2023-01-16 12:35:00

EUROPE NEED U.S. LNG

By VICTOR TENEV LNG Business analyst ROITI limited

ENERGYCENTRAL - Jan 13, 2023 - According to the EU-US announcement, EU commission aims to increase annual demand for American LNG by 50BCM by the end of 2030 and procure 15BCM more in 2022, not to mention the EU’s REPowerEU' s target to reduce dependence on Russian gas by more than 60 per cent within this year. Whereas the LNG's significance remained largely undervalued at COP26 along with the EU Environmental goals for methane emissions, that was all outpaced by the current energy conundrum where LNG influx appears to be a silver lining, though not the sole solution, but rather more as a complementary one.

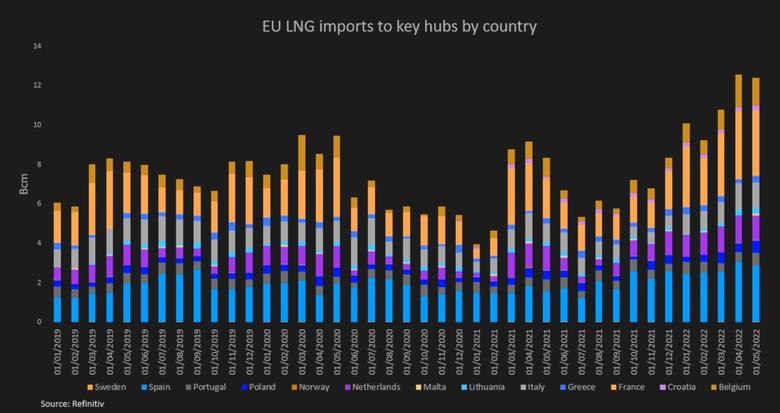

EU IMPORT TERMINALS AT FULL STEAM

As we know, utilization rates of regasification terminals can exceed the standard nameplate capacity during periods of peak use. This is exactly what happened to the Import Terminals which have been running close to their nameplate capacity for the last two months, with definitely the heaviest burden for NW LNG entry points, where the nameplate capacity for some regasification facilities were reaching an all-time peak utilization of 115% in April 2022, notably the Europe’s largest LNG terminal in Kent, UK, cracked their own record.

One fact worthy our attention is that the aggregated Gazprom supply is almost in parity with the overall EU LNG Import; in other words, Gazprom sales could be deemed the same degree of success achieved by EU to secure its LNG shipments. Gazprom's overall natural gas exports to countries outside CIS for the first 4 months of 2022 equals to 50 BCM, whereas over the same period the total LNG imported at the European regas terminals are above 46BCM (average regas - 15bcf/day).

US EXPORT - WINDY AT THE TOP

The United States took the key role as a swing supplier on global gas markets for Q1/Q2 with liquefaction plants running way above their nameplate capacity, exposing them to accidents and failures in equipment and lengthy maintenance outages. In the Freeport instance, utilization exceeded 96% of peak capacity for the last two months, compared to 87% on YOY basis.(EIA estimation)

Freeport's proportion of the Total LNG exported is 20%, whereas the downtime of Freeport will cost almost 40 cargoes or roughly 4.5BCM of natural gas with the terminal not to return to full service until late 2022.

Thinking logically, Freeport outage could not shake up the front position of US in LNG exporting, on the occasion of the proposed LNG Projects, actually this will consolidate more its position as a top producer, by adding "new build LNG liquefaction capacity of 220.3 mtpa (million tonnes per annum) by 2026, while expansion projects account for the rest with 30.3 mtpa." according to GlobalData’s latest report. Interestingly, 160MTPA of the aforementioned 220MTPA are assigned with permits.

ASIA'S STAKE IN THE LNG 'FIGHT-OVER-CRUMBS'

It is very clear that Asian buyers will not stake a claim before the new gas year, mainly due to the absence of well-developed storage infrastructure, unlike Europe. However, the heavily loaded regas plants were and will be the driving force behind any diversion decision for LNG relocation to Asia, despite the price differential in favour of TTF. As the Import terminals capacity is approaching to be fully utilized, the price differential(TTF-JKM) will move towards convergence. Soaring global gas prices have sent a signal that more supply is needed. However, over the last month we have actually seen cargos diverting towards Asia pacific because of regasification constraints in Europe.

Even if it was not for the EU lack of regasification capacity, with the new gas year Asia and Europe would start bidding again for the same LNG cargos, in fact Asia will seek to regain their 2021 volumes, which in 2022 are almost half of what they used to get from the US coast a year ago on YOY basis. Whilst 32 cargoes were contracted before, at this point only 22 cargoes per month are reaching the Asian countries, compared to 65 LNG carriers berthing at European Terminals.

IT HAS BEEN A HECTIC WEEK

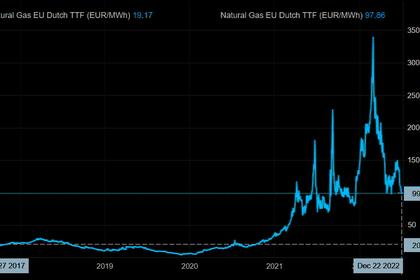

It is doubtful whether Freeport outage or the NS1 dropped 40% was affecting more the prices TTF and HH. The cumulative effect of the Freeport outage along with the drastically reduced pipeline supplies from Russia would have short-term implications for the energy market rather than reshaping the supply and demand in the long run.

This Freeport outage would keep more LNG for domestic sending the U.S. LNG prices down. In the wake of Freeport Terminal downtime, it is evident the linear relationship between LNG export and US domestic prices. In a few words, less export would mean more gas for domestic purposes.

As a result of the Freeport rapid production stoppage hand in hand with the NS1 sizeably reduced gas flow(to 60%), the Henry Hub pricing benchmark dropped by 16%, in parallel the European TTF reference price has seen a price surge with almost 50% in the week after.

ONE SOLUTION DOES NOT FIT ALL

The energy crisis does not develop with equal repercussions for all countries. This multi-faceted problem needs a heterogenous approach, where rather than a magic bullet, each remedy would be just part of the solution, targeted at the different regions in EU.

One part of the solution are the new liquefaction facilities in Sabine Pass and Calcasieu Pass, coming into operation in 2022, adding a combined 26 bcm to the US export capacity. Other U.S. exporters, such as Cheniere Energy Inc (LNG.A) and Sempra LNG, are increasing their efficiency and producing more LNG in order to make up some of the Freeport losses.

Part of the solution could be also if Japan achieve its new energy transition goals, which could then bring up to 31 bcm of LNG to Europe.

In the long term, the existing Global liquefaction capacity of 439MTPA and proposed 1079 MTPA until 2030(only the US proposed/approved LNG capacities - 160MTPA). As regards the EU regasification capacity, new projects might be able to add roughly 17bcm/year of regasification capacity by the end of 2022, with current European regasification capacity standing at 215bcm/year, and at least additional 99bcm/year by 2028. By the end of the decade, in EU more than 350 BCM of Regas capacity is expected to become operational.

In the long run, Qatar seems to be also part of the solution, where Ras Laffan North Field Expansion terminal will be commissioned by 2026-2027 with 32MTPA. Likewise, Italy and Germany are trying to reach an agreement with Qatar for long-term supplies, furthermore Italian company Eni joined Qatar Energy's project to expand production from the world's biggest natural gas field(South Pars/North Dome field), days after Russia slashed supplies to Italy.

Russian LNG Novatek was able to export slightly more in Q1 in contrast with the same period last year. Nevertheless, after the end of June, the Company is struggling not only with its two liquefied natural gas (LNG) projects and their construction, but also with the shipyards in Korea and China, which partially suspended work on their newly ordered ships. On top of this, Novatek came up short of selling its product on the European market as companies steer clear of doing business with the Russian company.

Part of the solution will be the African LNG export which could benefit from the outage, notably Nigerian and Algerian plants, which have "been running at levels far below nameplate capacity". Here, the most likely obstacle could be the diplomacy and the foreign affairs.

Azerbaijan's gas supplies through the South Gas corridor, (TAP and TANAP) with 6.8 billion cubic meters of Azerbaijani gas transported only this year in prospect of 16 billion cubic meters by the end of the year.

The Baltic Pipe Project with commission date October 2022: The offshore junction of Baltic pipeline with the Europipe II(carrying gas from Norway to Germany), will facilitate the transmission of natural gas (more than 10BCM) from Norway to Poland, Denmark, Sweden, the Baltic states and Central and Eastern European regions. For Poland this comes with beneficial opportunities namely the reverse transmission design which enables them to export natural gas(up to 3 BCM) to Denmark and Sweden.(most likely the regassified LNG at Swinoujscie LNG Terminal.)

EU energy rationing plan, where in the meantime referring to traditional sources, (e.g., Germany to head back to atomic energy and prolong the life of remaining three nuclear plants, likewise utilizing the abandoned oil-fired capacity)

All this could serve Europe well in order to make up the difference with the NG deficit.

EU LNG ABSORPTION CAPACITY

The hypothesis that at a maximum capacity EU regasification terminals could process an enormous influx of LNG, does not mean that Europe is fully capable to digest any incremental supply, infrastructure-wise. Put it plainly, main caveat for EU energy system is that it was not designed to be fed with LNG only, along with the entry points it is crucial for EU to build their internal energy market and infrastructure, in order to achieve evenly distributed LNG across the continent. Nevertheless, the European energy status quo is full of inconsistencies, stranded infrastructure PCIs and geographical areas.

Earlier:

2023, January, 5, 16:25:00

EUROPEAN GAS PRICES UPDOWN YET

Dutch front-month futures, the European gas benchmark traded 2% higher at to €66.30 per megawatt-hour by 12 p.m. in Amsterdam. The UK equivalent contract also rose. German power for next month increased 2.3% to €166 per megawatt-hour.

2022, December, 21, 12:20:00

EUROPEAN GAS PRICE CAP

"The TTF month-ahead settlement price for derivatives is by far the most widely used benchmark in gas supply contracts across the EU, followed by maturities of two-month ahead and year ahead," it states.

2022, December, 19, 12:05:00

EUROPEAN GAS PRICES UPDOWN YET

Dutch front-month futures, Europe’s gas benchmark were down 1.3% at €114 a megawatt-hour at 8:51 a.m. in Amsterdam.

2022, December, 19, 11:55:00

EUROPEAN GAS MARKET: DISTORTED

Russia's war against Ukraine that started in February has exacerbated gas prices. But the excesses of the TTF had already been detected before, with rises of more than 700% in 2021.

2022, December, 16, 12:35:00

EUROPEAN GAS PRICES DOWN AGAIN

Dutch front-month gas futures, a European benchmark, were 5% lower at €128 a megawatt-hour at 8:40 a.m. in Amsterdam.

2022, December, 13, 13:50:00

EUROPE NEED MORE GAS

Despite Russia slashing gas deliveries this year, Europe has averted a severe shortage and started the winter with brimming gas storage tanks

2022, December, 13, 13:45:00

EUROPEAN GAS DEADLOCK

Countries led by Germany, the Netherlands and Denmark are calling for a cautious approach, while a group including Belgium, Italy, Greece and Poland is pushing for a more aggressive tool to contain gas prices.