2023-02-10 12:25:00

GLOBAL ELECTRICITY DEMAND UP

IEA - 08 February 2023 - Electricity Market Report 2023

Executive summary

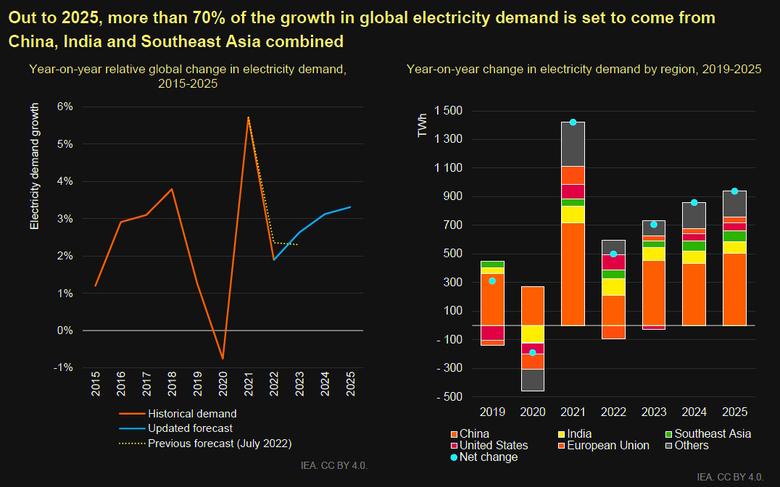

Global electricity demand growth slowed only slightly in 2022 despite energy crisis headwinds

World electricity demand remained resilient in 2022 amid the global energy crisis triggered by Russia’s invasion of Ukraine. Demand rose by almost 2% compared with the 2.4% average growth rate seen over the period 2015-2019. The electrification of the transport and heating sectors continued to accelerate globally, with record numbers of electric vehicles and heat pumps sold in 2022 contributing to growth. Nevertheless, economies around the world, in the midst of recovering from the impacts of Covid-19, were battered by record-high energy prices. Soaring prices for energy commodities, including natural gas and coal, sharply escalated power generation costs and contributed to a rapid rise in inflation. Economic slowdowns and high electricity prices stifled electricity demand growth in most regions around the world.

Electricity consumption in the European Union recorded a sharp 3.5% decline year-on-year (y-o-y) in 2022 as the region was particularly hard hit by high energy prices, which led to significant demand destruction among industrial consumers. Exceptionally mild winter added further downward pressure on electricity consumption. This was the EU’s second largest percentage decrease in electricity demand since the global financial crisis in 2009 – with the largest being the exceptional contraction due to the Covid-19 shock in 2020.

Electricity demand in India and the United States rose, while Covid restrictions affected China’s growth. China’s zero-Covid policy weighed heavily on its economic activity in 2022, and a degree of uncertainty remains over the pace of its electricity demand growth. We currently estimate it to be 2.6% in 2022, substantially below its pre-pandemic average of over 5% in the 2015-2019 period. Further data expected in due course will provide greater clarity on trends in China in 2022, which could also have implications for the global picture. Electricity demand in India rose by a strong 8.4% in 2022, due to a combination of its robust postpandemic economic recovery and exceptionally high summer temperatures. The United States recorded a significant 2.6% y-o-y demand increase in 2022, driven by economic activity and higher residential use to meet both heating and cooling needs amid hotter summer weather and a colder-than-normal winter.

Low-emissions sources are set to cover almost all the growth in global electricity demand by 2025

Renewables and nuclear energy will dominate the growth of global electricity supply over the next three years, together meeting on average more than 90% of the additional demand. China accounts for more than 45% of the growth in renewable generation in the period 2023-2025, followed by the EU with 15%. The substantial growth of renewables will need to be accompanied by accelerated investments in grids and flexibility for their successful integration into the power systems. The increase in nuclear output results from an expected recovery in French nuclear generation as more plants complete their scheduled maintenance, and from new plants starting operations, largely in Asia.

Global electricity generation from both natural gas and coal is expected to remain broadly flat between 2022 and 2025. While gas-fired generation in the European Union is forecast to decline, significant growth in the Middle East will partly offset this decrease. Similarly, drops in coal-fired generation in Europe and the Americas will be matched by a rise in Asia Pacific. However, the trends in fossil-fired generation remain subject to developments in the global economy, weather events, fuel prices and government policies. Developments in China, where more than half of the world’s coalfired generation occurs, will remain a key factor.

China’s share of global electricity consumption is forecast to rise to one-third by 2025, compared with one-quarter in 2015. Over the next three years, more than 70% of the growth in global electricity demand is set to come from China, India and Southeast Asia combined. Emerging and developing economies’ growth is accompanied by a corresponding rise in demand for electricity. At the same time, advanced economies are pushing for electrification to decarbonise their transportation, heating and industrial sectors. As a result, global electricity demand is expected to grow at a much faster pace of 3% per year over the 2023-2025 period compared with the 2022 growth rate. The total increase in global electricity demand of about 2 500 terawatt-hours (TWh) out to 2025 is more than double Japan's current annual electricity consumption. Nevertheless, uncertainties exist regarding the growth of electricity demand in China. While the country recently eased its stringent Covid restrictions in early December 2022, the full extent of the economic impacts remain unclear.

After reaching an all-time high in 2022, power generation emissions are set to plateau through 2025

Global CO2 emissions from electricity generation grew in 2022 at a rate similar to the 2016-2019 average. Their increase of 1.3% in 2022 is a significant slowdown from the staggering 6% rise in 2021, which was driven by the rapid economic recovery from the Covid shock. Nonetheless, electricity generation-related CO2 emissions reached a record high in 2022.

The share of renewables in the global power generation mix is forecast to rise from 29% in 2022 to 35% in 2025. As renewables expand, the shares of coal- and gas-fired generation are set to fall. As a result, emissions of global power generation will plateau to 2025 and its CO2 intensity will further decline in the coming years.

The European Union saw gas-fired generation increase during a turbulent 2022

Due to historic drought conditions, hydropower generation in Europe was particularly low in 2022. Italy saw a drop in hydropower generation of more than 30% compared with its 2017- 2021 average, followed closely by Spain. Similarly, France recorded a 20% decline in its hydro output compared with the previous fiveyear average.

Nuclear generation in the European Union was 17% lower in 2022 than in 2021 due to closures and unavailabilities. Plant closures in Germany and Belgium reduced the available nuclear capacity in 2022. At the same time, France faced record-low nuclear availability due to ongoing maintenance work and other challenges in its nuclear fleet. The constrained nuclear output and low hydropower supply in Europe – combined with reduced dispatchable capacity due to previous retirements of thermal generation plants – put additional pressure on remaining dispatchable capacities to meet demand. As a result, although variable renewable generation grew and record-high gas prices supported fuel-switching from gas to coal, gas-fired generation grew in 2022 by 2% in the European Union. These factors have also contributed to significant changes in the traditional import-export structure of electricity in Europe: France became a net importer and the United Kingdom a net exporter for the first time in decades.

In order to increase the security of electricity supply, reserve capacities of conventional power generation have been brought back in Europe for the 2022-2023 and 2023-2024 winters. Similarly, some plants that were previously set to be decommissioned were also extended. Germany had the highest share of such plants in Europe, having delayed the planned shutdown of its three remaining nuclear reactors, as well as delaying the closure or reactivating fossil-fired plants that make up 15% of its current fossil-fired generation capacity. An increased risk of power outages was reported in some European countries during several weeks of cold weather combined with lower-than-average hydro and nuclear output. Security of supply was achieved through successful short-term planning and management.

While the CO2 intensity of global power generation decreased in 2022, it increased in the European Union

After 2021, 2022 marks the highest percentage growth in CO2 emissions of EU power generation since the oil crises of the 1970s, recording a 4.5% year-on-year growth. Excluding the 2021 post-pandemic rebound, the European Union also saw in 2022 the highest absolute growth in power generation emissions since 2003. This was mainly due to a rise in coal-fired generation of more than 6% in stark contrast to the almost 8% average annual rate of decline in coal-fired generation over the pre-pandemic period of 2015-2019.

The setback in the European Union will be temporary, however, as power generation emissions are expected to decrease on average by about 10% annually through 2025. Both coal- and gas fired generation are expected to see sharp falls, with coal declining by 10% and gas by almost 12% annually on average over the outlook period as renewables ramp up and nuclear generation recovers.

Electricity prices remain high in many regions, with risks of tight supply in Europe next winter

The increase in wholesale electricity prices was most pronounced in Europe in 2022, where they were, on average, more than twice as high as in 2021. The exceptionally mild winter so far in 2022/23 in Europe has helped temper wholesale electricity prices, but they remain high compared with recent years. Elevated futures prices for winter 2023/24 reflect the uncertainties regarding gas supply in Europe over the coming year.

In the European Union, a wide range of responses to the energy crisis have been observed. In order to reduce reliance on fossil fuels and to increase resilience to price shocks, the European Commission published its REPowerEU plan in May 2022 to accelerate clean energy deployment. At the same time, discussions about electricity market design gained momentum due to soaring wholesale prices, and the Commission launched a consultation on market design reform. To dampen the effects of high electricity prices on consumers, many countries introduced measures such as the regulation of wholesale and retail prices; revenue caps on inframarginal technologies such as renewables, nuclear and coalplants; reductions of energy taxes and VAT; and direct subsidies. While such market interventions can help mitigate the impacts of the energy crisis, the potential creation of uncertainty in the investment landscape needs to be minimised to ensure that responses to the crisis do not come at the expense of much-needed investment.

Affordability will continue to be a challenge for emerging and developing economies

Globally, higher electricity generation costs in 2022 were driven by surging energy commodity prices. While the cost increases were more moderate in countries with regulated tariffs and long-term fuel supply agreements (oil-indexed LNG, long-term contracts or fuel supply contracts), regions dependent on short-term markets for fuel procurement were severely affected. In particular, record-high LNG prices led to difficulties for South Asian countries trying to procure gas for the power sector, which contributed to blackouts and rationing of electricity in the region. If prices of energy commodities remain elevated, fuel procurement will continue to be a serious issue for emerging and developing economies.

Nuclear power is gathering pace in Asia, curbing the CO2 intensity of power generation

The energy crisis has renewed interest in the role of nuclear power in contributing to energy security and reducing the CO2 intensity of power generation. In Europe and the United States, discussions on the future role of nuclear in the energy mix have resurfaced. At the same time, other parts of the world are already seeing an accelerated deployment of nuclear plants. As a result, global nuclear power generation is set to grow on average by almost 4% over 2023-2025, a significantly higher growth rate than the 2% over 2015-2019. This means that in every year to 2025, about 100 TWh of additional electricity is set to be produced by nuclear power, the equivalent of about one-eighth of US nuclear power generation today.

More than half of the growth in global nuclear generation to 2025 comes from just four countries: China, India, Japan and Korea. Among these countries, while China leads in terms of absolute growth from 2022 to 2025 (+58 TWh), India is set to have the highest percentage growth (+81%), followed by Japan. This results from the Japanese government’s push to ramp up nuclear generation in order to reduce reliance on gas imports and strengthen energy security. Outside Asia, the French nuclear fleet provides more than one-third of the absolute growth in global nuclear generation to 2025 as it gradually recovers.

Extreme weather events highlight the need for increased security of supply and resilience

In a world where both the demand and supply of electricity are becoming increasingly weather-dependent, electricity security requires increased attention. Along with the high cost of electricity generation, the world’s power systems also faced challenges from extreme weather events in 2022. In addition to the drought in Europe, there were heatwaves in India, where the hottest March in over a century was recorded, resulting in the country’s highest ever peak in power demand. Similarly, central and eastern China were hit by heatwaves and drought, which caused demand for air conditioning to surge amid reduced hydropower generation in Sichuan. The United States saw severe winter storms in December, triggering massive power outages. Mitigating the impacts of climate change requires faster decarbonisation and accelerated deployment of clean energy technologies. At the same time, as the clean energy transition gathers pace, the impact of weather events on electricity demand will intensify due to the increased electrification of heating, while the share of weather-dependent renewables will continue to grow in the generation mix. In such a world, increasing the flexibility of the power systems while ensuring security of supply and resilience will be crucial.

-----

Earlier:

2023, February, 1, 12:00:00

GLOBAL GROWTH WILL DOWN

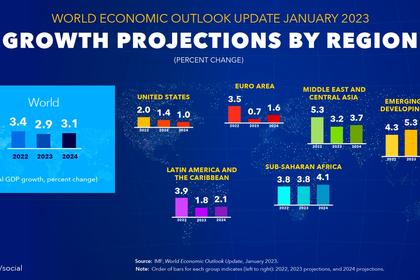

Global growth is projected to fall from an estimated 3.4 percent in 2022 to 2.9 percent in 2023, then rise to 3.1 percent in 2024.

2023, January, 30, 11:30:00

GLOBAL ENERGY TRANSITION FOR PEOPLE

As the world seeks to address climate and biodiversity challenges and move to clean energy solutions for example, these will deliver impacts within the workplace.

2023, January, 16, 13:00:00

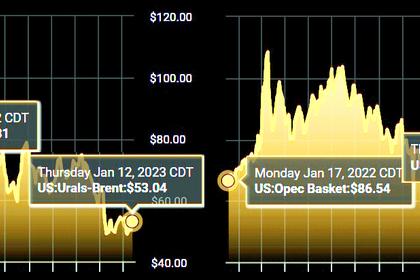

GLOBAL OIL MARKET IS STABLE

The OPEC+ Joint Ministerial Monitoring Committee, on which Mazrouei sits, is co-chaired by Saudi energy minister Prince Abdulaziz bin Salman and Russian Deputy Prime Minister Alexander Novak.

2023, January, 9, 12:20:00

GLOBAL ENERGY TRENDS 2023

Electric utilities are facing a future of increased competition, disruptive technologies, and changing customer demands.

2022, November, 21, 10:50:00

GLOBAL ENERGY TRANSITION DOESN'T WORK

Comparing a Solar Variable Renewable Energy Farm to an On-Demand Base Load Coal Fired Power Station is like saying you can use tomato sauce to replace vegetables.

2022, November, 18, 11:10:00

GLOBAL NUCLEAR POWER FOR CLIMATE

Nuclear energy must play a central role in economic relaunch strategies.

2022, November, 1, 17:10:00

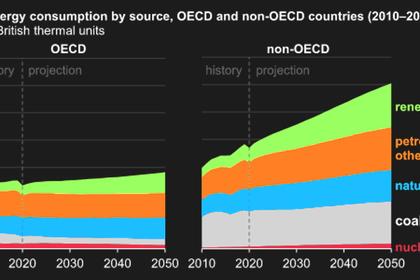

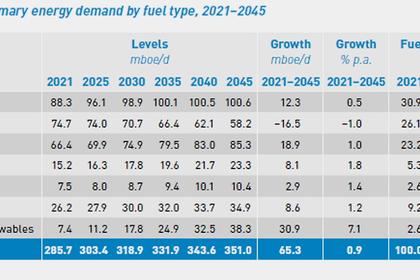

GLOBAL ENERGY DEMAND WILL UP BY 23%

Global primary energy demand is forecast to continue growing in the medium- and long-term, increasing by a significant 23% in the period to 2045. The world needs to annually add on average 2.7 million barrels of oil equivalent a day to 2045.