treble that of North America and 10 times more than the least-affected region, Europe.

2022, April, 26, 14:00:00

GLOBAL RENEWABLE ENERGY MARKET DOWN

A retreat from wind power could have devastating consequences, as it is set to play a pivotal role in global efforts to transition to green energy.

2022, April, 5, 13:40:00

GLOBAL CLIMATE DISASTER

We are on a pathway to global warming of more than double the 1.5-degree (Celsius, or 2.7-degrees Fahreinheit) limit” that was agreed in Paris in 2015.

2022, April, 1, 11:15:00

GLOBAL CLIMATE DISRUPTION, HAVOC

“Despite growing pledges of climate action, global emissions are at an all-time high,” Mr. Guterres warned. And they continue to rise, he said, adding that “the latest science shows that climate disruption is causing havoc in every region already.