2022-06-10 14:40:00

OIL PRICES 2022-23: $108 - $97

U.S. EIA - Jun. 7, 2022 - SHORT-TERM ENERGY OUTLOOK

Forecast Highlights

Global liquid fuels

• The June Short-Term Energy Outlook (STEO) is subject to heightened levels of uncertainty resulting from a variety of factors, including Russia’s full-scale invasion of Ukraine. Global macroeconomic assumptions in STEO are from Oxford Economics and include global GDP growth of 3.1% in 2022 and 3.4% in 2023, compared with growth of 6.0% in 2021. A range of potential macroeconomic outcomes could affect energy markets in the forecast period. Factors driving energy supply uncertainty include how sanctions affect Russia’s oil production, the production decisions of OPEC+, and the rate at which U.S. oil and natural gas producers increase drilling.

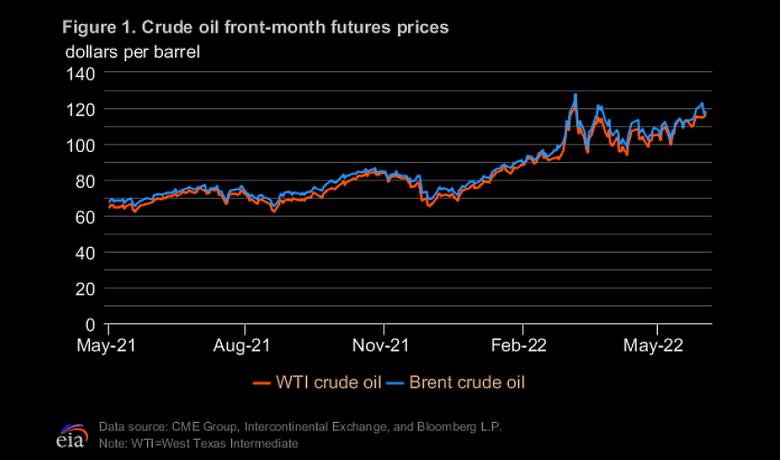

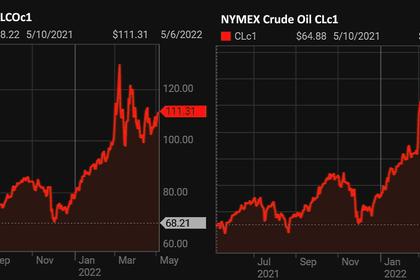

• The Brent crude oil spot price averaged $113 per barrel (b) in May. We expect the Brent price will average $108/b in the second half of 2022 (2H22) and then fall to $97/b in 2023. Current oil inventory levels are low, which amplifies the potential for oil price volatility. Actual price outcomes will largely depend on the degree to which existing sanctions imposed on Russia, any potential future sanctions, and independent corporate actions affect Russia’s oil production or the sale of Russia’s oil in the global market.

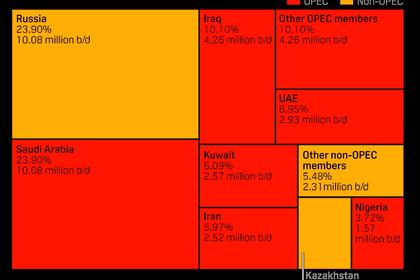

• We forecast Russia’s production of total liquid fuels will decline from 11.3 million b/d in the first quarter of 2022 (1Q22) to 9.3 million b/d in 4Q23. This STEO incorporates the recently announced EU ban of seaborne crude oil and petroleum product imports from Russia. We assume the crude oil import ban will be imposed in six months and the

petroleum product import ban in eight months. This forecast does not reflect restrictions on shipping insurance, as details regarding such restrictions were not available when we finalized this forecast on June 2. The possibility that these sanctions or other potential future sanctions reduce Russia’s oil production by more than expected creates upward risks for crude oil prices during the forecast period.

• At its June 2 meeting, OPEC+ announced an upward adjustment of production targets for July and August. We updated our forecast to reflect these targets. We expect OPEC crude oil production to average 29.2 million b/d in 2H22, up 0.8 million b/d from 1H22.

• The U.S. average retail price for regular grade gasoline averaged $4.44 per gallon (gal) in May, and the average retail diesel price was $5.57/gal. Rising prices for gasoline and diesel reflect refining margins for those products that are at or near record highs amid low inventory levels. We expect the gasoline wholesale margins (the difference between the wholesale gasoline price and Brent crude oil price) to fall from $1.17/gal in May to average 81 cents/gal in 3Q22, and we expect retail gasoline prices to average $4.27/gal in 3Q22. Diesel wholesale margins in the forecast fall from $1.53/gal in May to $1.07/gal in 3Q22, and retail diesel averages $4.78/gal in 3Q22.

• U.S. refinery utilization averages 94% in 3Q22 in our forecast, as a result of high wholesale product margins. Despite our expectation that refinery utilization will be at or near the highest levels in the past five years, operable refinery capacity is about 900,000 b/d less than at the end of 2019, and as a result, we do not expect total refinery output of products to reach its highest level in the past five years. Although we expect high refinery utilization will help bring wholesale margins down from record levels.

Natural gas

• We expect the Henry Hub spot price to average $8.69 per million British thermal units (MMBtu) in 3Q22, up from an average of $8.13/MMBtu in May. Natural gas prices are rising mainly because of three factors: natural gas inventories that are below the fiveyear average, steady demand for U.S. liquefied natural gas (LNG) exports, and high demand for natural gas from the electric power sector given limited opportunities for natural gas-to-coal switching. In 2023, we expect the Henry Hub price will average $4.74/MMBtu amid rising natural gas production.

• U.S. natural gas inventories ended May at 2.0 trillion cubic feet (Tcf), which is 15% below the five-year average. We forecast that natural gas inventories will end the 2022 injection season (end of October) at just over 3.3 Tcf, which would be 9% below the fiveyear average.

• We forecast that U.S. LNG exports will average 11.7 billion cubic feet per day (Bcf/d) during 2Q22 and 3Q22 and 11.9 Bcf/d for all of 2022, a 22% increase from 2021, as a result of additional U.S. LNG export capacity that has come online. Since the end of 2021, the EU and the UK imported record-high LNG volumes because of low natural gas inventories. Europe has become the main destination for U.S. LNG exports and accounted for 74% of total U.S. LNG exports during the first four months of 2022. We forecast LNG exports will average 12.6 Bcf/d in 2023. Expected growth in LNG exports in 2023 results from LNG export terminals that came online in mid-2022 being operational for the whole year in 2023.

• U.S. consumption of natural gas in our forecast averages 85.3 Bcf/d in 2022, up 3% from 2021. Rising U.S. natural gas consumption reflects increased consumption across all sectors. In the residential and commercial sectors, increasing consumption results from colder temperatures in 2022 than in 2021, and in the industrial sector, rising economic activity contributes to higher consumption. Limited natural gas-to-coal switching in the electric power sector, despite high natural gas prices, results in increased consumption of natural gas for power generation. For 2023, we forecast that natural gas consumption will average 85.1 Bcf/d, about the same as 2022.

• We forecast U.S. dry natural gas production to average 95.7 Bcf/d in June and to average 97.9 Bcf/d in 2H22, which would be 2.7 Bcf/d (3%) more than in 2H21. We expect dry natural gas production to average 101.6 Bcf/d in 2023.

Electricity, coal, renewables, and emissions

• The largest increases in U.S. electricity generation in the next two years are likely to come from renewable energy sources, driven by expanded generating capacity from these sources. We expect renewable energy will provide 22% of U.S. generation in 2022 and 24% in 2023, up from a share of 20% last year. Solar capacity additions in the electric power sector total 20 gigawatts (GW) for 2022 and 22 GW for 2023. Solar PV installation delays from 2022 to 2023 account for about 1 GW of the expected installed solar capacity. We expect that small-scale (systems less than 1 GW) solar capacity will grow to a total of 39 GW by the end of 2022 and to 46 GW in 2023.We estimate that wind capacity additions in the U.S. electric power sector will total 11 GW in 2022 and 5 GW in 2023.

• The continued retirement of coal-fired generating capacity in the United States contributes to our forecast that the share of electricity generation from coal will decline from 23% in 2021 to 21% in 2022 and to 20% in 2023. The coal fleet has been facing constraints in raising its share of generation despite high natural gas prices. The constraints include limited rail capacity for fuel delivery, low coal stocks at power plants, reduced coal mining capacity, and rising generation from renewable sources.

• Although we expect annual U.S. natural gas fuel costs for electricity generators will increase 59% in 2022, we do not expect a significant decline in generation from natural gas-fired power plants because of the limited ability of coal power plants to act as an alternative source of generation. We forecast the U.S. natural gas generation share will average 37% in 2022, about the same as last year. The forecast natural gas share averages 36% in 2023 as the share of generation from renewable sources increases.

• We forecast the U.S. residential electricity price will average 14.6 cents/kWh between June and August 2022, up 4.8% from summer 2021. The forecast summer commercial sector price averages 12.0 cents/kWh (up 4.7%) and the forecast industrial sector price averages 7.7 cents/kWh (up 3.2%). Higher retail electricity prices largely reflect higher wholesale power prices and higher natural gas prices. We expect the summer increases in retail residential electricity prices will range from an increase of 2.4% in the West South Central region to a 16.1% increase in New England.

• U.S. coal production in the forecast increases by 23 million short tons (MMst) (3.9%) in 2022 to 601 MMst and then declines by 13 MMst (2.1%) to 588 MMst in 2023. The forecast increase occurs despite our expectation that coal use in the electric power sector will decline. We expect rising coal production will replenish electric power sector inventories and contribute to U.S. coal exports.

• We expect energy-related carbon dioxide (CO2) emissions in the United States to increase 1.3% in 2022 and fall by 0.7% in 2023. Forecast emissions increases in 2022 primarily reflect growth in transportation demand.

-----

Earlier:

2022, May, 6, 11:30:00

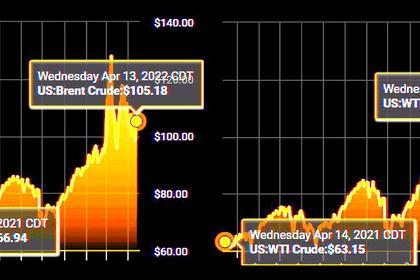

OIL PRICE: BRENT BELOW $112, WTI BELOW $109

Brent rose 88 cents, or 0.8%, to $111.78 a barrel, WTI climbed 84 cents, or 0.8%, to $109.10 a barrel.

2022, May, 6, 11:25:00

ОПЕК + РОССИЯ + 432 ТБД

Участники соглашения сохранили в силе достигнутые ранее договорённости о дальнейшем наращивании производства нефти в июне на уровне 432 тыс. баррелей в сутки.

2022, May, 6, 11:20:00

OPEC+ RUSSIA + 0.432 MBD

Reconfirm the production adjustment plan and the monthly production adjustment mechanism approved at the 19th OPEC and non-OPEC Ministerial Meeting and the decision to adjust upward the monthly overall production by 0.432 mb/d for the month of June 2022, as per the attached schedule.

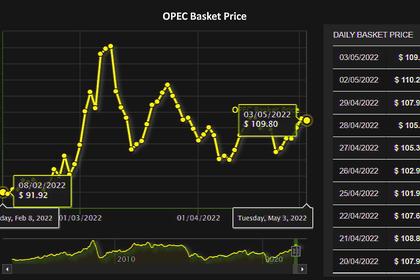

2022, May, 4, 12:25:00

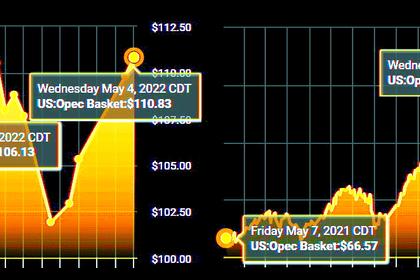

OPEC OIL PRICE: $109.80

The price of OPEC basket of thirteen crudes stood at $109.80 a barrel on Tuesday

2022, April, 13, 12:50:00

OIL PRICES 2022: $108 - $102

The Brent price will average $108/b in 2Q22 and $102/b in the second half of 2022 (2H22).

2022, April, 12, 13:10:00

OIL PRICE: BRENT ABOVE $101, WTI NEAR $97

Brent were up $2.98 or 3.03% to $101.46 a barrel, WTI was up $3 or 3.18% to $97.29 a barrel.

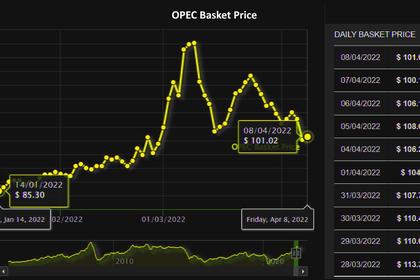

2022, April, 11, 13:25:00

OPEC OIL PRICE: $100.12

The price of OPEC basket of thirteen crudes stood at $100.12 a barrel