2022-05-11 11:20:00

OIL PRICES 2022-23: $107 - $97

U.S. EIA - May 10, 2022 - SHORT-TERM ENERGY OUTLOOK

Forecast Highlights

Global liquid fuels

The May Short-Term Energy Outlook (STEO) is subject to heightened levels of uncertainty resulting from a variety of factors, including Russia’s full-scale invasion of Ukraine. This STEO assumes U.S. GDP will grow by 3.1% in both 2022 and 2023, following growth of 5.7% in 2021. We use the S&P Global macroeconomic model to generate our U.S. economic assumptions. Global macroeconomic assumptions in our forecast are from Oxford Economics and include global GDP growth of 3.4% in 2022 and 3.5% in 2023, compared with growth of 6.0% in 2021. A wide range of potential macroeconomic outcomes could significantly affect energy markets during the forecast period. Major factors driving energy supply uncertainty include how sanctions affect Russia’s oil production, the production decisions of OPEC+, and the rate at which U.S. oil and natural gas producers increase drilling.

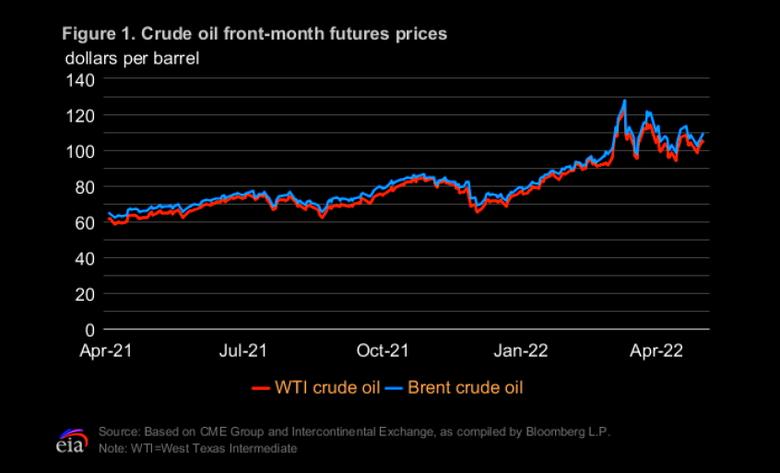

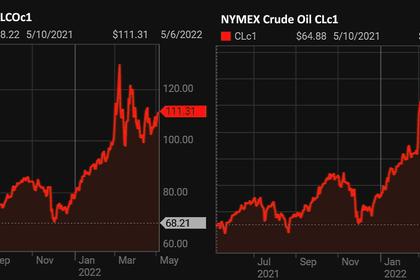

The Brent crude oil spot price averaged $105 per barrel (b) in April, a $13/b decrease from March. Although down from March, crude oil prices remain above $100/b following Russia’s full-scale invasion of Ukraine. Sanctions on Russia and other independent corporate actions contributed to falling oil production in Russia and continue to create significant market uncertainties about the potential for further oil supply disruptions. These events occurred against a backdrop of low oil inventories and persistent upward oil price pressures. Global oil inventory draws averaged 1.7 million barrels per day (b/d) from the third quarter of 2020 (3Q20) through the end of 2021. We estimate that commercial oil inventories in the OECD ended 1Q22 at 2.63 billion barrels, up slightly from February, which was the lowest level since April 2014.

We expect the Brent price will average $107/b in 2Q22 and $103/b in the second half of 2022 (2H22). We expect the average price to fall to $97/b in 2023. However, this price forecast is highly uncertain. Actual price outcomes will largely depend on the degree to which existing sanctions imposed on Russia, any potential future sanctions, and independent corporate actions affect Russia’s oil production or the sale of Russia’s oil in the global market. We completed this outlook on May 5, therefore it does not include an EU ban on oil imports from Russia. However, the bans being reported at the time of writing would likely contribute to tighter oil balances and higher oil prices than our current forecast. In addition, the degree to which other oil producers respond to current oil prices and the effects macroeconomic developments might have on global oil demand will be important for oil price formation in the coming months. We reduced Russia’s oil production in this month’s forecast compared with our April forecast, and we now expect oil markets to be mostly balanced from 2Q22 through the end of 2023. Because oil inventories are currently low, we expect downward oil price pressures will be limited and market conditions will exist for significant price volatility.

We estimate that 97.4 million b/d of petroleum and liquid fuels was consumed globally in April 2022, an increase of 2.1 million b/d from April 2021. We forecast that global consumption of petroleum and liquid fuels will average 99.6 million b/d for all of 2022, which is a 2.2 million b/d increase from 2021. We revised down our forecast for 2022 global consumption of petroleum and liquid fuels by 0.2 million b/d from the April STEO, primarily as a result of downward revisions to consumption growth in China and the United States. We forecast that global consumption of petroleum and liquid fuels will increase by 1.9 million b/d in 2023 to average 101.5 million b/d.

U.S. crude oil production in the forecast averages 11.9 million b/d in 2022, up 0.7 million b/d from 2021. We forecast that production will increase to more than 12.8 million b/d in 2023, surpassing the previous annual average record of 12.3 million b/d set in 2019.

Natural Gas

In April, the Henry Hub natural gas spot price averaged $6.59 per million British thermal units (MMBtu), which was up from the March average of $4.90/MMBtu and higher than the April 2021 average of $2.66/MMBtu. We expect the Henry Hub price to average $7.83/MMBtu in 2Q22 and average $8.59/MMBtu in 2H22. High forecast natural gas prices reflect our expectation that natural gas storage levels will remain less than the five-year (2017–2021) average this summer. Lower-than-average storage levels partly result from limited opportunities for natural gas-to-coal switching for power generation, which we forecast will keep the demand for natural gas for power generation high despite high prices. Natural gas prices could rise significantly above forecast levels if summer temperatures are hotter than assumed in this forecast and electricity demand is higher. In addition, we expect that U.S. liquefied natural gas exports (LNG) will remain high during the summer. We expect the Henry Hub spot price will average $4.74/MMBtu in 2023. The forecast drop in prices for 2023 reflects our expectation that the rate of natural gas production will increase next year while LNG export and demand growth slow, contributing to higher storage levels in 2023 than in 2022.

We estimate that natural gas inventories ended April at 1.6 trillion cubic feet (Tcf), which is 17% below the five-year average. Inventories at the end of April were 190 billion cubic feet (Bcf) higher than at the end of March. This increase was below the five-year average as a result of below-normal temperatures that raised demand for natural gas for heating amid relatively flat production. We expect natural gas inventories to increase by 418 Bcf in May, ending the month at 2.0 Tcf, which would be 14% below the five-year average for this time of year. We forecast that natural gas inventories will end the 2022 injection season (end of October) at almost 3.4 Tcf, which is 9% below the five-year average. However, summer temperatures will be key to storage, and a hotter-than-normal summer that results in high electricity demand could cause inventories to be lower than forecast and result in prices that are higher than forecast.

In April, U.S. LNG exports averaged 11.6 billion cubic feet per day (Bcf/d), slightly below an all-time peak of almost 12.0 Bcf/d set in March. We forecast that U.S. LNG exports will average 12.1 Bcf/d from May through August, which is slightly lower than our previous forecast. This forecast reflects our assumption of slightly lower LNG demand in Asia and Europe this summer compared with our previous assumption, in part because of sustained high natural gas prices. We expect U.S. LNG exports to average 12.0 Bcf/d this year, a 23% increase from 2021. Growth in LNG exports in recent years has been driven by capacity expansions. However, we do not expect any new export facilities to come online in the forecast period, and as a result, forecast growth in LNG exports slows to 5% in 2023, with LNG exports averaging 12.6 Bcf/d for the year.

We expect that U.S. consumption of natural gas will average 85.7 Bcf/d in 2022, up 3% from 2021. The increase in U.S. natural gas consumption is a result of colder temperatures and related higher consumption in the residential and commercial sectors in 2022 compared with 2021. We also expect the industrial sector to consume more natural gas in 2022 in response to expanding economic activity. In addition, forecast natural gas consumption in the electric power sector increases in 2022 because of limited natural gas-to-coal switching despite high natural gas prices. For 2023, we forecast natural gas consumption will average 85.3 Bcf/d, down 1%, mostly as a result of assumed milder winter temperatures (based on forecasts from the National Oceanic and Atmospheric Administration) that will reduce residential and commercial consumption.

We estimate dry natural gas production averaged 95.5 Bcf/d in the United States in April, up 0.4 Bcf/d from March. Although production in April was lower than the recent peak in December 2021, it increased in each of the past two months. Periods of below-normal temperatures and snow in some producing regions, along with seasonal maintenance on pipelines, limited the production increases in April compared with March. We forecast dry natural gas production to average 95.8 Bcf/d in May. For all of 2022, we expect that dry natural gas production will average 96.7 Bcf/d, which would be 3.2 Bcf/d more than in 2021. We expect dry natural gas production to average 101.7 Bcf/d in 2023.

Electricity, coal, renewables, and emissions

We forecast that the annual share of U.S. electricity generation from renewable energy sources will rise from 20% in 2021 to 22% in 2022 and to 23% in 2023 because of continuing increases in solar and wind generating capacity. We forecast that natural gas will provide almost 37% of generation in 2022, which is similar to the level in 2021, and we forecast natural gas generation will provide 36% of generation in 2023. Despite significantly higher natural gas fuel costs this year compared with last year, we do not expect an increase in electricity generation from coal-fired power plants, which have in the past acted as a primary substitute for natural gas in the power industry. Along with the continued retirement of coal-fired generating capacity, the remaining coal fleet has been facing constraints in regard to fuel delivery and coal stocks. We forecast coal will provide 21% of total U.S. generation 2022 and 20% in 2023, compared with a share of 23% last year. Nuclear generation remains relatively constant in the forecast at an average share between 19% and 20%. One nuclear reactor will retire during 2022, and two reactors at the Vogtle nuclear power plant are scheduled to come online in 2023, the first new nuclear units to open in the United States since 2016.

Planned additions to U.S. wind capacity increase wind electricity generation in our forecast. We estimate that the U.S. electric power sector added 14 GW of wind capacity in 2021. Wind capacity additions in the forecast total 10 GW in 2022 and 4 GW in 2023. The electric power sector added 13 GW of utility-scale solar capacity in 2021, and forecast solar capacity additions in the power sector total 20 GW for 2022 and 23 GW for 2023. We expect additions to solar capacity and batteries to account for more than half of new electric sector capacity in 2022 and 2023. In addition, in 2021 small-scale solar (systems less than 1 megawatt) rose by 5 GW to 33 GW. We expect that small-scale solar capacity will grow by 5 GW in 2022 and 6 GW in 2023.

U.S. coal production in the forecast increases by 20 million short tons (MMst) (3%) in 2022 to 598 MMst and by 7 MMst (1%) in 2023. We expect production in the Western region to drive the forecast increases. The forecast increase occurs despite our expectation that coal use in the power sector will decline. We expect rising coal production will replenish electric power sector inventories in 2023 that were depleted during 2021. We also expect coal exports will remain at high levels during the forecast period as a result of high global coal prices. Although exports and inventory builds contribute to rising coal production in the forecast, labor shortages, rail congestion, and challenges obtaining equipment are expected to limit production gains.

U.S. energy-related carbon dioxide (CO2) emissions increased by more than 6% in 2021 as a result of rising energy use. We expect a 2% increase in energy-related CO2 emissions in 2022, primarily from growing transportation-related petroleum consumption. Forecast energy-related CO2 emissions remain relatively unchanged in 2023. We expect petroleum emissions to increase by 3% in 2022 compared with 2021 before growth slows to 1% in 2023. Natural gas emissions rise by 3% in our forecast for 2022, then remain unchanged in 2023. We forecast that coal-related CO2 emissions will fall by 2% in 2022 and by 5% in 2023.

-----

Earlier:

2022, May, 6, 11:30:00

OIL PRICE: BRENT BELOW $112, WTI BELOW $109

Brent rose 88 cents, or 0.8%, to $111.78 a barrel, WTI climbed 84 cents, or 0.8%, to $109.10 a barrel.

2022, May, 6, 11:25:00

ОПЕК + РОССИЯ + 432 ТБД

Участники соглашения сохранили в силе достигнутые ранее договорённости о дальнейшем наращивании производства нефти в июне на уровне 432 тыс. баррелей в сутки.

2022, May, 6, 11:20:00

OPEC+ RUSSIA + 0.432 MBD

Reconfirm the production adjustment plan and the monthly production adjustment mechanism approved at the 19th OPEC and non-OPEC Ministerial Meeting and the decision to adjust upward the monthly overall production by 0.432 mb/d for the month of June 2022, as per the attached schedule.

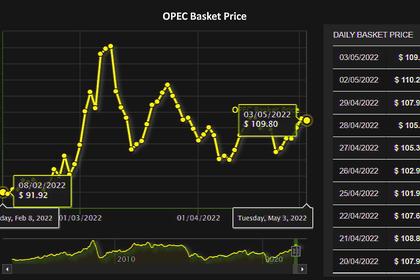

2022, May, 4, 12:25:00

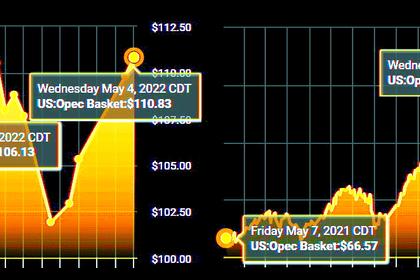

OPEC OIL PRICE: $109.80

The price of OPEC basket of thirteen crudes stood at $109.80 a barrel on Tuesday

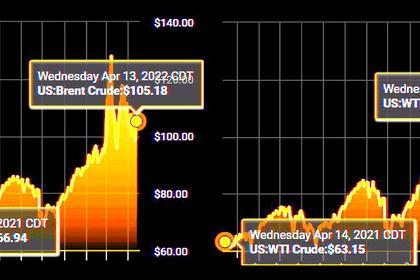

2022, April, 13, 12:50:00

OIL PRICES 2022: $108 - $102

The Brent price will average $108/b in 2Q22 and $102/b in the second half of 2022 (2H22).

2022, April, 12, 13:10:00

OIL PRICE: BRENT ABOVE $101, WTI NEAR $97

Brent were up $2.98 or 3.03% to $101.46 a barrel, WTI was up $3 or 3.18% to $97.29 a barrel.

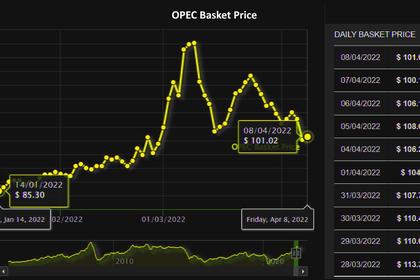

2022, April, 11, 13:25:00

OPEC OIL PRICE: $100.12

The price of OPEC basket of thirteen crudes stood at $100.12 a barrel